Gox Watch: Payouts quiet after sending out $5.8B before bitcoin crash

It’s been over a week since the last Mt. Gox transfer, and a lot has happened to bitcoin’s price

Primakov/Shutterstock and Adobe modified by Blockworks

What a welcome back to bitcoin for Gox creditors.

As many as 20,600 creditors had been waiting 10 years to have their bitcoin returned, during which time BTC’s price had gone from under $500 to $58,000 when repayments began in May.

About $5.77 billion in bitcoin has been sent to participating crypto exchanges to date, valued at the time of transfer. If a creditor had $1,000 in bitcoin when Mt. Gox collapsed, they would now have over $110,000 based on current distributions.

Read more: Mt. Gox customers to receive crypto assets after 10-year wait

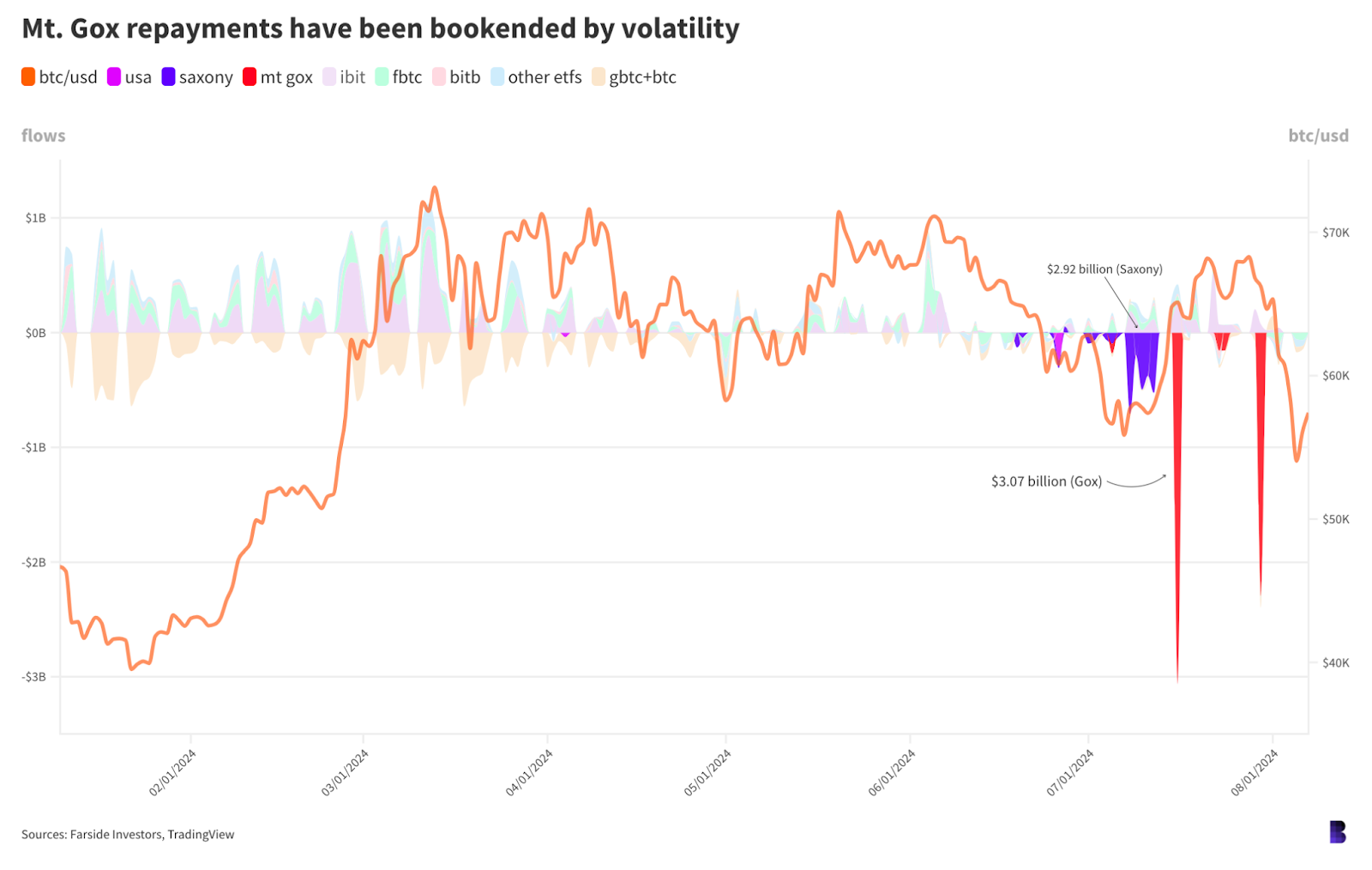

Figures for how much remains differ from screener to screener, but it appears that 51,957.7 BTC — worth $3 billion — is left from an initial 141,690 BTC ($8.15 billion at current prices). All the remaining bitcoin should be sent out sometime over the next two months or so.

For scale, the government of the German state of Saxony in total sent $2.92 billion directly to exchanges and other OTC desks, which on the surface appeared to dent the price of bitcoin, either directly or indirectly.

Saxony’s net outflows are marked in purple on the chart below. Notice those purple areas coincide with a bitcoin dip, and prices picked up directly after they were done.

Mt. Gox distributions are those big spikes downward in red while ETF flows are the lighter colors in the background

Mt. Gox distributions are those big spikes downward in red while ETF flows are the lighter colors in the background

Coincidentally, bitcoin ETFs — particularly BlackRock’s IBIT — posted over days some sizable inflows as Mt. Gox made its $3.07 billion transfer to Kraken.

The inflows, which, all things considered, would’ve hypothetically balanced some selling from Mt. Gox creditors by the end of the day.

Plotting the precise impact of Mt. Gox repayments on the price of bitcoin involves a lot of assumptions. The payments are not being sent directly to individual addresses. Instead, Mt. Gox trustees are forwarding them to cryptocurrency exchanges, which will then credit the bitcoin directly to user accounts.

Read more from our opinion section: The Mt. Gox disaster was essential for crypto’s evolution

The bitcoin is then one button away from being sold and even completely cashed out for fiat. And because hot wallets generally jumble user funds under one address, once Mt. Gox bitcoin goes in, there’s little way of knowing what happens to it from there.

Glassnode at the end of last month still gave it a go. Its analysts compared Kraken and Bitstamp volumes around the time of Gox distributions and found only a marginal uptick in sell-side dominance, still within typical ranges.

Still, there were some major whales among Gox creditors. Twenty-three alone had claims to more than a quarter of all funds ($2 billion at current prices), and the top 1% of creditors were set to receive more than half.

If any of them decided to sell all at once, on public markets and not over-the-counter, then it’s reasonable to assume that they could impact prices in the short-term.

And then there’s investors in bitcoin ETFs, who have net pulled over half a billion dollars from ETFs in the past three days — during which time the price of bitcoin has fallen by 20%.

If the macro environment truly set bitcoin up for a fall, ETFs could have very well pushed it over the edge, especially so if they were selling at the bottom. In that case, bitcoin will have to get back up before Mt. Gox joins back in.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.