Michael Saylor’s crypto framework includes ‘concrete’ proposals: Lawyer

Michael Saylor’s not just behind Strategy’s big buys, he’s also looking to define asset classes

Strategy co-founder Michael Saylor | Gage Skidmore/”Michael Saylor” (CC license)

This is a segment from the Empire newsletter. To read full editions, subscribe.

Strategy’s Michael Saylor has had a busy start to the year, between his company buying $2 billion more bitcoin — meaning Strategy now holds nearly 500,000 BTC — and meeting with the SEC’s shiny new Crypto Task Force.

While the former is good for bitcoin, even with the current market falling apart (but David’ll get more into that), I want to focus on the latter today.

Yesterday, my colleague Eleanor Terrett broke the news that Saylor had swung by the SEC’s offices to chitchat with Commissioner Hester Peirce’s new task force, and we — thanks to Saylor himself — now have an idea of what they focused on.

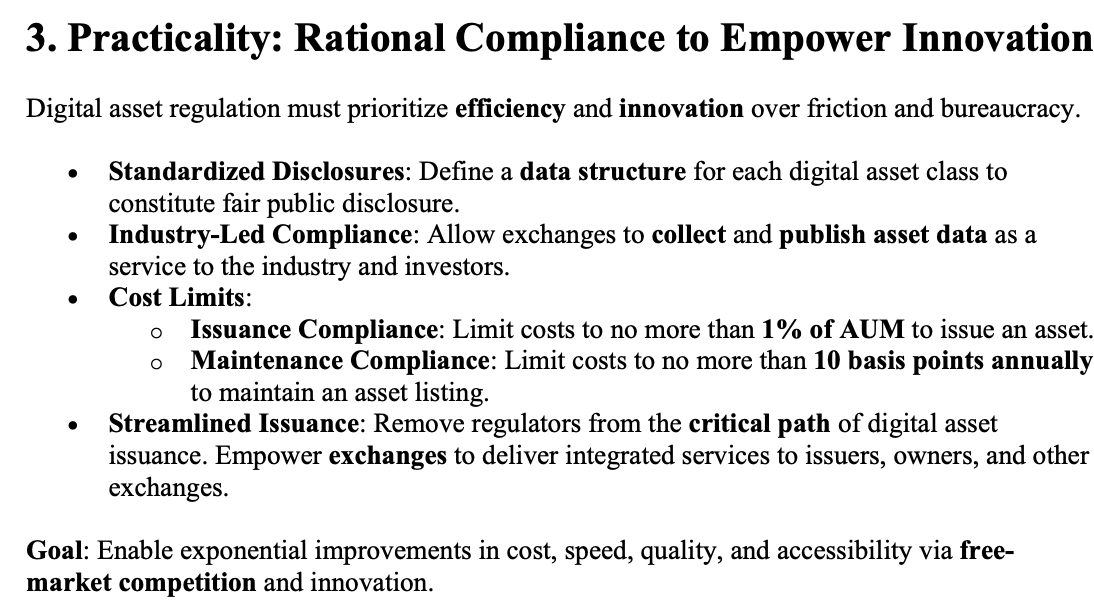

The framework includes definitions for digital asset classes, establishing responsibilities that focus on efficiency and innovation. It also outlines potential gains for the US if it embraces crypto and ensures fair regulation.

Some of the talking points — like a strategic bitcoin reserve and industry-led compliance — are topics we’ve talked about before and shouldn’t be a huge surprise.

But Saylor is showing an interesting tactic here: Not only is he focused on ensuring that Strategy continues to build up its bitcoin treasury (which, one could argue, has helped to keep the price of bitcoin elevated despite the rest of the market meltdown we’ve seen), he’s also now bringing ideas directly to the SEC about how to regulate the broader crypto market.

I caught up with Anthony Tu-Sekine, head of Seward & Kissel’s blockchain and crypto group yesterday and he was most interested by Saylor’s taxonomy section.

From Saylor’s framework

From Saylor’s framework

It’s the most “concrete” proposal of the entire framework, Tu-Sekine noted, and that’s what lawyers are looking for. Even with a more friendly SEC, some of the overhang from the last administration hasn’t been removed and won’t be remedied by dropped investigations and cases into the likes of Coinbase and Robinhood, for example.

Take Kaito for example: One of the questions left over from the token drop is whether or not it’s legal for a centralized company to pursue that type of activity. Tu-Sekine says the tricky part is that it’s still unclear. One could make an argument for both cases, he noted.

Tu-Sekine told me he was looking at Saylor’s proposal from a “practical perspective.”

“Policy goals are great, but they’re meaningless until somebody actually tries to write some sort of rules and a complete proposal.”

The definitions would mark the first step in giving the industry more actionable clarity, and I’d personally argue we see a little bit more of that in Saylor’s compliance section.

If you need some sort of silver lining amid these market conditions, this very well may be a good one to look at.

With this proposal, Saylor’s kicking off the conversations we’ve been trying to have for years now. And it’s clear from the SEC’s docket that he’s not the only one. Robinhood and the Crypto Council for Innovation (which includes reps from heavy hitters like Coinbase) have also met with the SEC.

Now we just need to see some movement.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.