Insights / Advisory Analysis

JAAA as USDe backing asset

JAAA, the Janus Henderson Anemoy AAA CLO Fund, is eligible for Ethena's USDe backing under Blockworks Advisory's adapted RWA framework. A demonstrated $318.6M single-day redemption supports an initial $250M allocation, though elevated holder concentration remains an open monitoring item.

By Blockworks Advisory ·

Instrument structure

Fund architecture and issuer

Anemoy Capital SPC Limited is a British Virgin Islands segregated portfolio company that issues the JAAA token. The fund's sole mandate is to hold AAA-rated collateralized loan obligation tranches benchmarked to the methodology of the Janus Henderson AAA CLO ETF (NYSE: JAAA). Subscriptions and redemptions settle in USDC where trading and custody operations have been migrated to JPMorgan with fund administration provided by Trident Trust. Reinvestment and rebalancing decisions are made solely by Janus Henderson Investors US as portfolio manager and sub-investment manager, without a requirement for Anemoy approval at any size or risk threshold. The management fee is 40 bps per annum with additional pass-through costs for brokerage, custody, administration, and audit, making the total annual cost to holders above the 40 bps headline.

Tokenization is delivered through the Centrifuge V3 protocol. The JAAA token represents a participating share in the segregated portfolio, and the deJAAA token is an ERC-20 wrapper that enables DEX trading without initiating a primary redemption. The two tokens are economically linked but operationally separate, where deJAAA liquidity does not substitute for primary redemption capacity.

Subscription and redemption mechanics

Primary redemptions operate through the Centrifuge epoch architecture, which batches investor requests into monthly cycles. Investors submit onchain, the fund processes once per epoch, with USDC proceeds returned after the cycle closes. Observed settlement within this architecture is fast with P90 of 1.98 business days and a maximum of 3.71 days in the sample. There are no formal daily redemption capacity limits. Settlement targets T+1 (contractual settlement period is three business days) with a 2 pm ET cut-off where the fund notifies investors immediately via Telegram and email in the rare event that TradFi settlement processes cause a delay. This has not occurred since the migration to JPMorgan. Janus Henderson has not experienced a redemption restriction or failure to meet settlement timing in any fund or strategy across EMEA, the US, and Australia. Subscriptions and redemptions are struck at the following day's NAV, eliminating intraday price slippage risk.

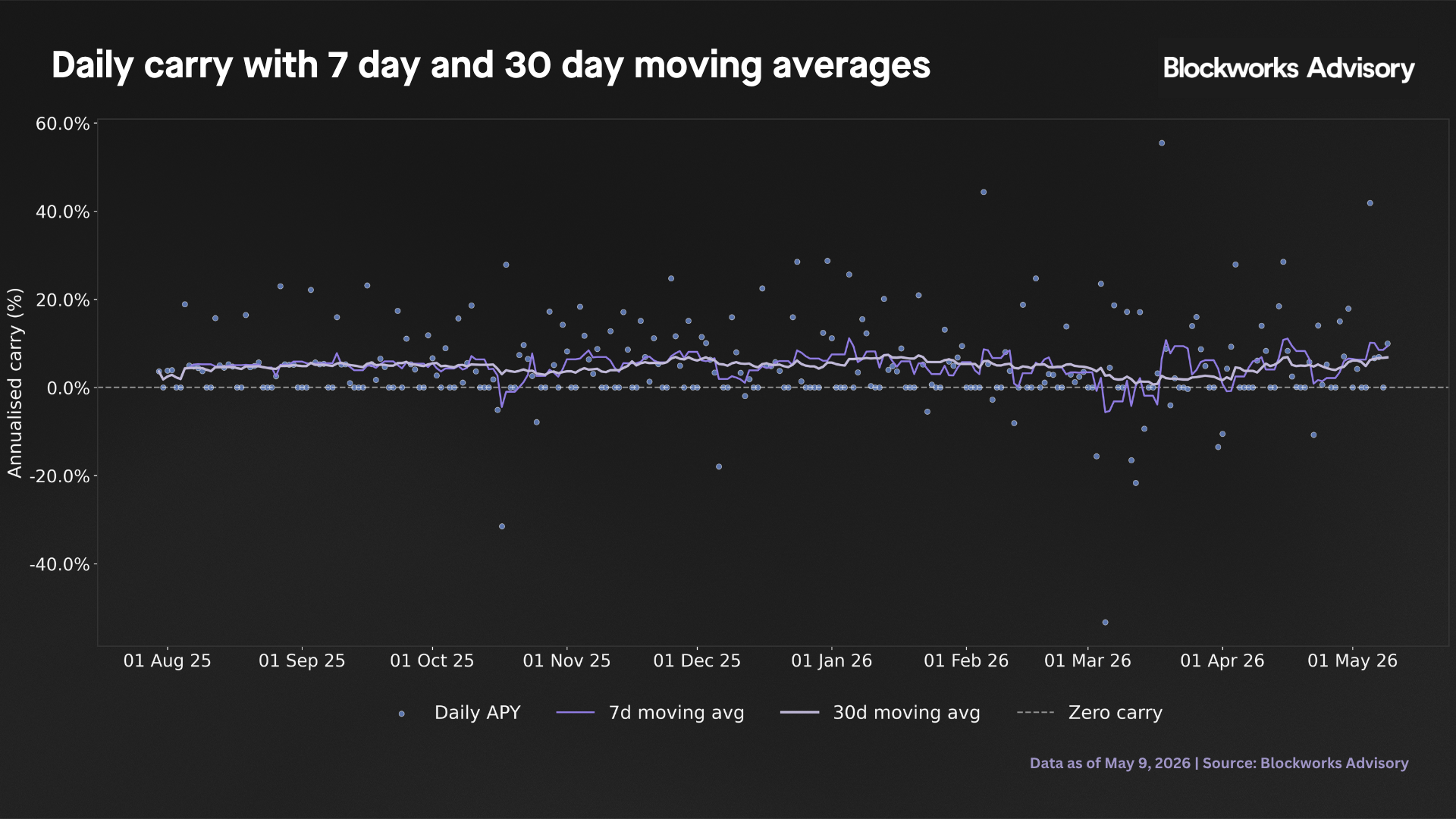

The epoch architecture produces an important data artifact. CLO income accumulates continuously but is recognized in the NAV on a single settlement day per month. This causes the daily annualized return to spike to 30-55% on the one settlement day and to near zero on all other days. The resulting distribution has a standard deviation of 9.85% and a range of -53% to +55% values that are mechanically impossible for a fund holding only AAA CLO tranches. The 30-day moving average of 6.83% at the analysis date is the economically meaningful carry indicator. All scorecard carry assessments use the 30-day moving average or the median; the raw daily series is shown for completeness only.

The Information Memorandum does not reference the right to suspend, gate, prorate, or defer redemptions; payment is specified within three business days. The governing PPM and Articles nonetheless grant the Board extensive discretionary suspension powers, including suspension in circumstances where the Board of Directors may determine in its sole discretion. The Board may also compulsorily redeem any shareholder's shares with or without cause in the sole discretion of the directors on seven days notice. These powers have not been exercised in the fund's operating history.

Portfolio characteristics

The April 2026 holdings confirm 20 CLO positions and one cash or money market position of $24.1M (5.9% of the $408M portfolio). All 20 CLO positions carry AAA ratings at original issuance and at the current date with zero non-AAA holdings. The weighted average price of the portfolio is $100.12 as of April 30, 2026, indicating no mark-to-market distress. As of May 21, 2026, 79% of the portfolio by NAV is within its non-call period.

The top three managers by weight are Madison Park (17.42%), CBAM (12.29%), and KKR (9.82%), with a combined top three share of 39.5% and the top 10 managers accounting for 83.3% of the portfolio. The largest single CLO position is ARES 2022-ALF2A at 8.12%. Position level HHI is 5.4% and manager level HHI is 9.0%. Six positions exceed the 5% per CLO limit, and one manager (Madison Park at 17.42%) exceeds the 15% per manager limit that applies to the JAAA ETF under its prospectus; these limits do not apply to the Centrifuge fund, which operates without hard concentration thresholds and intentionally builds a more concentrated portfolio to obtain better execution in block trades. No AAA CLO tranche has ever defaulted or been downgraded.

Portfolio count declined from 55 positions at the December 2025 peak ($1,022M AUM) to 21 positions at April 2026 ($408M AUM), reflecting the AUM reduction from Grove redemptions. The underlying managers across all four reference dates are consistent.

Cross-chain architecture

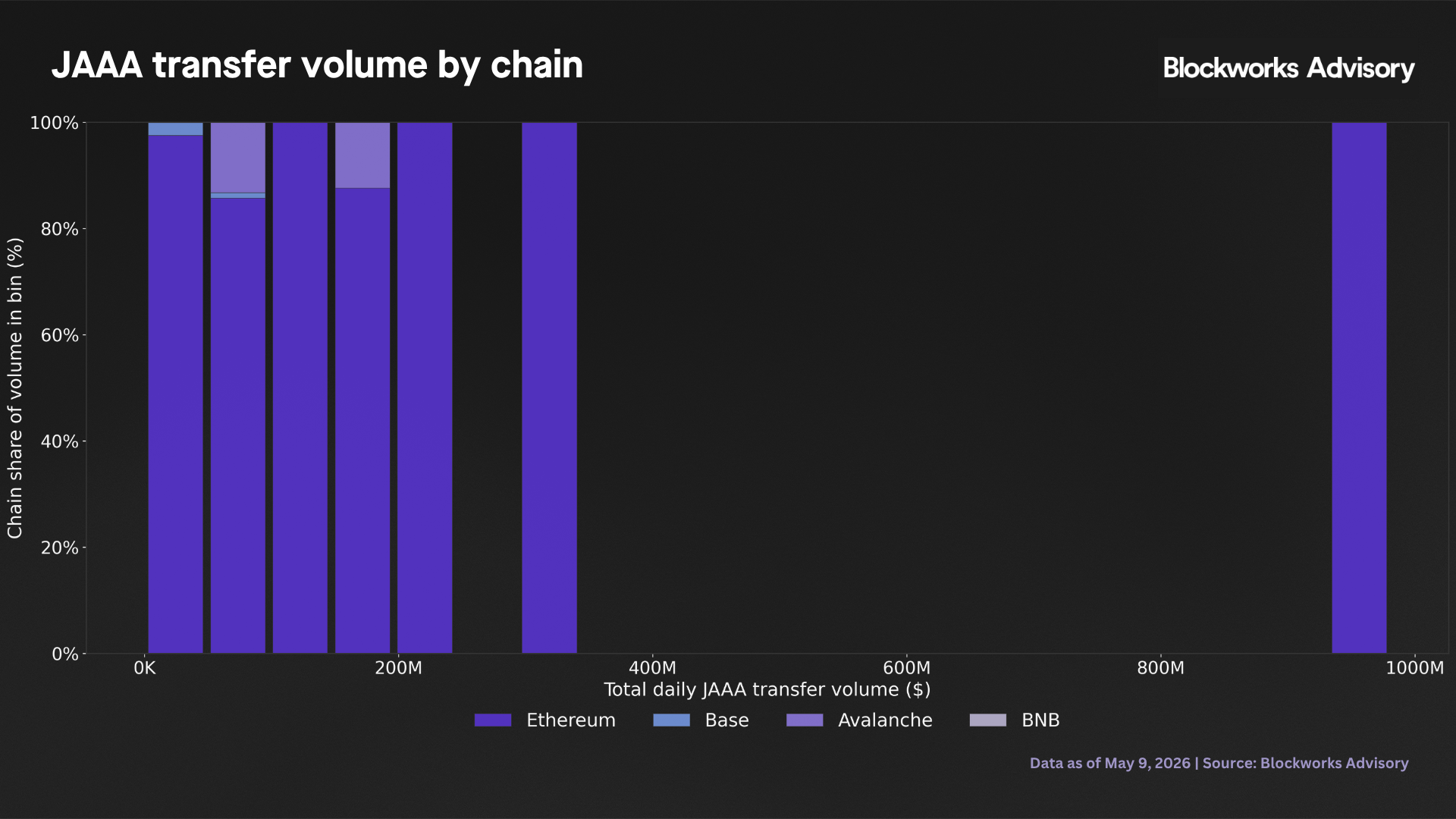

JAAA and deJAAA tokens are deployed on Ethereum (94.6% of combined transfer volume), Avalanche (4.5%), Base (0.9%), and BNB Chain (under 0.1%). Cross-chain token movement relies on bridge adapters whose specific implementation and quorum configuration have not been disclosed. The April 2026 rsETH exploit demonstrated that a forged cross-chain message via a compromised adapter can drain bridged RWA positions at scale. Until adapter architecture is confirmed, bridge security risk cannot be quantified.

NAV stability and yield economics

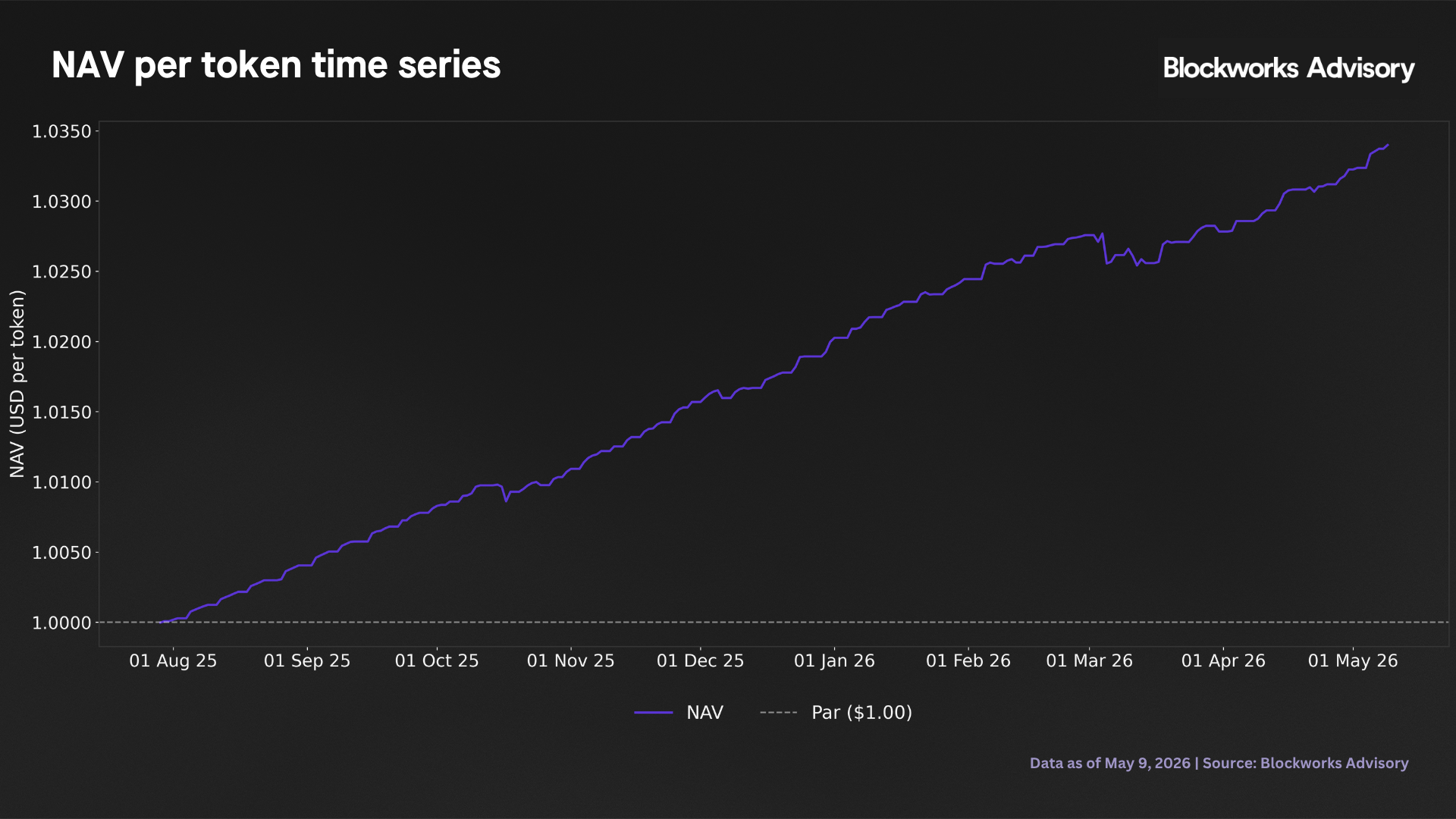

NAV trajectory

JAAA is a floating NAV fund with the token accreting from a $1.00 par issue price as CLO income accumulates, where a rising NAV above par is expected and does not constitute a breach. The credit stress scenario the peg threshold tests is the reverse, where a CLO credit event that forces AAA tranche impairment drives the NAV below par. Over 285 daily observations, the NAV moved from $1.00 at inception (July 29, 2025) to $1.03 on May 9. 2026. The maximum deviation below par is 0.22 bps, recorded at inception, which is the date of the initial subscription. There were no below-par events that occurred during the sample period.

A NAV event was reported in public communications during July 2025, and the root cause has not been confirmed in due diligence. The available circumstantial evidence that the Janus Henderson JAAA ETF did not deviate concurrently is consistent with an oracle or Centrifuge pipeline failure at the Chronicle layer. This interpretation is not entered as a factual finding, and it is the most likely mechanism pending further clarification from the issuer. A formal fair value pricing procedure exists under the supervision of a US Pricing Committee with representatives from the Office of the Treasurer, Compliance, and Trading. In the absence of evaluated prices from an approved pricing service, the US Pricing Committee determines fair value using a defined set of factors, including recent market prices, trading volumes, comparable securities, and observations from financial institutions.

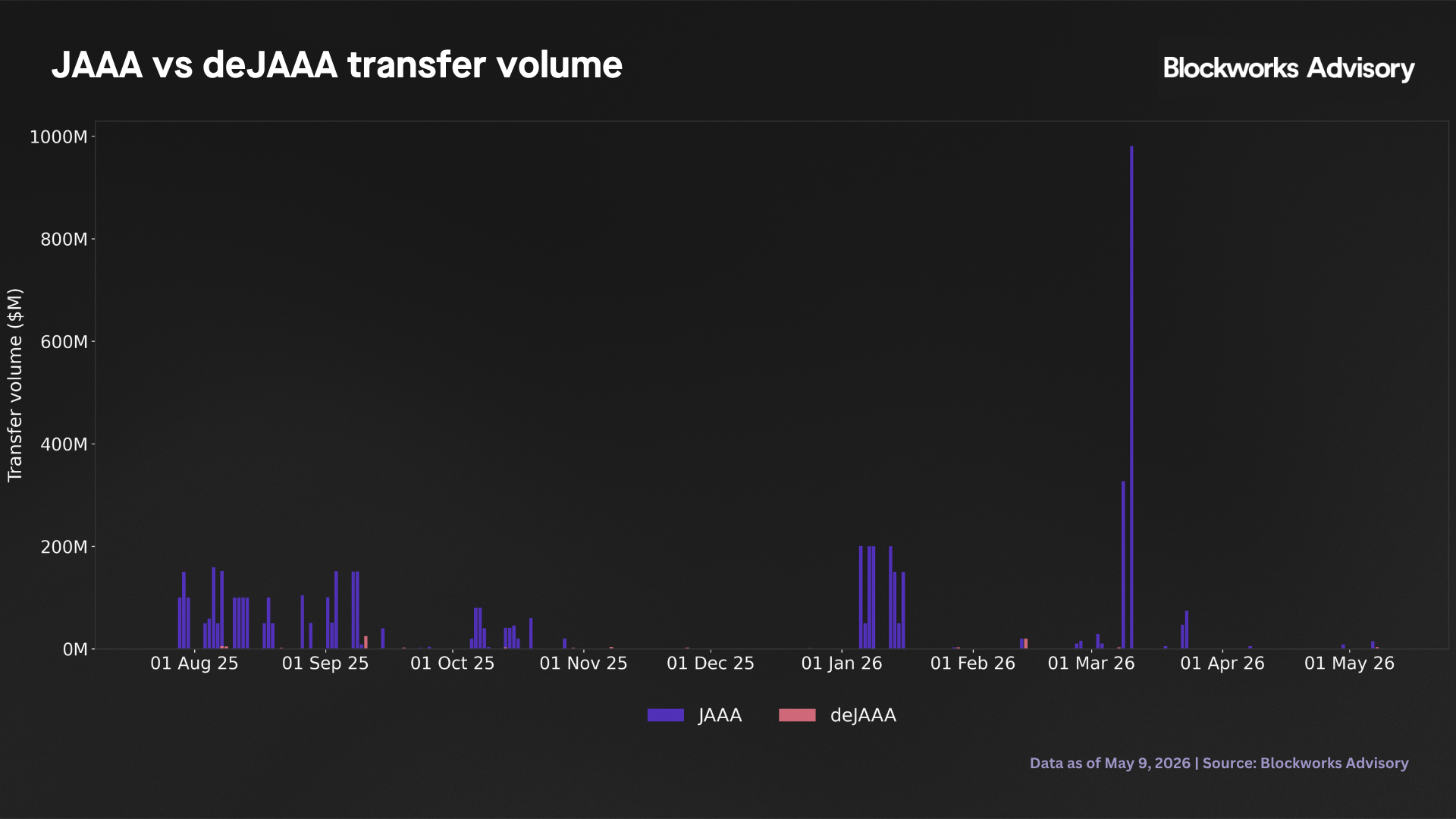

AUM trajectory and the March 2026 drawdown

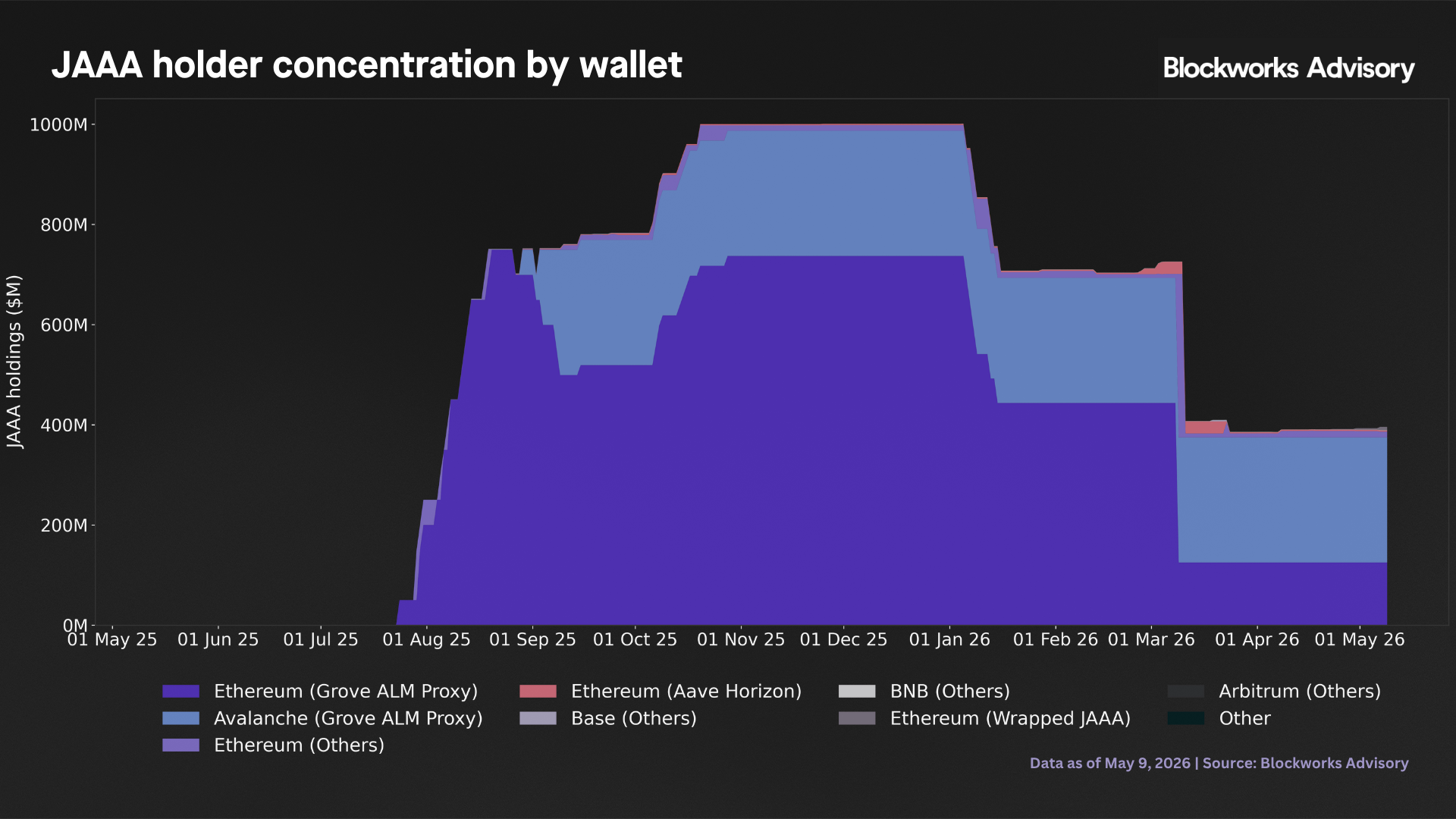

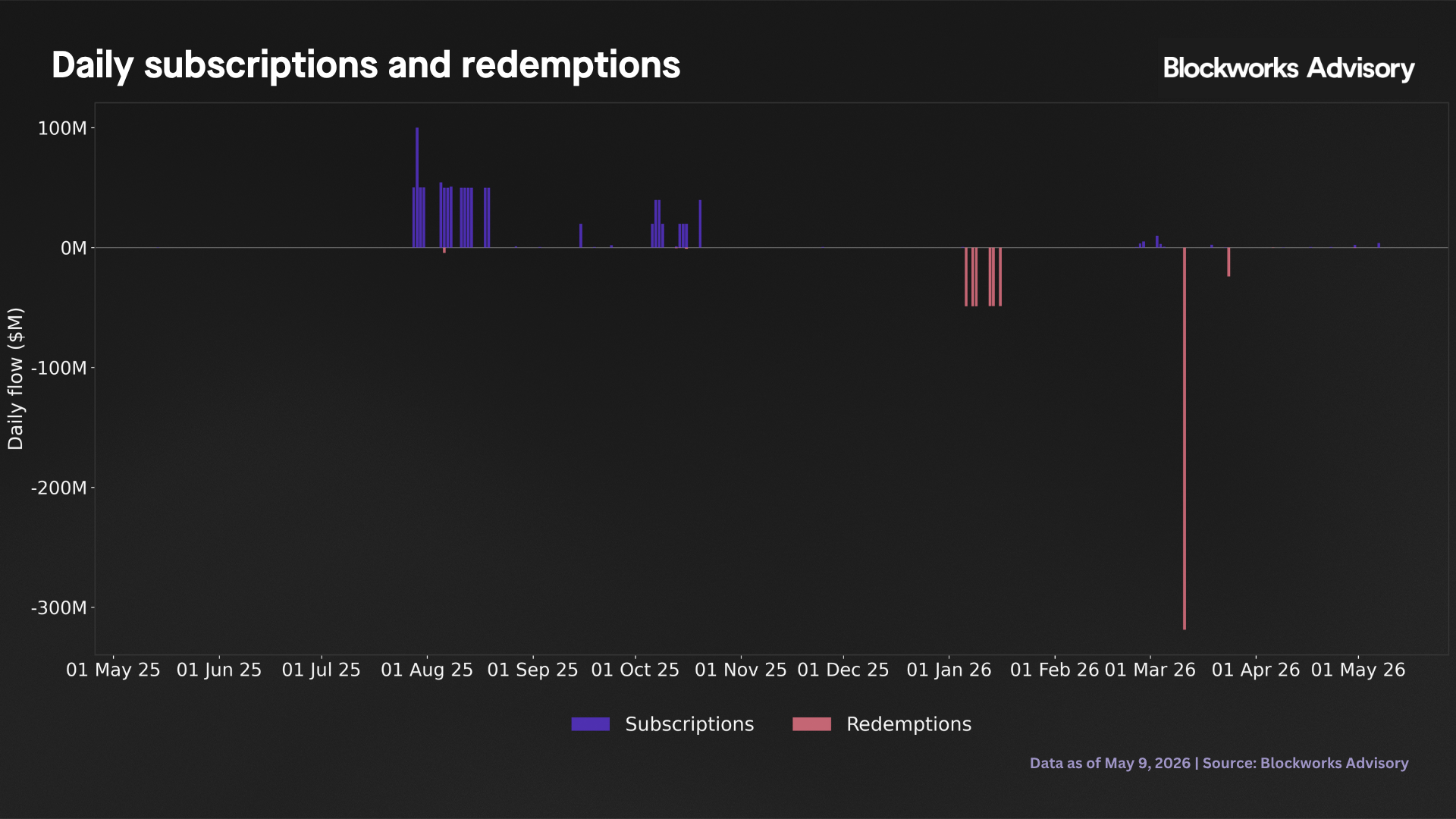

The fund grew from the $50M inception AUM on July 29, 2025, to a peak of $1,022M on Jan. 6, 2026, an increase of approximately 20-fold in five months. As of May 9, 2026, AUM stands at $409M, a peak-to-current decline of 59.96%. The decline is attributable almost entirely to a single wallet in a single day. On March 11, 2026, the wallet labelled as Ethereum (Grove ALM Proxy) submitted a redemption of $318.6M, equal to 42.8% of AUM at that date ($744.8M). This redemption, the largest single-day outflow in the sample period, was processed via a block trade with Bank of America at approximately 5 bps total execution slippage with no NAV impairment. The Avalanche (Grove ALM Proxy) wallet of $250M was not redeemed and remains the largest single holding at the analysis date.

The drawdown has two distinct phases. An initial AUM decline from $873M to $724M (-17.1%) occurred between Jan. 10 and Jan. 17, 2026, and has not been attributed to a specific wallet class in the available data. The primary event — the Grove Ethereum redemption of $318.6M on March 11, 2026 — reduced AUM from approximately $745M to approximately $426M on that single day, before stabilizing to the current level of $409M as the Avalanche Grove position remained intact. The period between the two phases shows broadly stable AUM, confirming the drawdown is event driven.

Janus Henderson provided execution details on the March 2026 redemption. The $318.6M was liquidated as a block trade with Bank of America, achieving total execution slippage of approximately 5 bps. A separate accounting correction of 6 bps at fund administrator Trident Trust related to NAV accrual timing has been resolved and will not recur. The fund applies IHS Markit bid prices for portfolio valuation, pricing to liquidation scenarios. MSCI Liquidity Metrics classifies 100% of the fund's assets as highly liquid, meaning the full portfolio can be liquidated within three business days. CLO secondary trading volume reached a record $84B in Q1 2026, with the first week of March recording $12B, the highest weekly volume on record. Janus Henderson is one of the largest CLO traders in the institutional bank market and executes block liquidations through its banking partners at pricing unavailable to smaller managers. The fund executed the $318.6M redemption in a single day with no significant performance impact. The April 2026 holdings confirm this characterization: all 20 CLO positions remain AAA rated, and the portfolio weighted average price is $100.12, demonstrating that the redemption was executed without lasting impairment to the remaining portfolio.

Carry economics

The fund's carry is measured from the daily NAV-based return, applying ACT/365 annualization. The epoch settlement cycle produces extreme daily return observations with the series running from -53.22% to +55.48% with a standard deviation of 9.85%, values inconsistent with a AAA CLO fund on any given day. The mean daily observation is 4.87% annualized, and the median is 2.91%. The 30-day moving average at the analysis date is 6.83%, and the 7-day moving average is 9.34%, both reflecting the most recent settlement cycle. The carry sustainability criterion, the frequency of negative daily carry, passes comfortably with 18 of 285 days (6.3%) recorded negative daily carry, all on non-settlement days when the daily return rounds to zero or marginally below due to fee accrual.

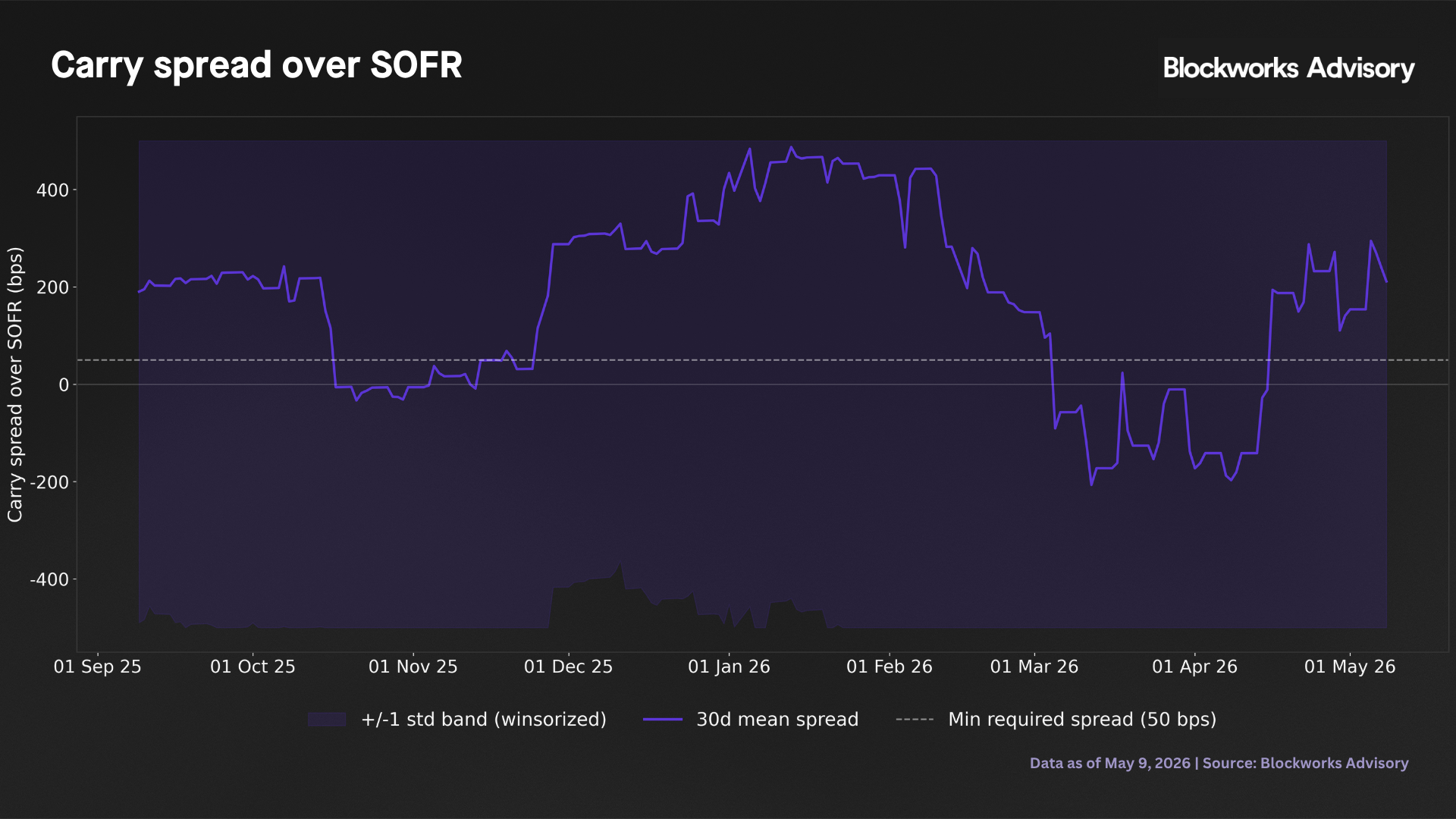

Carry spread over SOFR

The carry spread is assessed using two methods. The daily method computes (ethereum_apy − sofr_rate) × 10,000 for each observation. The daily median of 28.34 bps falls below the 50 bps floor, driven by the epoch settlement artifact: among the 80% of days with no income recognition, the daily return rounds near zero against continuously accruing SOFR. The quarterly NAV-based method, which eliminates this artifact, is the primary assessment.

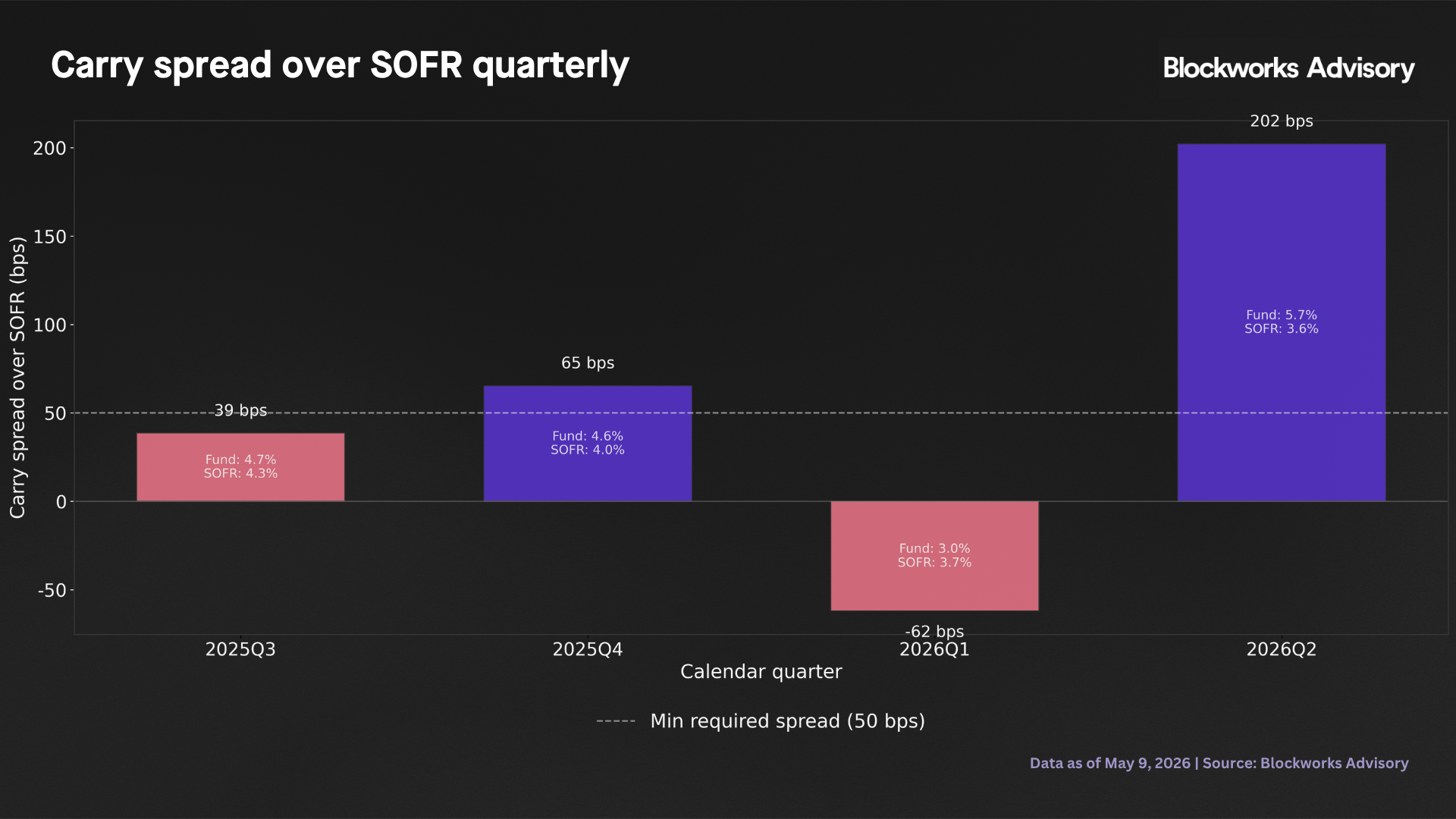

The quarterly assessment computes the fund’s holding period return (NAV₂ / NAV₁ − 1, annualized ACT/365) for each calendar quarter and subtracts the average SOFR over the same period. Results are Q3 2025 (partial, 63 days) +38.6 bps; Q4 2025 (91 days) +65.4 bps; Q1 2026 (89 days) −62.0 bps; Q2 2026 (partial, 37 days) +202.2 bps with a mean quarterly spread of 61.1 bps. The negative Q1 2026 observation (−62.0 bps) is economically real since it coincides with the Grove redemption stress period, during which SOFR averaged 3.66% against a fund return of only 3.04% annualized. This quarter is a genuine below SOFR observation and should be monitored in future assessments. SOFR declined from approximately 5.3% in mid-2025 to 4.3% in May 2026; the fund’s income accrual tracked this decline but with a lag reflecting the floating rate reset schedule of the underlying CLO tranches.

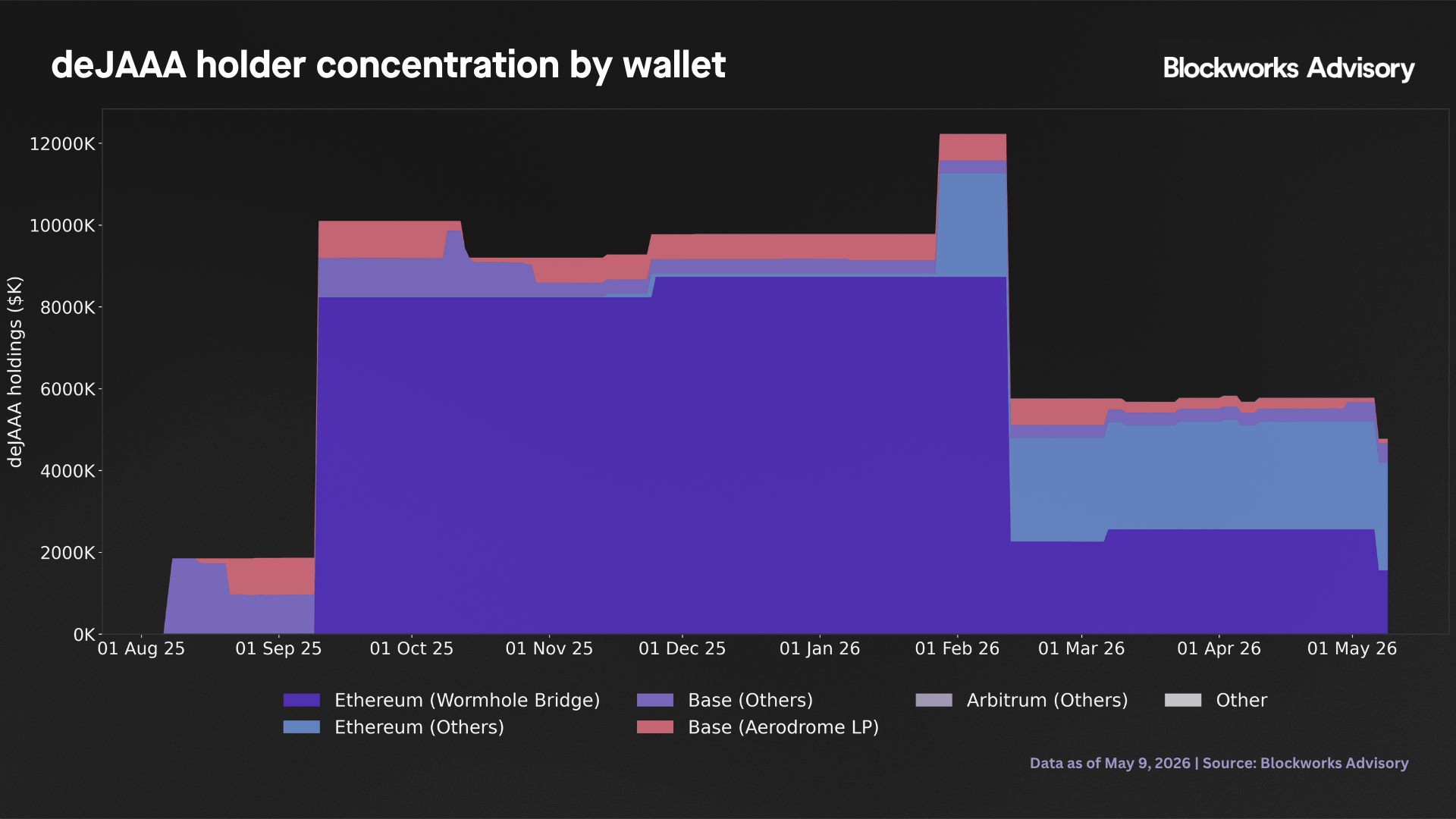

Holder concentration and run risk

Concentration

The holder snapshot at May 9, 2026, is presented below. Note that the holder snapshot totals $396M while the AUM series shows $409M; the $13M discrepancy reflects the different timing of the two data pipelines and does not affect the concentration percentages, which are computed within each dataset.

| Wallet class | Balance | Share (%) | Cumulative (%) |

|---|---|---|---|

| Avalanche Grove ALM Proxy | $250,000,000 | 63.15 | 63.15 |

| Ethereum Grove ALM Proxy | $124,807,013 | 31.53 | 94.68 |

| Ethereum others | $11,298,318 | 2.85 | 97.54 |

| Ethereum Wrapped JAAA | $6,771,372 | 1.71 | 99.25 |

| Ethereum Aave Horizon | $2,482,956 | 0.63 | 99.87 |

| BNB others | $489,708 | 0.12 | 100.00 |

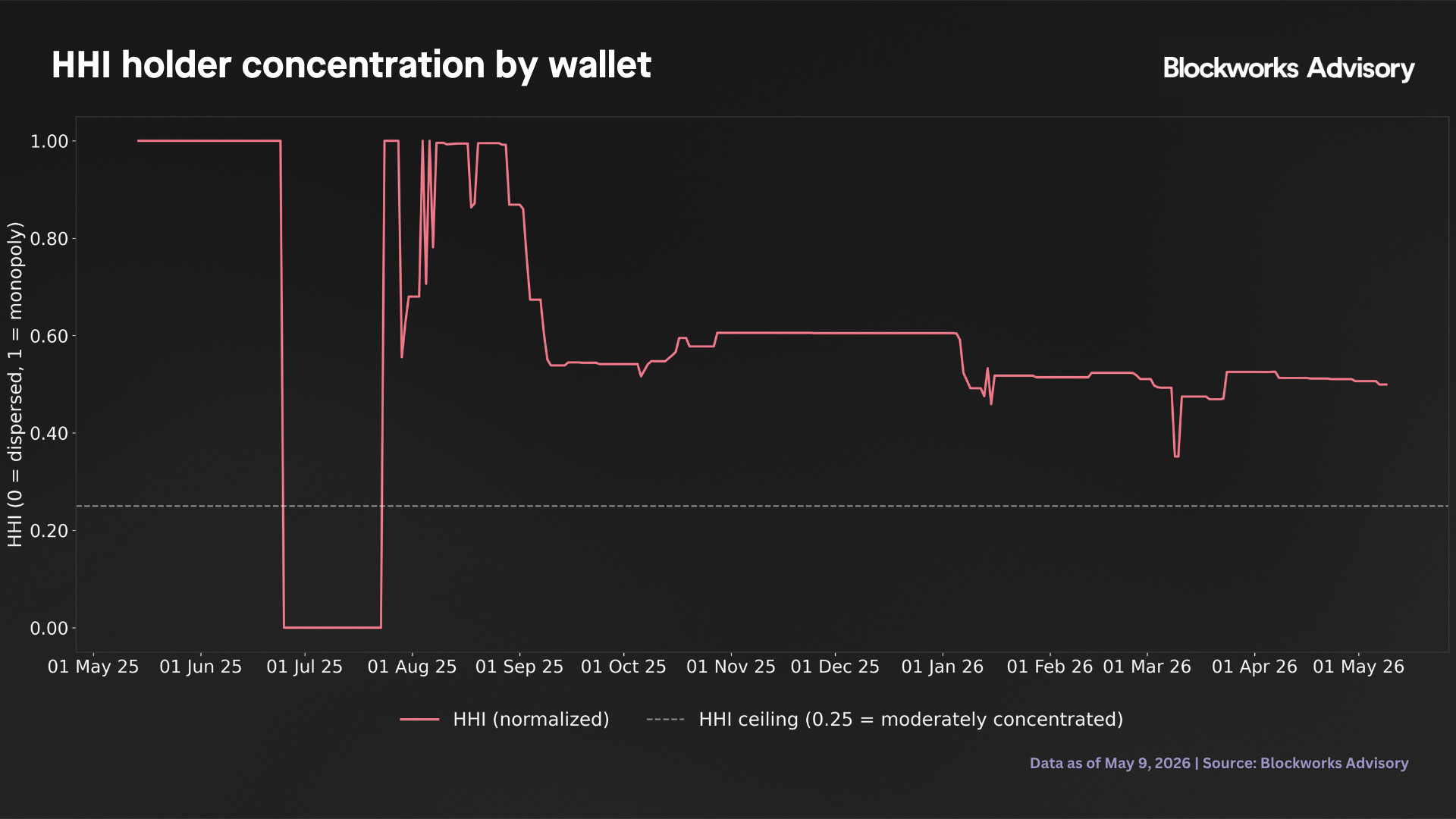

The two Grove ALM Proxy wallets combined hold $374.8M of $395.9M snapshot total, representing 94.68%, and the Herfindahl Hirschman Index of 49.9% against a 25% framework reference level. The Gini coefficient of 0.7878 places the fund in the extreme concentration range (above 0.60 is classified as high). Concentration has been consistently severe across all quarterly observations since inception, peaking at HHI 60.5% in December 2025 when Grove's Ethereum wallet held 73.65% alone, before declining modestly following the March 2026 redemption.

The AUM concentration cliff (-59.96%), the 42.8% single-day outflow, and the top five holder share of 99.87% are arithmetic consequences of the same concentrated investor base. The run risk event is directly attributable to the Grove Ethereum wallet redemption of 11 March 2026, which was executed without queue congestion or NAV impairment at 5 bps execution slippage. These metrics are monitoring inputs and would improve automatically as the investor base diversifies.

March 2026 redemption attribution

The February to April 2026 window covers the primary drawdown event. The Ethereum Grove wallet balance fell from $443.4M to $124.8M, a reduction of $318.5M, representing 99.7% of the $319.4M total AUM decline over this period. The Ethereum Aave Horizon wallet (Resolv's position) declined by $9.0M, contributing 2.8%. These two events are structurally independent, where Grove's redemption preceded the Resolv exploit by eleven days (March 11 versus March 22, 2026). The Avalanche Grove wallet of $250M was unchanged across this window.

The $250M Avalanche wallet represents a latent overhang at the analysis date. With a current AUM of $409M, a redemption of this wallet would represent 61.1% of AUM, a larger proportional event than the March 11 redemption (42.8%). The forward redemption intentions of Grove have not been obtained.

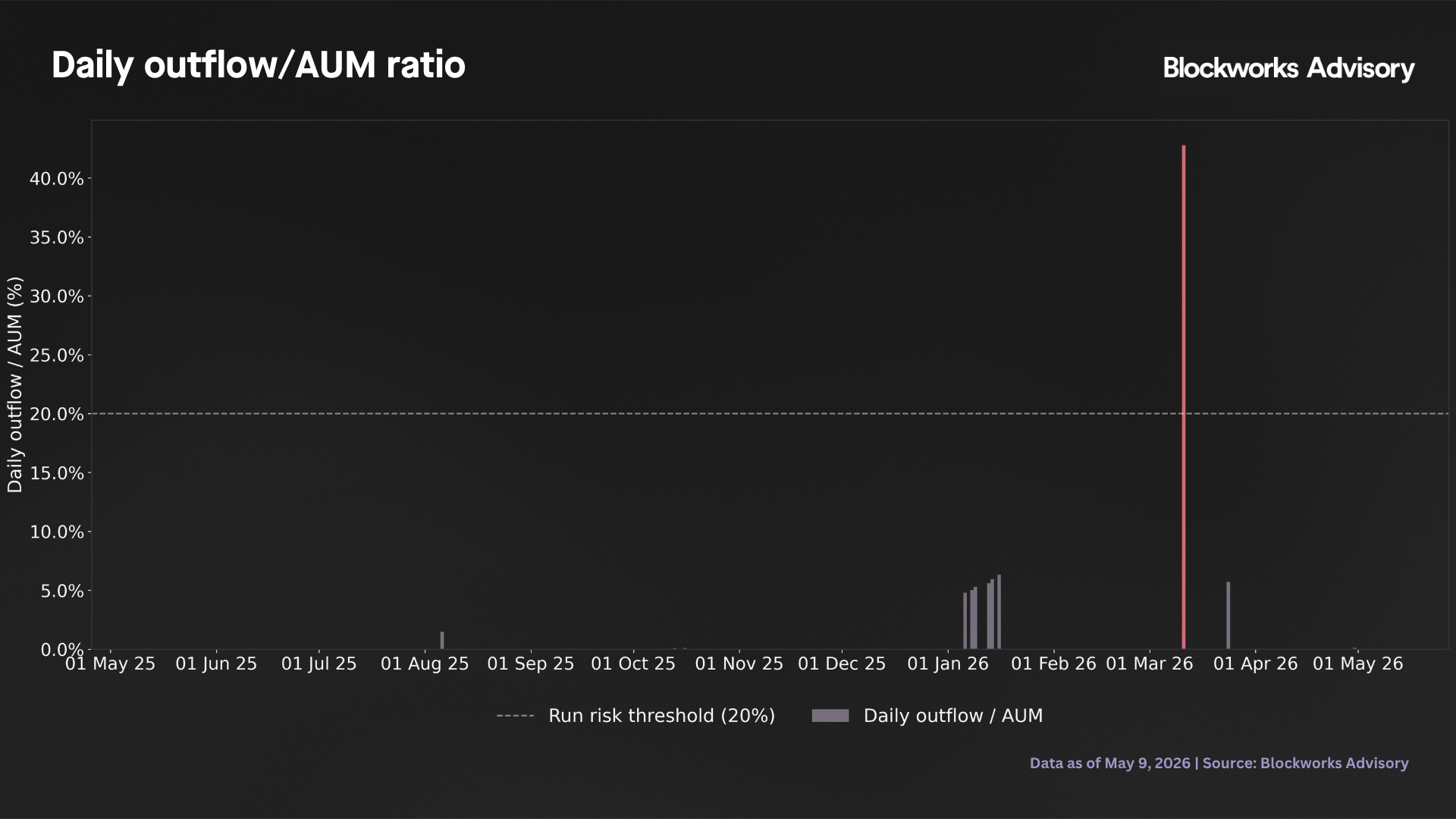

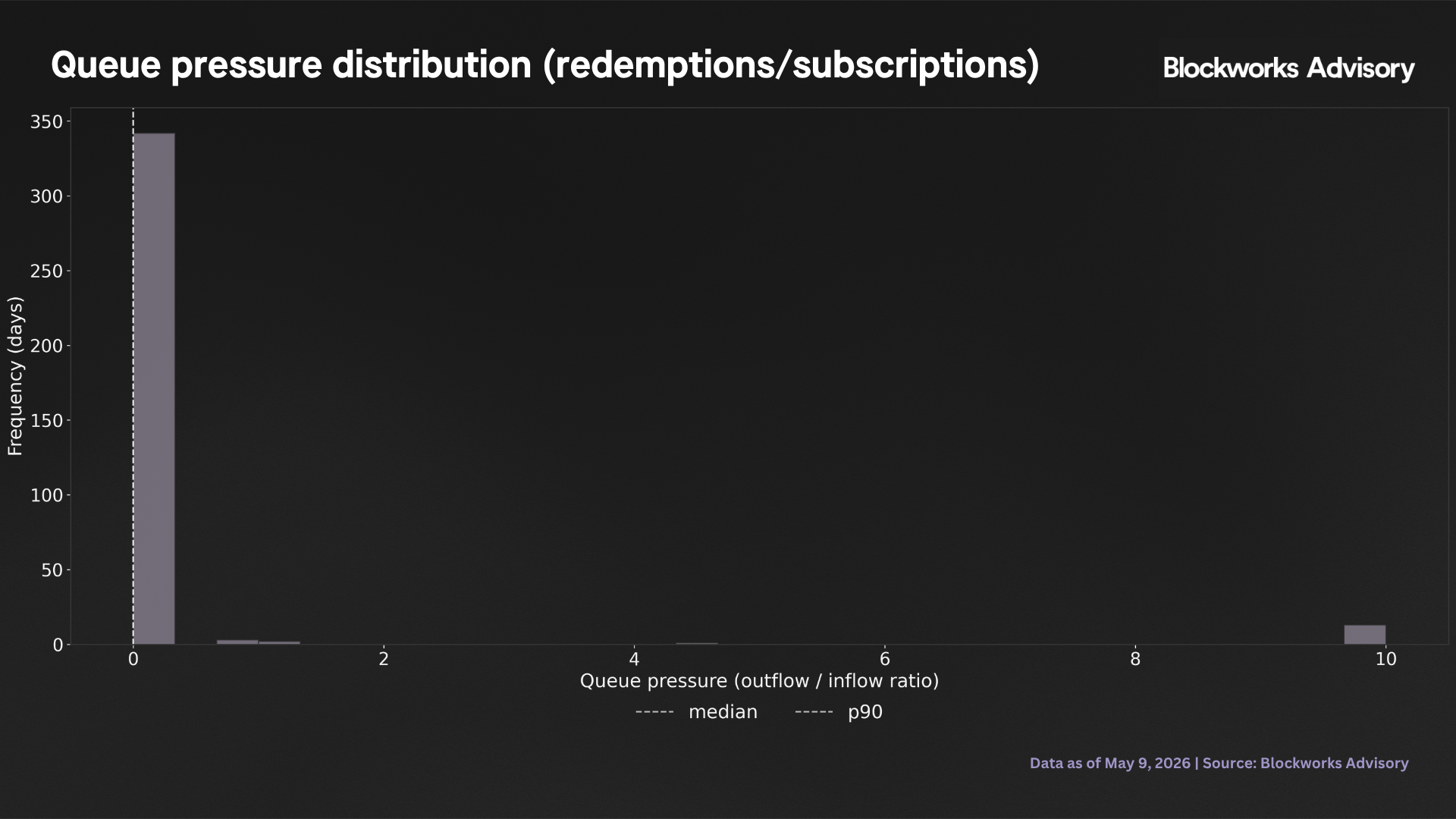

Run risk

Mean daily subscriptions are $9.4M, and the mean daily redemptions are $5.8M, giving a mean net daily inflow of $3.5M. The maximum single-day outflow as a percentage of AUM is 42.78% ($318.6M/$744.8M) on March 11, 2026, more than double the 20% framework threshold. The March 2026 event demonstrated that a 42.8% single-day outflow can be processed without queue congestion or NAV impairment at a total execution cost of 5 bps. With no formal daily redemption limits and JPMorgan as the execution counterparty, concurrent redemption scenarios are operationally manageable. The $250M Grove Avalanche wallet represents a latent overhang and is a monitoring trigger; in absolute dollar terms, it is below the $318.6M single-day execution precedent, and its existence does not constrain Ethena's ability to redeem its own position.

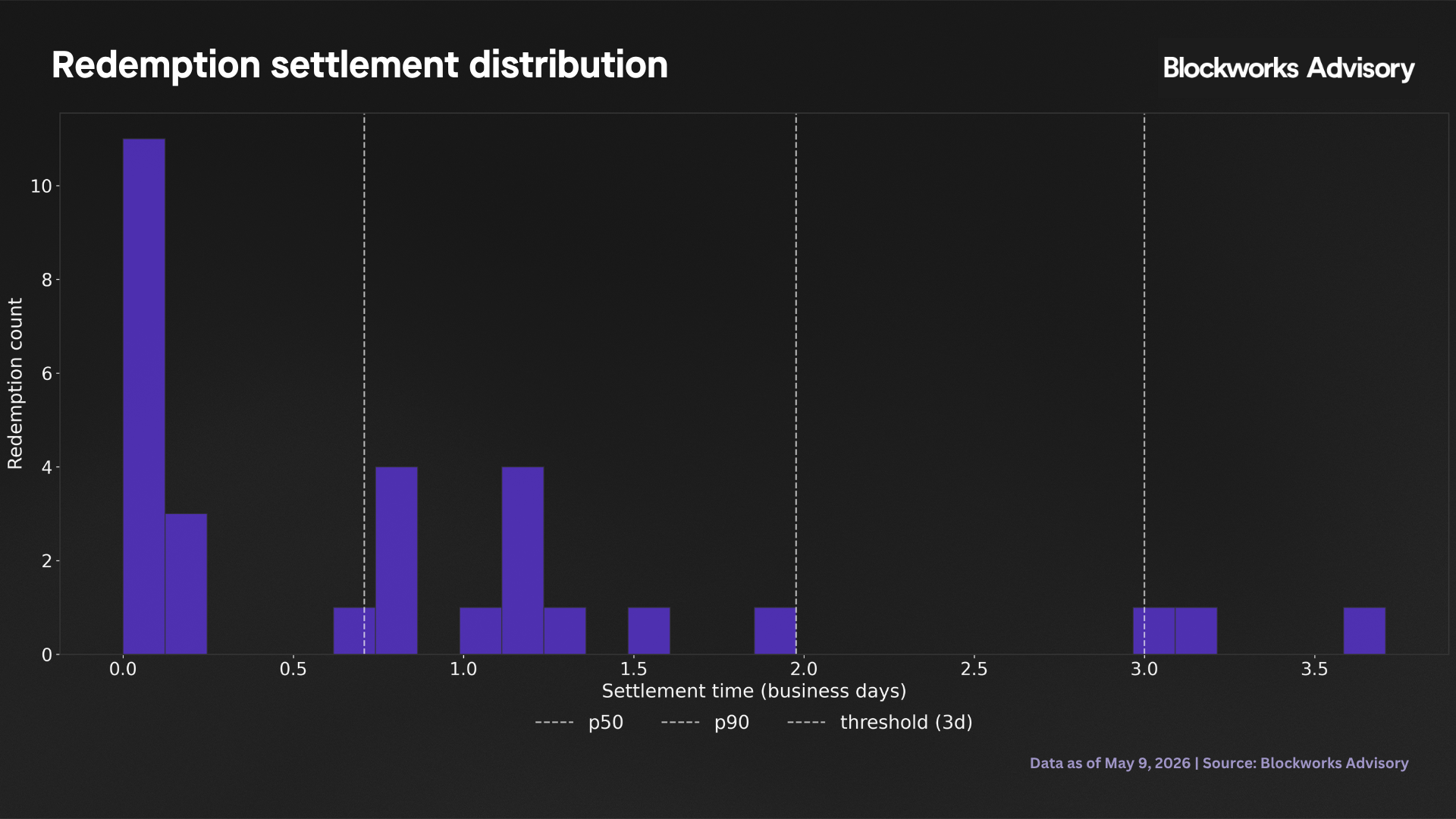

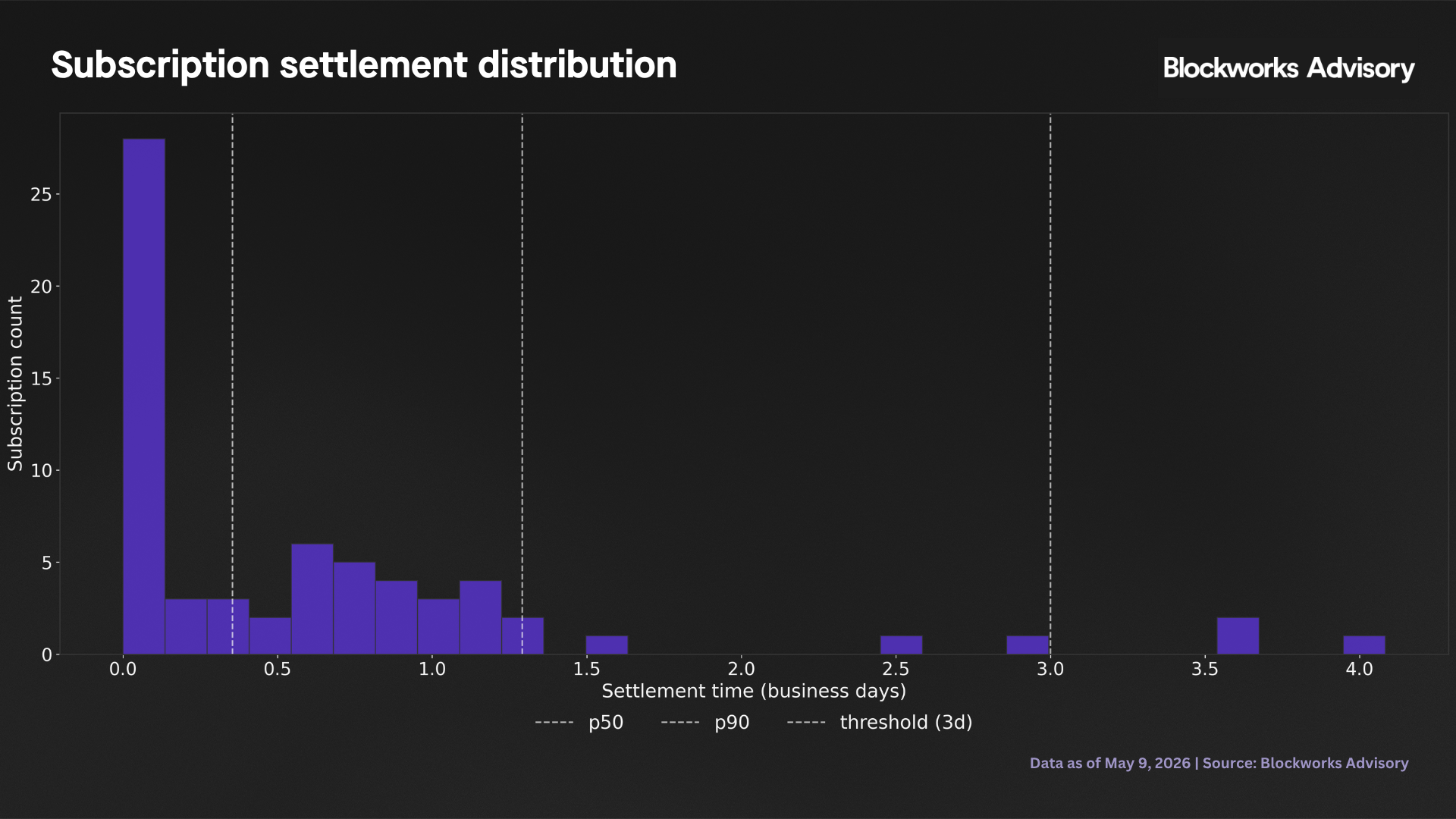

Settlement mechanics and redemption throughput

Redemption settlement data: 30 epoch-level observations, with settlement measured in business days using Monday to Friday convention. The P90 of 1.98 business days and a maximum of 3.71 business days both pass the framework thresholds of three and five days, respectively. Subscription settlement (66 observations) is faster with P90 of 1.29 days and a maximum of 4.08 days. The Mann-Kendall trend test on redemption latency returns τ = 0.078, p = 0.554, indicating no statistically significant trend.

The 30-observation redemption sample is sparse for statistical inference where the P90 estimate carries qualification. More importantly, the observed settlement times reflect single actor or lightly contested epoch cycles. No formal daily redemption limits apply. Concurrent redemption requests are processed on a prorata basis in the unlikely event that operational constraints were to arise, though this scenario has not occurred in the fund's operating history.

| Metric | Redemption | Subscription | Threshold | Notes |

|---|---|---|---|---|

| P90 settlement (business days) | 1.98 | 1.29 | ≤ 3.0 | n=30 redemption; n=66 subscription |

| Maximum observed (business days) | 3.71 | 4.08 | ≤ 5.0 | single tail event each |

| % exceeding 3 days | 10.0% | 4.6% | < 20% | 3 of 30; 3 of 66 |

| % exceeding 5 days | 0.0% | 0.0% | < 5% | no observations above 5 days |

| Mann-Kendall trend | τ=0.08, p=0.55 | No clear trend | No trend | no worsening; low power at n=30 |

| Contractual SLA | T+1 target, 2pm ET | T+1 target, 2pm ET | T+1 | no formal capacity limits; T+3 contractual SLA; T+1 target; investor notification via Telegram and email if delayed |

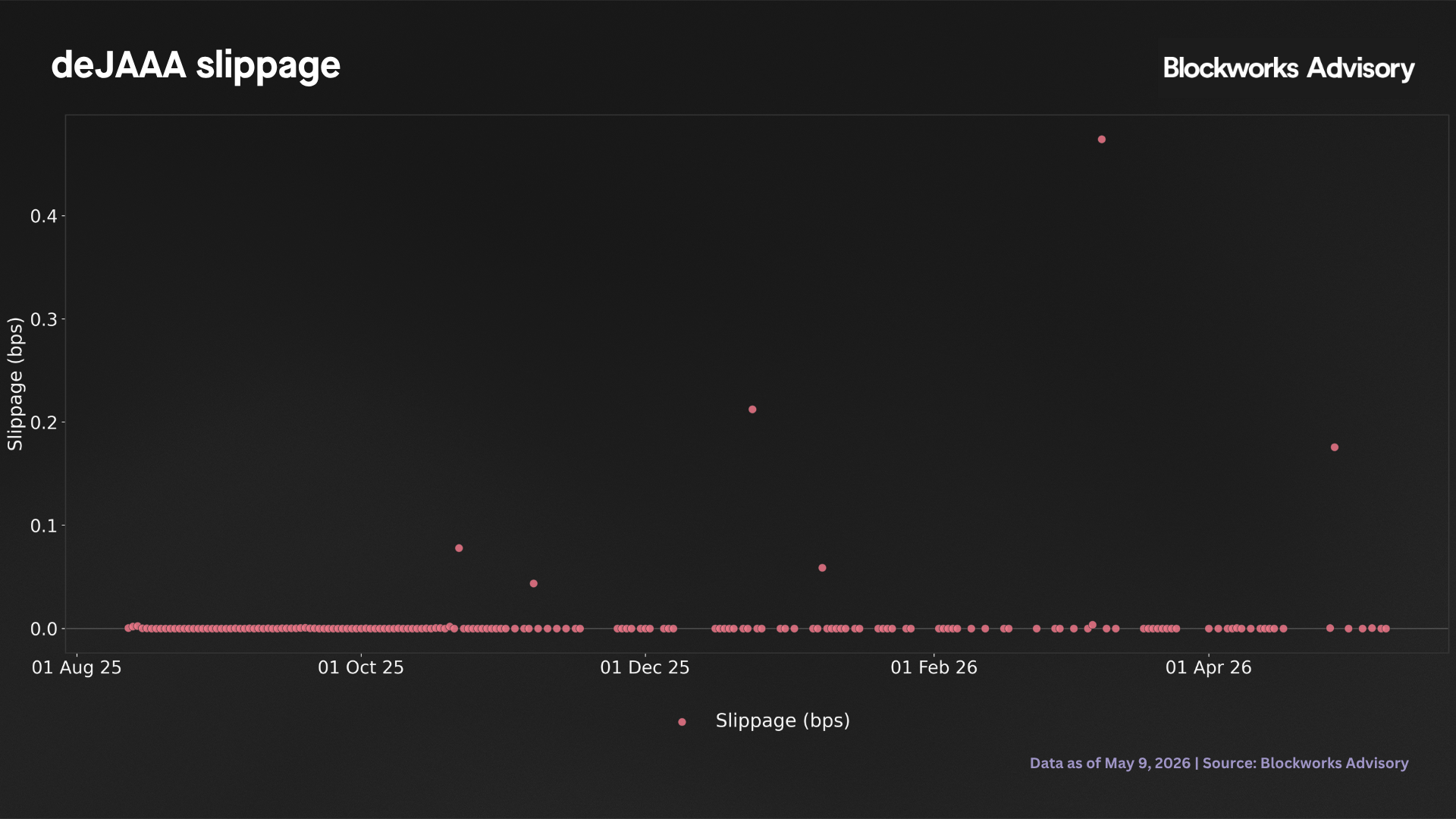

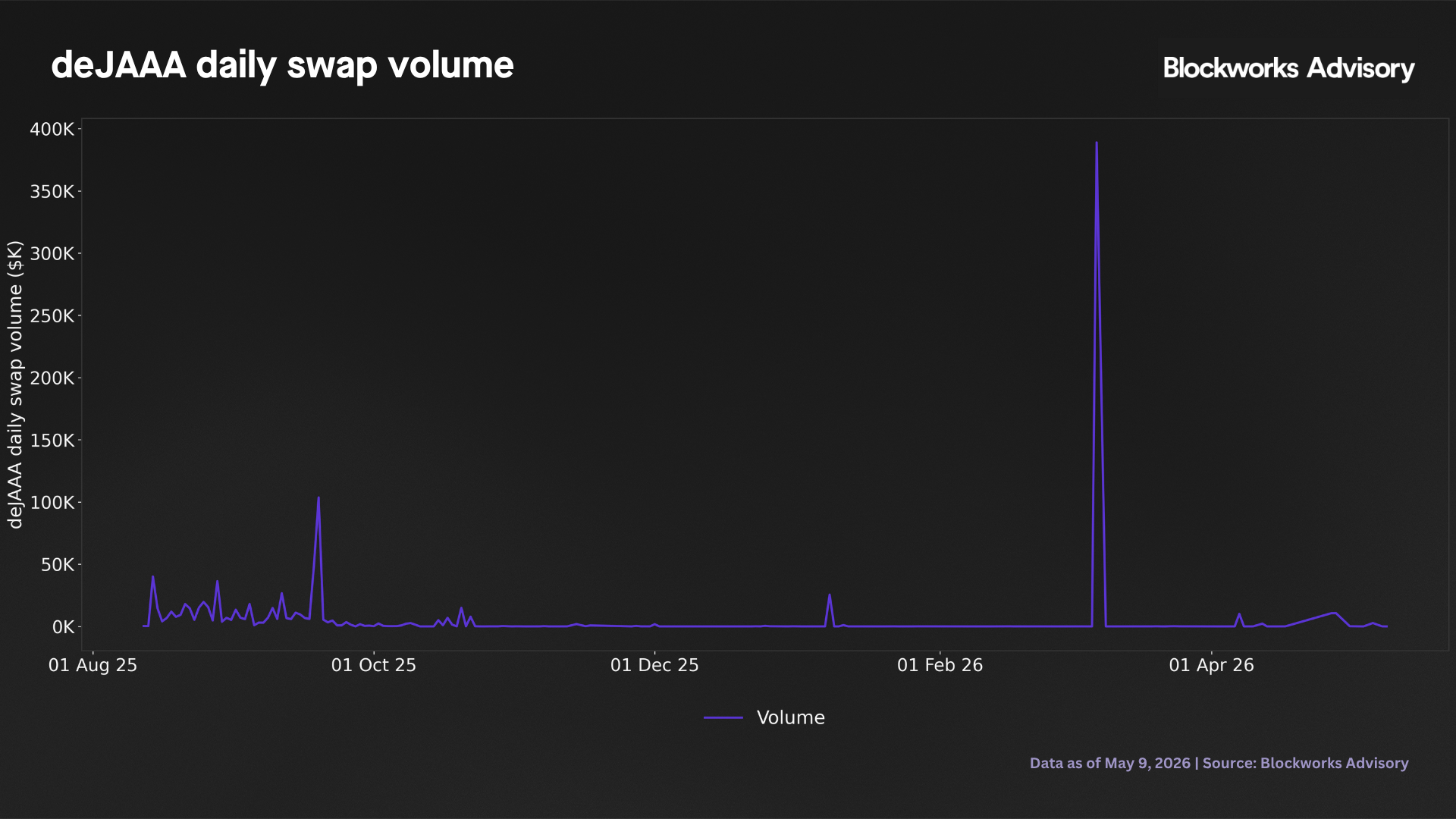

Secondary market liquidity

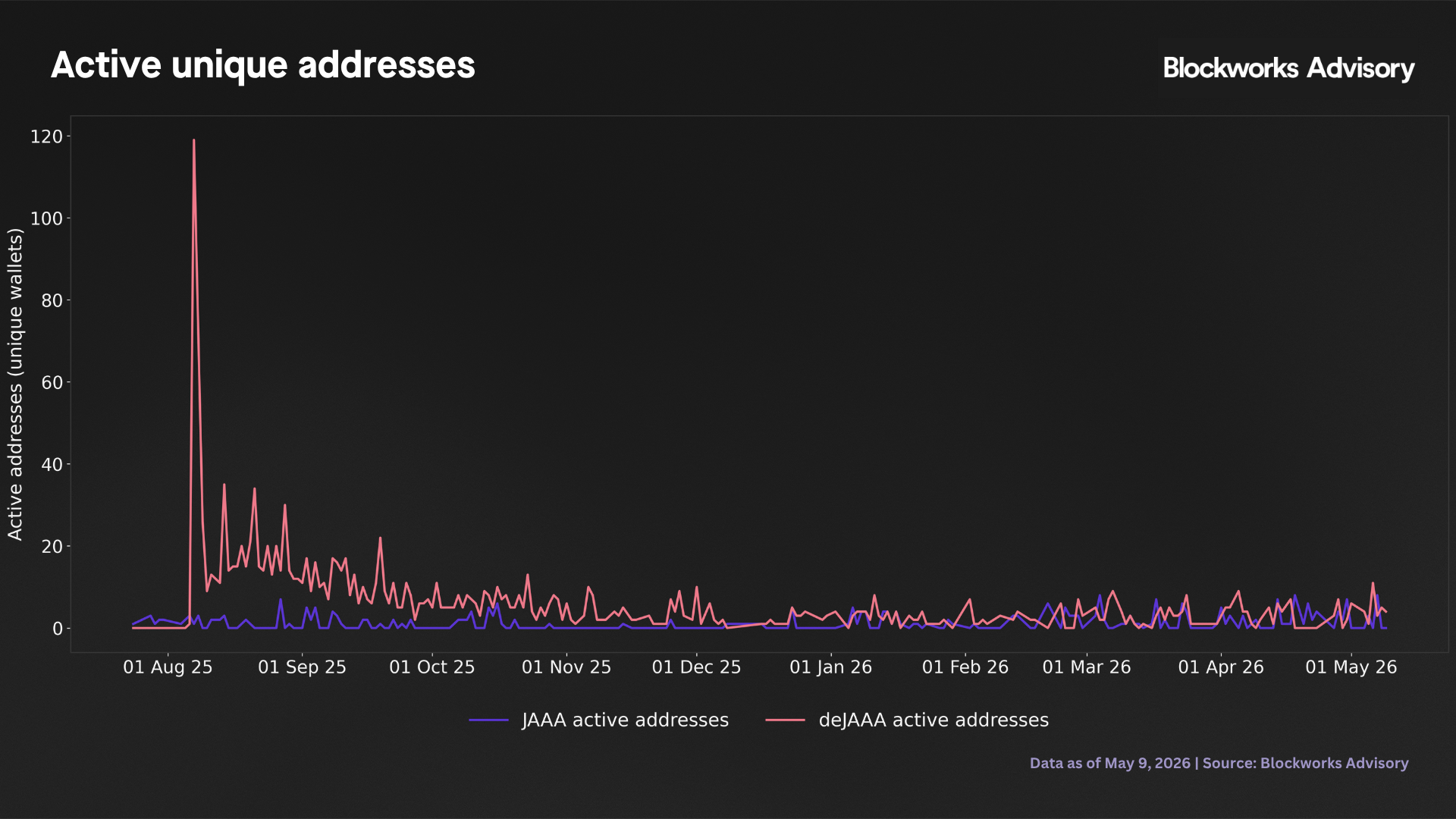

The deJAAA token trades on Aerodrome Finance (Base) and related venues. The median pool depth is $257K against a framework floor of $1M. The pool depth fails the threshold on all 176 observed days, with the maximum depth observed being $744K on a single day in January 2026 and the remainder of the distribution consistently below $400K.

The maximum position exitable via the deJAAA secondary market without exceeding the 100 bps slippage ceiling computed as median depth × (100 bps/200 bps) under a linear price impact approximation is $128K. An intended initial position of $250M cannot be liquidated via the secondary market under any realistic scenario. The primary redemption queue is the appropriate exit mechanism for any meaningful position, with confirmed unlimited daily capacity and a T+1 settlement target.

The recorded slippage is technically zero on all observed days and reflects the absence of meaningful trading activity. The daily volume shows non-zero trading on 79 of 228 days (34.6% of the sample), and on active days the pool processes small rebalancing swaps, not a meaningful exit volume.

Cross-chain architecture

JAAA transfer volume is 95.0% Ethereum by total USD volume over the sample period, with Avalanche at 4.6%, Base at 0.3%, and BNB Chain below 0.1%. The Ethereum dominance in volume is consistent with the holder snapshot, where all Grove wallets and the Aave Horizon position are Ethereum-based. The Avalanche wallet ($250M, Grove) generates relatively little transfer volume despite its large balance, suggesting a hold-not-trade posture consistent with a single institutional investor.

The Centrifuge protocol team has been asked to provide detail on the cross-chain bridge adapter architecture (this response is pending). The April 2026 rsETH exploit on KelpDAO confirmed that cross-chain message forgery via a compromised adapter can drain bridged RWA positions at scale. JAAA's Avalanche deployment represents the highest concentration risk point at $250M. Until the specific adapter set and quorum are confirmed, this risk cannot be quantified.

Wrong way risk

Resolv Protocol held a $100M JAAA position on Aave Horizon and Centrifuge as of March 2026, confirmed by public reporting and by the onchain holder data (Ethereum Aave Horizon wallet balance of $11.4M in February 2026, consistent with incremental position drawdown from the full $100M). This was the largest RWA loop trade in DeFi at that time.

On March 22, 2026, Resolv was exploited via compromise of an offchain AWS KMS signing key. The attacker minted approximately $80M in unbacked USR tokens against minimal USDC deposits, causing USR to depeg to approximately $0.025. Resolv paused all protocol functions and became insolvent ($95M assets versus $173M liabilities at the analysis date per public reporting). JAAA's underlying CLO portfolio was not impaired; NAV accreted through the event without deviation. The redemption queue pressure arose from the insolvency wind-down process.

The Ethereum Aave Horizon holder balance declined from $11.4M in February 2026 to $2.5M in May 2026, implying $8.9M in post-exploit redemptions. The remaining $91.1M requires a full wind-down resolution. These redemptions flowed through the standard primary queue and are visible in the flow data as incremental redemption activity after March 22, 2026, distinct from the Grove event of March 11, 2026.

The analysis was designed to model a credit stress pathway where CLO NAV decline drives an LTV breach at Aave Horizon, forcing liquidation and queue pressure. The formula (1 - entry_LTV / trigger_LTV) × 100 = (1 - 0.80 / 0.875) × 100 = 8.57% defines the NAV decline required to reach the liquidation trigger from the 80% entry LTV. This trigger was not reached, and the Resolv event followed a wholly different mechanism.

| Pathway | Trigger mechanism | Queue pressure | Status |

|---|---|---|---|

| LTV triggered liquidation (modeled) | JAAA NAV falls 8.57% from entry -> entry LTV 80% reaches trigger LTV 87.5% | $100M | Not triggered CLO portfolio intact; NAV declined 0.22 bps, far from trigger |

| Protocol insolvency via exploit (observed) | offchain key compromise -> unbacked USR minting -> USR depeg -> insolvency -> orderly wind down | $100M | Partially realized $8.9M redeemed post-exploit; full $100M wind down ongoing |

The calibration implication is material where the 8.57% NAV decline trigger is not a reliable predictor of when leveraged JAAA positions generate redemption queue pressure. A protocol security failure structurally unrelated to CLO credit quality produced equivalent queue pressure with JAAA NAV at par. Future eligibility criteria should require a monthly mapping of all known third-party leveraged JAAA positions on lending protocols, updated before any cap decision.

Carry regime stress matrix

The 30-day P&L matrix for a $250M Ethena position under four carry and outflow scenarios is presented below. Carry income uses the 30-day moving average (14.73% annualized, the economic signal) for the HIGH regime and the 5th percentile (-3.83%) for LOW. Effective P90 settlement under HIGH outflow is doubled from 2.0 to 4.0 business days, reflecting a conservative stress assumption. Exit friction is 20 bps round trip. All values are model dependent.

| Scenario | Carry (%) | Eff. P90 (d) | Carry income | Queue cost | Net P&L (30d) |

|---|---|---|---|---|---|

| HIGH_CARRY × LOW_OUTFLOW | 14.73 | 2.0 | +$3.05M | -$0.20M | +$2.35M |

| HIGH_CARRY × HIGH_OUTFLOW | 14.73 | 4.0 | +$3.05M | -$0.40M | +$2.15M |

| LOW_CARRY × LOW_OUTFLOW | -3.83 | 2.0 | -$0.80M | -$0.05M | -$1.35M |

| LOW_CARRY × HIGH_OUTFLOW | -3.83 | 4.0 | -$0.80M | -$0.10M | -$1.40M |

Framework scorecard

The scorecard applies 14 data-available criteria. The fund passes all primary eligibility criteria, including NAV stability, redemption settlement speed, carry sustainability, carry spread over SOFR, and confirmed unlimited redemption capacity. One criterion record fails on the defined thresholds, which is deJAAA pool depth. Three concentration criteria, i.e., HHI, top one holder share, and top five holder share, exceed their framework thresholds and are classified as monitoring inputs given confirmed unlimited redemption capacity. The run risk criterion is classified as a pass based on the confirmed execution of the 42.8% single-day outflow without NAV impairment or queue congestion. The carry spread criterion passes under the quarterly NAV-based methodology (mean 61.1 bps, above the 50 bps floor), though Q1 2026 recorded a genuine negative spread of −62.0 bps. The redemption capacity criterion passes; the fund operates with no formal daily limits, a T+1 settlement target, and JPMorgan as custodian and execution counterparty. The overall determination is eligible as a USDe backing asset.

| Criterion | Threshold | Observed | Status | Notes |

|---|---|---|---|---|

| NAV peg stability (bps below par) | < 100 | -0.22 | PASS | Zero below par days; 0.22 bps at inception only |

| NAV time below peg (consecutive days) | ≤ 3 | 0 | PASS | |

| Carry sustainability (% negative days) | < 25% | 6.3% | PASS | 18 of 285 days; max consecutive streak 2 days |

| Carry spread to SOFR (quarterly mean, bps) | ≥ 50 | 61.07 | PASS* | Carry passes quarterly methodology (mean 61.1 bps). Q1 2026 recorded genuine negative spread. |

| Redemption P90 (business days) | ≤ 3 | 1.98 | PASS | n=30 observations; directional only |

| Redemption maximum (business days) | ≤ 5 | 3.71 | PASS | Single tail event |

| Run risk: max outflow/AUM (%) | No NAV impairment; no queue congestion | 42.78% processed at 5 bps; no impairment | PASS | 42.8% single-day outflow on 11 March 2026 executed at 5 bps slippage via BofA block trade; no queue congestion; no NAV impairment; noted for cap sizing |

| AUM concentration cliff (peak to current %) | < 30% | -59.96% | MONITOR | 59.96% peak to current reflects Grove redemption; no impairment to remaining holders; cap sizing consideration |

| Holder HHI | < 25% | 49.9% | MONITOR | Confirmed unlimited redemptions and demonstrated execution quality mitigate queue pressure risk; monitor for position sizing |

| Top 1 holder share (%) | < 25% | 63.15% | MONITOR | $250M Avalanche wallet is active monitoring item; position sized at $250M based on redemption capacity |

| Top 5 holder share (%) | < 60% | 99.87% | MONITOR† | †Derivative; arithmetic consequence of top-1 = 63% and top-2 = 95%; cap sizing context only |

| deJAAA pool depth (median, $M) | > $1.0M | $0.26M | FAIL | Primary redemption queue has confirmed unlimited capacity; deJAAA secondary market provides supplementary liquidity for smaller amounts only |

| deJAAA slippage (median, bps) | < 100 | 0 | PASS | Reflects zero trading activity; zero trading days not benign market conditions |

| Wrong way risk: Resolv (pressure ratio) | < 2× | 0.31× | PASS | Resolv wind down is an out-of-sample realization of operational stress |

| Portfolio look through (100% AAA) | 100% AAA | Confirmed 100% AAA | PASS | 20 CLO positions all AAA rated at origination and current date as of April 2026; WAP $100.12; zero non-AAA holdings |

| Redemption capacity (primary) | No limits | No formal limits (T+1 target) | PASS | No daily limits; not missed since JPMorgan migration |

Eligibility determination: Eligible

Recommendation: The $250M Grove Avalanche wallet overhang and the $91M Resolv wind down position are monitoring items noted in the cap derivation below. The initial allocation cap recommendation is $250M since there are no formal redemption limits, and the March 2026 execution confirmed $318.6M can be processed in a single day at 5 bps with no NAV impairment. The constraint on position sizing is not operational capacity. If Ethena subscribes $250M, pro forma AUM rises to approximately $659M, and Ethena holds 37.9%. If Grove subsequently redeems its $250M Avalanche position, remaining AUM falls to approximately $409M and Ethena's share rises to 61.1%; the absolute redemption requirement of $250M remains below the $318.6M single-day execution precedent, so Ethena's exit capacity is not impaired by this scenario. The cap should scale above $250M as Grove concentration resolves and new investors reduce Ethena's residual share, lowering Ethena's post-Grove exit share below the 61.1% level observed at this cap.

Risk considerations

Anchor holder cliff risk

Grove controls 94.7% of JAAA AUM through two onchain wallets. The remaining non-Grove investor base of $21M (5.3% of AUM) means Grove's continued participation is central to the fund's current scale. A decision by Grove to exit the Avalanche position would represent 61.1% of the current AUM proportionally, though the $250M absolute amount is below the $318.6M single-day execution precedent established in March 2026. Given the demonstrated execution of $318.6M at 5 bps slippage and MSCI's classification of 100% of assets as highly liquid, a $250M Ethena position is below the demonstrated single-day execution ceiling and does not introduce execution risk beyond the March 2026 precedent.

Epoch measurement and carry criterion

Monthly epoch income recognition is a feature of Centrifuge’s settlement architecture. The quarterly NAV based methodology has been implemented to address this with the mean quarterly spread of 61.1 bps over SOFR passing the 50 bps floor. The Q1 2026 observation of −62.0 bps is economically real and reflects a period when SOFR (3.66%) exceeded the fund’s annualized return (3.04%) during the March 2026 redemption stress. The carry criterion should be monitored quarterly going forward, where a sustained pattern of negative spread quarters would constitute a genuine economic concern requiring further investigation.

Cross-chain bridge security

JAAA's Avalanche deployment ($250M Grove wallet) is the highest concentration bridge risk point. A compromise of the cross-chain adapter serving Avalanche could expose this holding to forced movement at scale. The April 2026 rsETH precedent demonstrates that forged cross-chain messages can drain RWA positions without any action by the legitimate holder. The Centrifuge protocol team's response on adapter architecture is a prerequisite before any cross-chain JAAA holding is considered.

Resolv wind down and third-party leverage precedent

With approximately $91M of Resolv's confirmed JAAA position outstanding at the analysis date, the wind down represents ongoing queue pressure. More broadly, the Resolv case establishes a monitoring requirement: any future JAAA eligibility assessment should map all third-party leveraged JAAA positions on lending protocols before onboarding and update this mapping monthly. The mechanism that generated $100M of queue pressure was protocol insolvency unrelated to CLO quality and could recur with any future leveraged holder.

Conclusions

JAAA is eligible for onboarding as USDe backing. The fund's primary redemption mechanics are operationally sound with no formal capacity limits, a T+1 settlement target, JPMorgan as custodian and execution counterparty, and demonstrated execution quality evidenced by the $318.6M March 2026 block trade at 5 bps slippage with no NAV impairment. The underlying AAA CLO portfolio has a 100% highly liquid classification under MSCI Liquidity Metrics, with full liquidation achievable within three business days. All 20 CLO positions are AAA rated at origination, and as of April 2026, the portfolio weighted average price is $100.12, and no AAA CLO tranche has defaulted or been downgraded in the fund's operating history. Holder concentration in the tokenized wrapper is elevated and is retained as a monitoring input; it does not constitute an eligibility barrier or a binding cap constraint, given that the recommended cap of $250M is below the demonstrated single-day redemption capacity of $318.6M.

Three criteria pass on positive merit independently of concentration: NAV stability (zero below par days; maximum peg deviation of 0.22 bps), primary settlement speed (P90 of 1.98 business days), and carry sustainability (6.3% negative carry day frequency). These confirm that the instrument's underlying structure (AAA CLO tranches, Centrifuge tokenization, Chronicle oracle pricing) is operationally sound. The primary consideration for cap sizing is Ethena's absolute redemption requirement relative to demonstrated execution capacity.

An initial recommended cap of $250M is appropriate given no formal redemption limits and demonstrated single-day execution of $318.6M at 5 bps. At $250M, if Grove exits its $250M Avalanche position post-onboarding, Ethena's share of remaining AUM rises to 61.1%; the $250M absolute exit requirement remains below the $318.6M single day execution precedent, leaving Ethena's redemption capacity unimpaired in this scenario. The cap should scale upward as concentration in the investor base resolves and new investors reduce Ethena's post Grove exit share below the 61.1% level observed at this cap.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network