Insights / DeFi Credit Risk

Will tranching eat looping?

Tranching brings structured-finance risk allocation onchain. How it maps to looping, where the two differ, and why combining them creates more tailored credit.

By Silvio Busonero ·

Tranching is a new primitive that's seeing early adoption. The DeFi economy is built on looping, which fuels around 40% of lending revenues.

Both looping and tranching are a risk transfer mechanism between senior capital (lenders) or junior capital (loopers). But tranching actually expands and completes what can be done with looping.

Protocols like Royco, Strata, and Reflect on Solana offer a tranching protocol, while others embed tranching as a core mechanism.

On the DeFi side, the TVL in tranching protocols is still small and constitutes a tiny fraction of lending market deposits (<1%). That said, it is one of the few verticals showing growth despite the bear market.

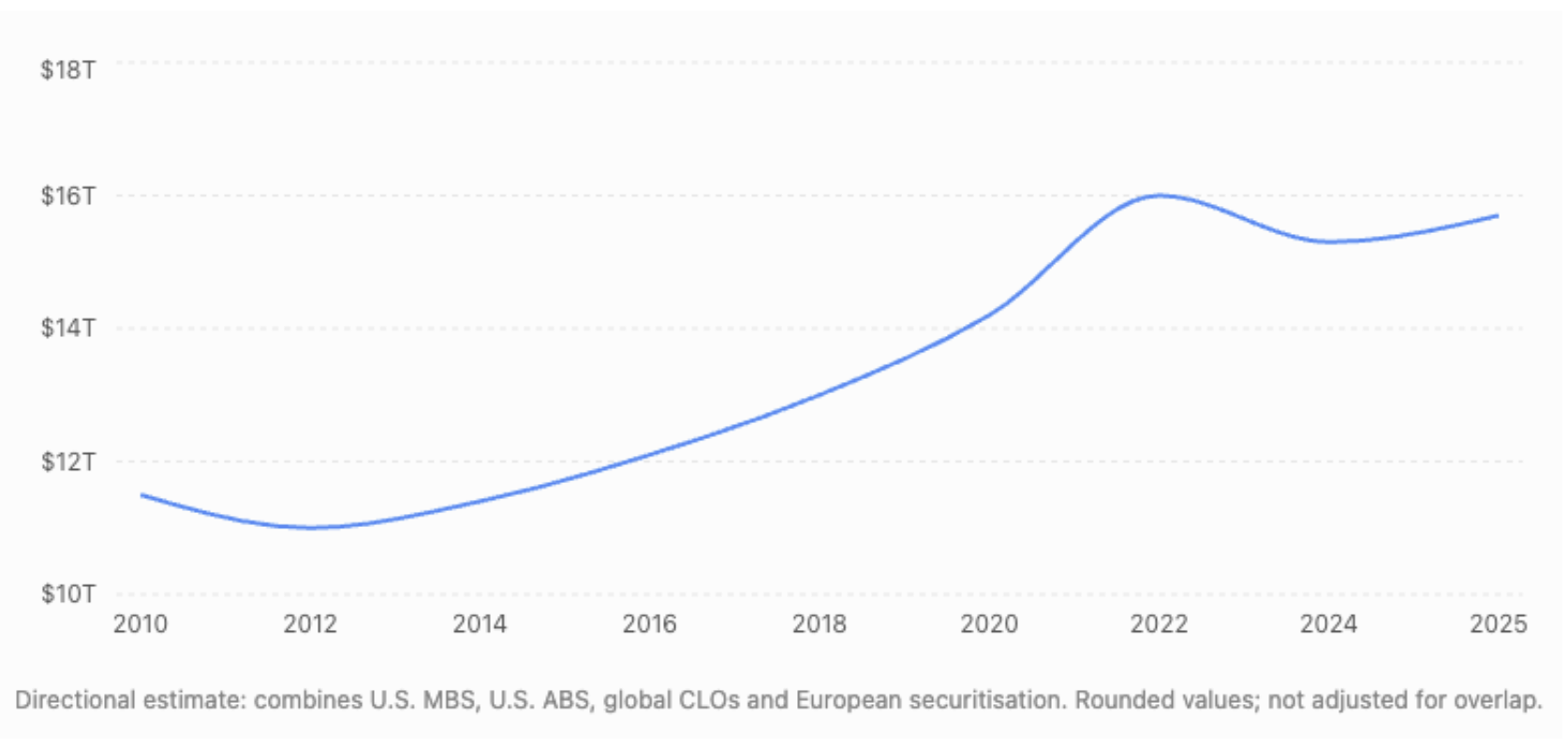

On the TradFi side, structured finance is a $15T market, mostly driven by mortgages.

My view is that this will grow meaningfully, and tranching is early but very promising.

The parallel between looping and tranching

The general principle of tranching is that the junior protects the senior from losses, up to a certain coverage. The mechanism is based on a market-clearing formula (like utilization in the case of Royco, and a coverage aware risk premium on Strata) to determine the optimal coverage of the senior tranche.

Looping is built very differently through the process of recursive rehypothecation, but it creates a very similar effect: the loopers are the equivalent of junior capital when the assets incur losses, as they absorb them through liquidations.

How about the senior tranche? In looping, there is no explicit definition of protected capital.

However, the senior role overlaps pretty much with lenders. As a lender, you would incur losses only if the collateral gets permanently impaired below the liquidation thresholds (which works as the coverage for the tranching).

Risk map of tranching vs. looping

Let's see how the main risk spreads with these two structures.

Temporary depegs are not absorbed by the junior tranches because losses are realized after an observation period (1-2 weeks). That means no money for liquidators. On the other side, this remains a true risk for loopers, depending on the oracle configuration.

In the case of permanent asset impairment, the senior tranche and lender are both protected up to a certain coverage or liquidation loan-to-value, so the two structures are similar.

It's important to emphasize again the cooldown mechanism of tranches. In case of lending, loopers can close their positions instantly, spiking utilization and triggering a cascade of withdrawals, and exposing lenders to higher risk. This is partially solved by withdrawal queues. On the other hand, withdrawals of junior tranches are often delayed or implement a cooldown preventing such a bank run.

Negative carry is a risk for loopers only, as the junior tranche gets yield without borrowing costs.

Some tranching products like Strata also protect against yield variance, which provides a more stable yield to senior and more volatile yield to junior tranches. In the looping case, the borrowers always bear rate risk.

| Risk | Tranching | Looping |

| Gap risk (temporary depegs) | None / dependent on market set up | Borrower |

| Negative carry | None | Borrower |

| Permanent impairment | Junior, then senior if impairment > coverage | Borrower, then lender if impairment > LLTV |

| Smart contract risk of underlying | Senior if larger than LLTV | Borrower up to LLTV |

| yield variance | Can be borne by Junior, depending on market config | Absorbed by borrower / looper |

| Withdrawals during stress | Control bank run via cooldown mechanism | Withdrawal queue can expose to liquidation cascade |

The risk profile may look similar, but tranching allocates losses to specific risk types far more precisely and explicitly.

The tranching-looping parallel also maps more cleanly onto isolated lending markets than onto monolithic protocols. In a pool like Aave, borrow costs depend on broad utilization across all assets and borrowers, so the rate a looper pays reflects pool-wide demand rather than the risk of their specific position, making the comparison to a cleanly priced tranche looser.

Another key difference is that loopers can choose the level of leverage based on what makes them comfortable. On the other hand, junior tranches don't offer the same levels of flexibility but have the advantage of being tokenized and support secondary liquidity. Bear in mind that looping also has larger costs: issuers need in-depth redemption and secondary liquidity for the markets to work well.

The optionality of tranching + lending

The fact that the risks covered are not identical implies that the two can be combined to create more tailored risk profiles:

- Lending against senior collateral provides additional seniority compared to holding the senior tranche. The lender would have an additional layer of protection for losses on the collateral up to liquidation LTV. Besides, looping increases the liquidity in senior tranches, therefore also pushing the APY for junior tranches (to maintain optimal coverage). My view is that this will be the fastest-growing intersection of the two models. For an asset issuer and curators, the opportunity is to grow TVL by focusing on looping senior capital and providing the junior capital with its own money.

- Lending against junior collateral is trickier. The lender is not lending against a stable asset with ordinary price volatility; they are lending against a claim whose value can drop rapidly when losses approach the junior threshold. This creates lots of friction and liquidity issues. These markets will take more time to develop.

This table shows intuitively the waterfall of losses, assuming a start with the position of 80 senior value, 20 junior value, and with both senior lender and junior lender.

| Pool loss | Junior value | Junior borrower equity | Junior lender outcome | Senior value | Senior borrower equity | Senior lender outcome |

| $0 | $20 | $2 | Fully covered | $80 | $8 | Fully covered |

| $1 | $19 | $1 | Fully covered | $80 | $8 | Fully covered |

| $2 | $18 | $0 | Break-even | $80 | $8 | Fully covered |

| $5 | $15 | $0 | $3 shortfall | $80 | $8 | Fully covered |

| $10 | $10 | $0 | $8 shortfall | $80 | $8 | Fully covered |

| $20 | $0 | $0 | $18 shortfall | $80 | $8 | Fully covered |

| $25 | $0 | $0 | $18 shortfall | $75 | $3 | Fully covered |

| $28 | $0 | $0 | $18 shortfall | $72 | $0 | Break-even |

| $30 | $0 | $0 | $18 shortfall | $70 | $0 | $2 shortfall |

| $50 | $0 | $0 | $18 shortfall | $50 | $0 | $22 shortfall |

| $100 | $0 | $0 | $18 shortfall | $0 | $0 | $72 shortfall |

Besides the extra optionality, tranching is the best fit for cases when shortfall precision is required: think about curators and underwriters providing first-loss capital for complex products. This is key in private credit: some protocols like Pareto already support tranching natively in their onchain credit facilities, and those facilities are open enough that others can build their own tranche models on top. Royco does this with Pareto's FalconX vault and its “receipt token.”

Tranching is tailored DeFi

DeFi risk management is going from brute-force recursive looping to deliberate financial engineering. Tranching brings the accuracy of structured finance to onchain markets, replacing liquidation thresholds with explicit first-loss protection and dynamic pricing.

More broadly, a market with a diverse set of risk-management tools is a more efficient one. The more structures that coexist around the same underlying credit, the more precisely capital can sort itself to the risk it actually wants.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network

Resources & Legal