Insights / Advisory Analysis

Ethena backing asset allocation to Aave V4

This analysis estimates the feasibility of an Aave V4 allocation and argues for an initial Ethena deployment framework.It recommends a conservative initial allocation, subject to Aave V4 draw caps, observed yield performance, exit-liquidity constraints, and Ethena-specific correlated risk.

By Blockworks Advisory ·

Executive summary

Of five Ethena Spoke stablecoins assessed across a 26-day dataset, only USDT at 91% utilization clears the 4.75% minimum allocation return threshold, with protocol-wide supply APY of 0.93%, which is 382 bps below that threshold at current utilization of 37.8%. Aave V4 constitutes a standalone risk assessment because of three structural changes from the prior analysis: (1) a Hub and Spoke architecture that introduces per-Spoke draw caps as the binding external ceiling on deployable capital, (2) a Core Hub credit line that bootstraps stablecoin depth on Plus Hub but creates a wrong-way dependency with Ethena redemption events, and (3) an Ethena Correlated Spoke that can borrow only USDe, requiring independent sizing.

V4 native observed yields run 96-118 bps below model projections at equivalent utilization, raising the effective break-even from 85.5% (model) to approximately 88% for Plus Hub USDC/USDT, approximately 90% for Core Hub USDC/USDT, and above 90% for Plus Hub USDe.

Three independent security audits (Blackthorn, Trail of Bits, ChainSecurity) found no critical or high severity findings. All seven medium severity issues were resolved before mainnet. Three accepted residual risks are relevant to Ethena: (1) a dead share yield lock at low pool TVL (Blackthorn M-2), (2) a deficit reporting delay via dust collateral (Blackthorn L-3, Trail of Bits TOB-AAVE-1), and (3) a riskPremiumThreshold misconfiguration risk on Plus Hub (Trail of Bits TOB-AAVE-3, ChainSecurity CS-AAVE4-022).

The allocation framework from the prior analysis carries forward intact. The 10% total ceiling, looping formula ceiling of $39.8M at $2.15B sUSDe supply and 6x leverage, a minimum 50% Ethena ownership requirement, a 1.25× exit liquidity trigger, and a 25 bps minimum yield premium are all retained. The initial Ecosystem Spoke policy cap is set at $20M, below the looping formula ceiling, pending further analysis as pool depth and utilization history develops. The looping formula governs the steady state policy ceiling, while exit liquidity is a current operational constraint that prevents reaching it, binding at $1.43M under 95% stressed utilization and $2.85M at 90% at the current pool scale of $35.6M. Therefore, active management from day one is recommended.

| Metric | Value |

|---|---|

| Window | March 30 to April 24, 2026 (26 days) |

| Cumulative net supply | $35.6M |

| Cumulative net borrow | $13.5M |

| Protocol-wide utilization | 37.8% |

| Exit liquidity | $22.2M |

| Min allocation yield | 4.75% |

| Supply APY at 37.8% utilization (model) | 0.93% [-382 bps vs threshold] |

| Break-even utilization (model) | 85.5% |

| Break-even utilization V4 calibrated (Plus Hub USDC/USDT) | 88% |

| Break-even utilization V4 calibrated (Core Hub USDC/USDT) | 90% |

| Break-even utilization V4 calibrated (Plus Hub USDe) | 90% |

| Stables clearing threshold today | 1 of 5 (USDT only, at 91% utilization) |

| Weighted avg stable supply APY (gross / net LF) | 3.81% / 3.43% |

| USDC + USDT share of stable borrow flow | 75.0% |

| Ecosystem Spoke policy cap | $20M initial cap; looping formula ceiling $39.8M at $2.15B sUSDe, 6x |

| Correlated Spoke initial cap | $10-15M (USDe only; sized independently) |

| Binding cap 95% stressed util, T1 funded | $1.43M [exit liquidity constraint] |

| Binding cap 90% high util, T1 funded | $2.85M [exit liquidity constraint] |

| USDe supply (April 29, 2026) | $3.80B |

| Liquid backing T1+T2+T3 | $2.62B |

| Tier 1 headroom above 45% floor | $126.8M |

| Audit outcome | 0 critical / 0 high; 7 medium resolved; 3 residual accepted |

Protocol background

Hub and Spoke architecture

Aave V4 deploys a Hub and Spoke architecture. All assets pool into a central Liquidity Hub where Spokes hold user interactions and risk configurations. The same underlying token can carry different collateral factors, liquidation parameters, and collateral risk scores across different Spokes, enabling risk isolation without liquidity fragmentation. Three Hubs are deployed at genesis: (1) Core Hub (general-purpose rate environment and credit line source), (2) Prime Hub (blue-chip collateral, limited borrowable via Bluechip Spoke), and (3) Plus Hub (Ethena strategy domain). Both Ethena Spokes reside on Plus Hub.

Three structural changes from the prior analysis are most consequential. First, the per-Spoke draw cap set by Aave governance is the hard external ceiling on deployment. Second, the Core Hub credit line to the Ecosystem Spoke introduces wrong-way risk, where Core Hub stablecoin stress simultaneously drives Ethena redemption demand and reduces credit line availability. Third, the Correlated Spoke can borrow only USDe, creating a reflexively Ethena native loop that requires independent sizing.

Ethena Spoke reserve configuration

The onchain reserve configuration confirms that the Correlated Spoke (0x5813...649) connects only to Plus Hub with USDe as the sole borrowable asset. The Ecosystem Spoke (0xba1B...8AF) connects to Plus Hub (reserve IDs 0-6) and Core Hub via credit line (reserve IDs 7-9: coreUSDC, corefrxUSD, coreUSDT). RLUSD is not deployed on either Ethena Spoke.

| Spoke | Reserve | Asset | Hub | Role |

|---|---|---|---|---|

| Ethena Correlated | 0-2 | PT-USDe-7MAY26, PT-sUSDe-7MAY26, sUSDe | Plus Hub | Collateral only |

| Ethena Correlated | 3 | USDe | Plus Hub | Collateral + borrowable (USDe loop lane) |

| Ethena Ecosystem | 0-2 | PT-USDe-7MAY26, PT-sUSDe-7MAY26, sUSDe | Plus Hub | Collateral only |

| Ethena Ecosystem | 3 | USDe | Plus Hub | Collateral + borrowable |

| Ethena Ecosystem | 4-5 | USDC, USDT | Plus Hub | Borrowable (direct) |

| Ethena Ecosystem | 6 | GHO | Plus Hub | Borrowable (Plus Hub only) |

| Ethena Ecosystem | 7 | coreUSDC | Core Hub credit line | Borrowable (credit line) |

| Ethena Ecosystem | 8 | corefrxUSD | Core Hub credit line | Borrowable (credit line; no direct Plus Hub pool) |

| Ethena Ecosystem | 9 | coreUSDT | Core Hub credit line | Borrowable (credit line) |

Risk Premium system

V4 introduces collateral quality aware pricing, where each asset receives a Collateral Risk score (CR, 0-10,000 bps), where 0 represents risk-free collateral. The User Risk Premium is the debt-weighted average CR across the position. User borrow rate is R_user = R_base × (1 + RP_u), where R_base is the Hub-level utilization-driven rate. Premium interest accrues via ghost premium shares without affecting the base rate paid by other borrowers. The observed USDT borrow APY of 7.76% versus USDC at 4.47% at near identical utilization (91% vs. 90%) is consistent with the Risk Premium system pricing different collateral compositions per Reserve but the divergence could equally reflect different base IR curve parameters set per asset per Hub by governance. Both sets of parameters remain undisclosed. Isolating the Risk Premium contribution requires confirmed R_base values for each asset from Aave governance.

Circuit breakers

The key distinction for Ethena is between freeze (blocks new supply and borrows; permits withdrawals) and pause (blocks all actions, including exits). The Correlated and Ecosystem Spokes have independent circuit breaker states. A Hub-level action targeting Plus Hub would affect both Ethena Spokes simultaneously. Ethena should monitor governance proposals targeting either Spoke or the Core Hub credit line assets.

Audit and smart contract security

Aave V4 underwent three independent security assessments prior to launching on Ethereum mainnet. Blackthorn (October 2025), Trail of Bits (October to November 2025, 6 engineer weeks, 51 invariant stateful fuzzing), and ChainSecurity (October 2025 to January 2026, five code versions). No critical or high-severity findings were identified. All seven medium severity findings were resolved before launch.

| Auditor | Period | Findings | Status |

|---|---|---|---|

| Blackthorn | Oct 6-20, 2025 | 0 High / 2 Medium / 9 Low | All resolved |

| Trail of Bits | Oct 21 - Nov 3, 2025 (6 eng-weeks) | 2 Medium / 1 Low / 4 Info | 3 resolved; 4 accepted |

| ChainSecurity | Oct 2025 - Jan 28, 2026 (5 versions) | 0 Critical / 0 High / 3 Med / 9 Low | 0 open; 9 corrected; 3 per spec |

The three residual accepted risks most relevant to Ethena are:

- The dead share yield lock (Blackthorn M-2), which locks a portion of early-stage yield at low TVL and further understates model-derived supply APY estimates beyond the 96-118 bps calibration gap;

- the deficit reporting delay via dust collateral (Blackthorn L-3, Trail of Bits TOB-AAVE-1), which can delay formal bad debt recognition after a liquidation cascade; and

- the riskPremiumThreshold misconfiguration (Trail of Bits TOB-AAVE-3, ChainSecurity CS-AAVE4-022), which blocks liquidations if governance lowers the threshold below the effective premium ratio of active sUSDe borrowers.

Yield analysis

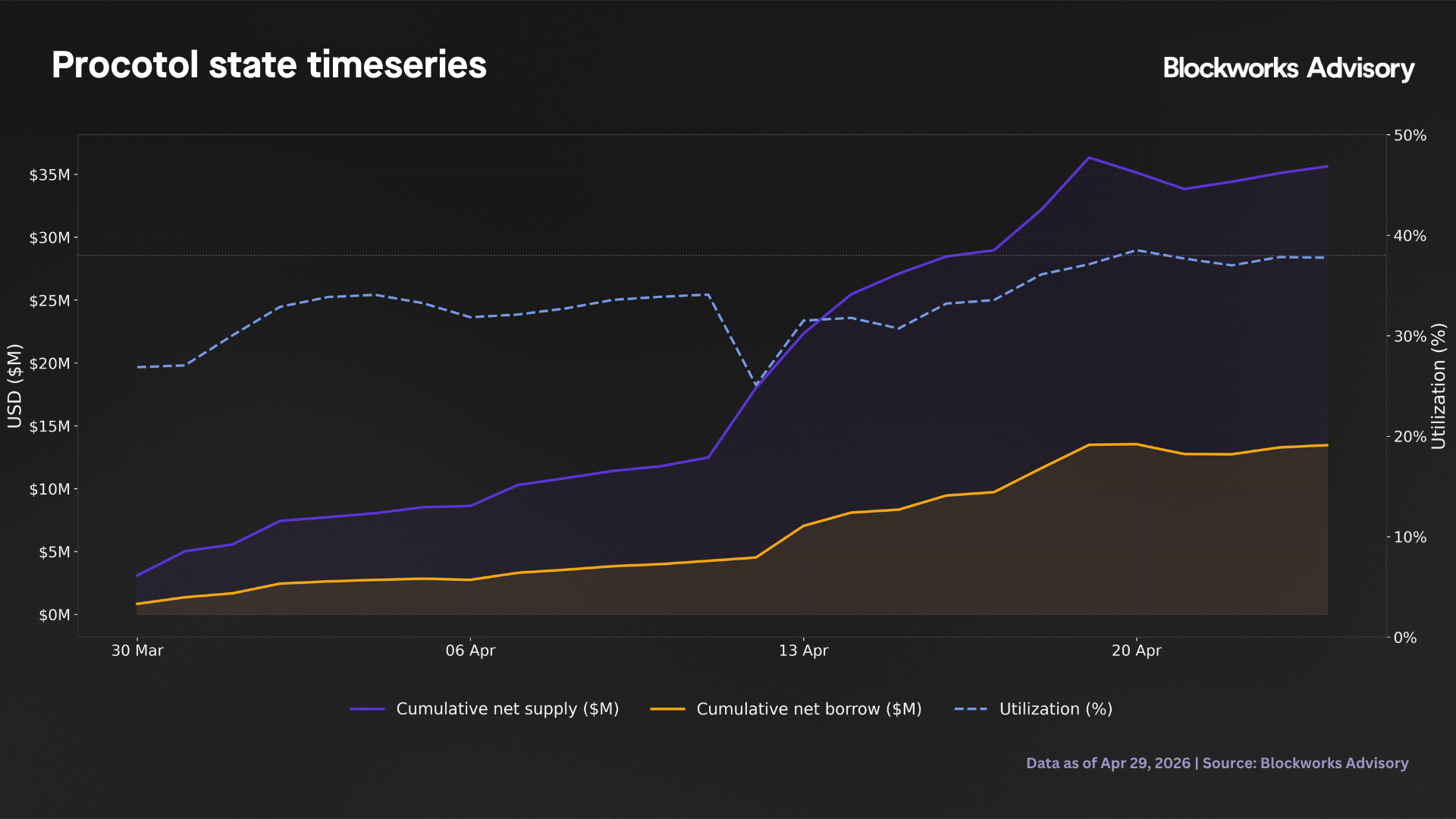

Protocol-level state

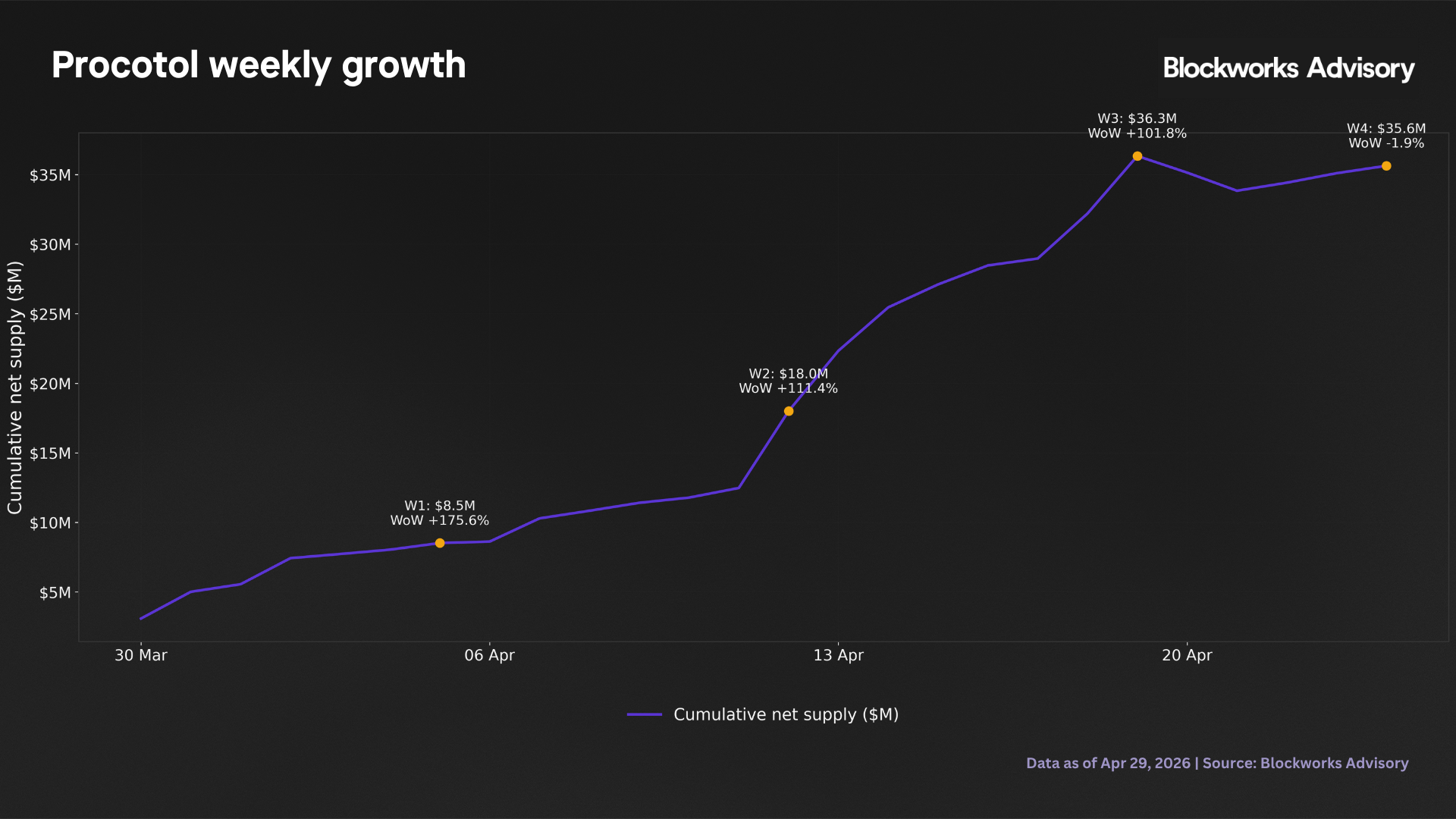

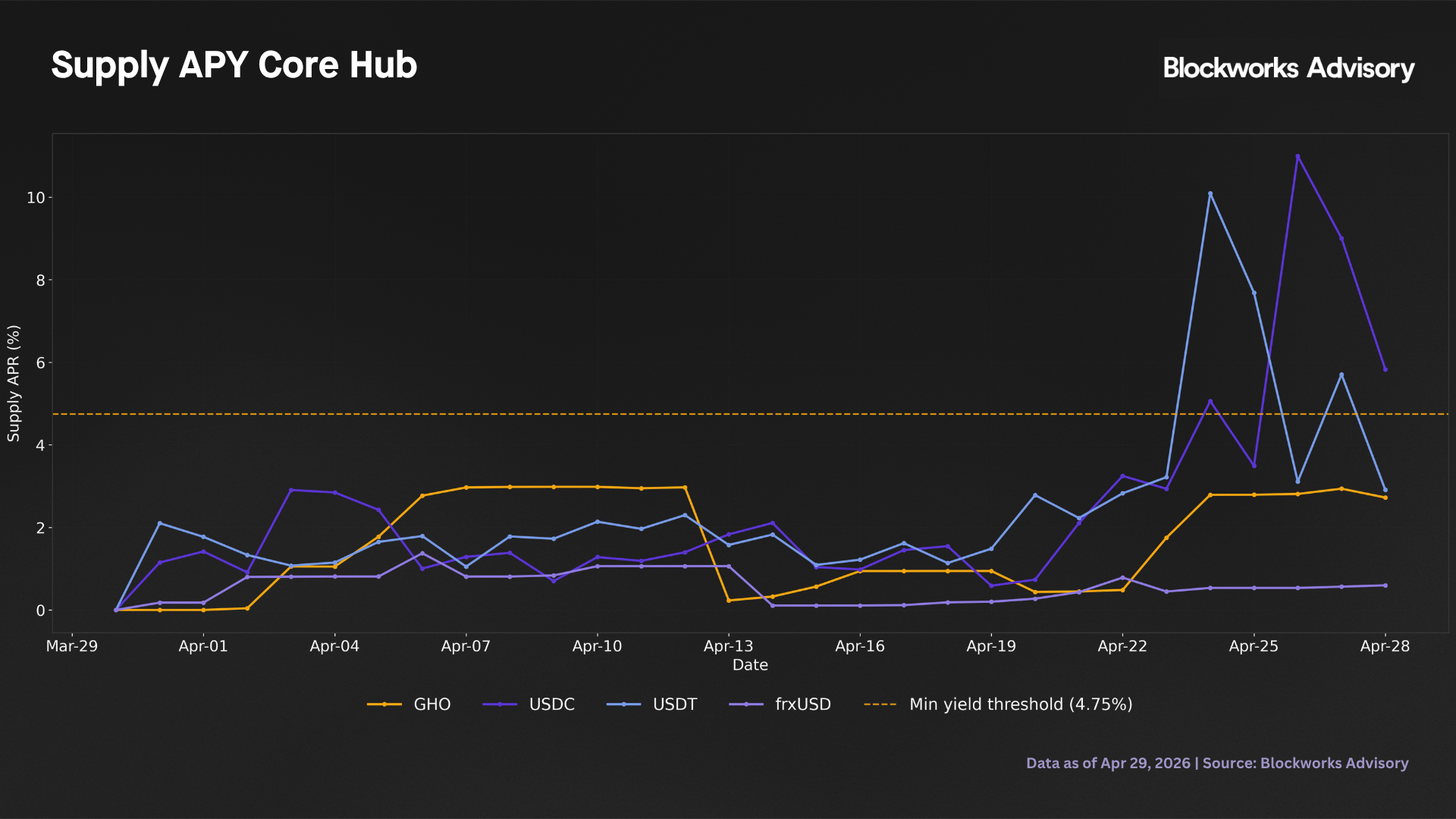

Cumulative net supply reached $35.6M by April 24, 2026, with net borrow at $13.5M, giving a final utilization of 37.8%. The largest single-day flows occurred on April 19 with $10.5M in net supply and $3.75M in net borrow. Daily flow volatility was $1.65M (supply) and $700k (borrow).

The protocol followed a three-week ramp followed by the first reversal. Week 1 closed at $8.5M with 175.6% growth, week 2 grew 111.4% to $18.0M, week 3 grew 101.8% to $36.3M, and week 4 net flows turned negative at -$0.7M, closing at $35.6M. Total window growth from day 1 to day 26 was 1,052.9%. This first reversal warrants monitoring as it may reflect incentive program maturation or a natural ceiling at the current utilization regime.

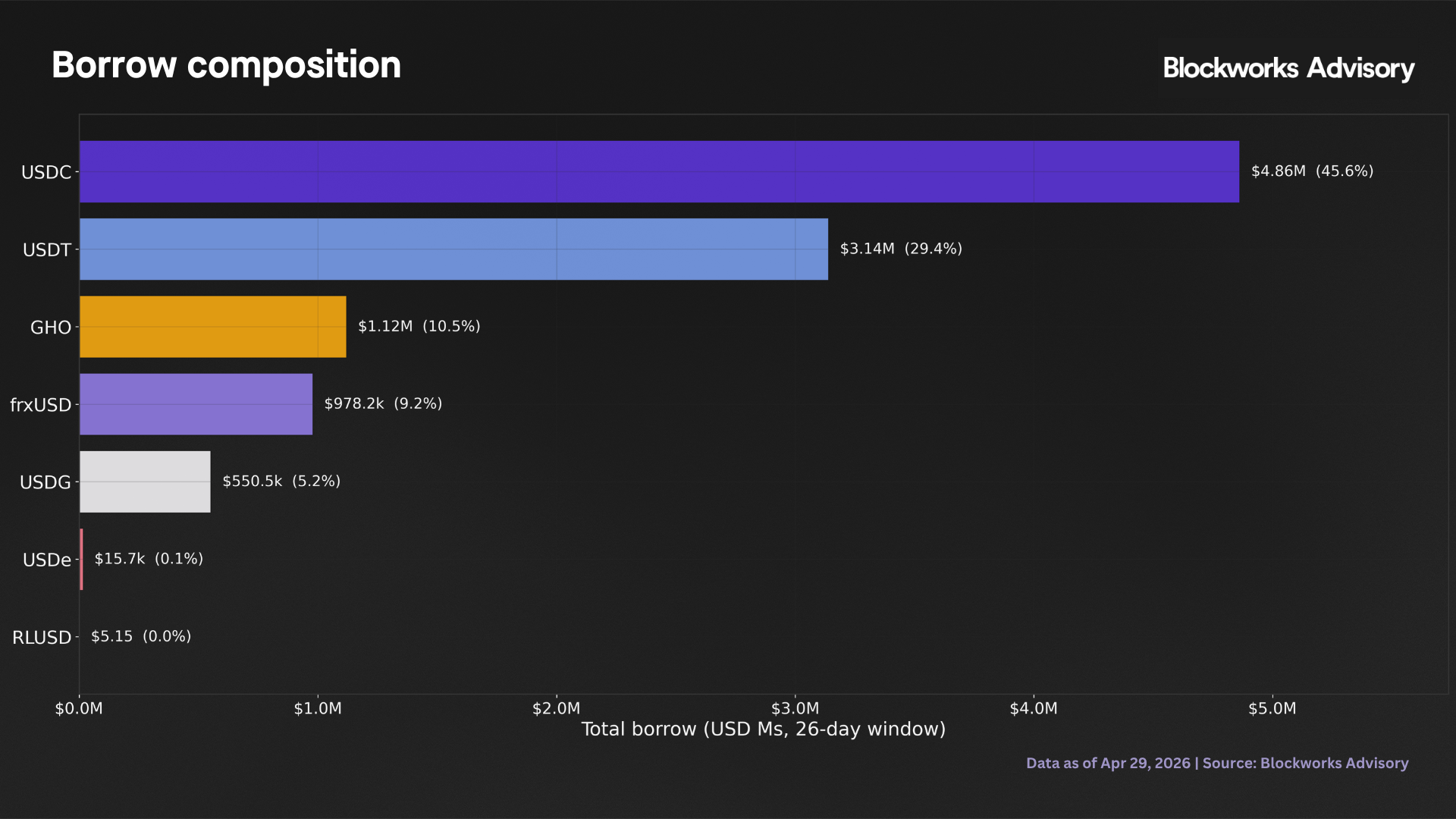

Borrow demand composition

USDC and USDT represent 75% of stable borrow flow. frxUSD, accessible only via the Core Hub credit line, shows intermittent demand and should receive lower allocation priority until the credit line cap and its stress behavior are characterized. GHO is Plus Hub only with no Core credit line counterpart, making borrowable depth directly sensitive to Plus Hub governance actions.

| Asset | Total borrow (26d) | Share | Days active | Spoke routing |

|---|---|---|---|---|

| USDC | $4.86M | 45.6% | 26 | Ecosystem (Plus Hub + Core credit) |

| USDT | $3.14M | 29.4% | 26 | Ecosystem (Plus Hub + Core credit) |

| GHO | $1.12M | 10.5% | 22 | Ecosystem (Plus Hub only) |

| frxUSD | $0.98M | 9.2% | 18 | Ecosystem (Core credit line only) |

| USDG | $0.55M | 5.2% | 23 | Main Spoke, not in Ethena Spokes |

| USDe | $0.016M | 0.1% | 7 | Correlated + Ecosystem Spoke |

| RLUSD | <$0.001M | <0.01% | 2 | Main Spoke, not deployed on Ethena Spokes |

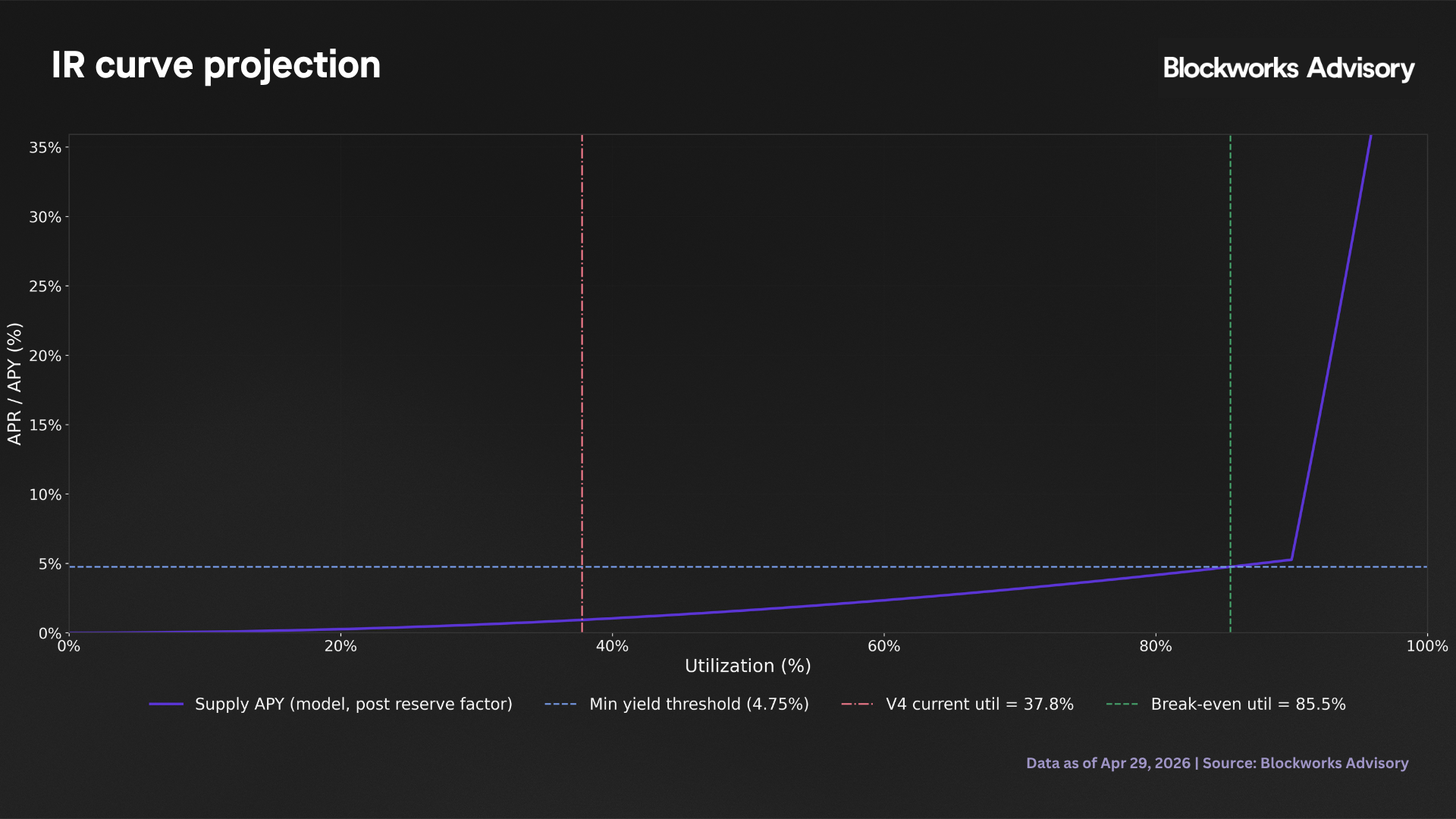

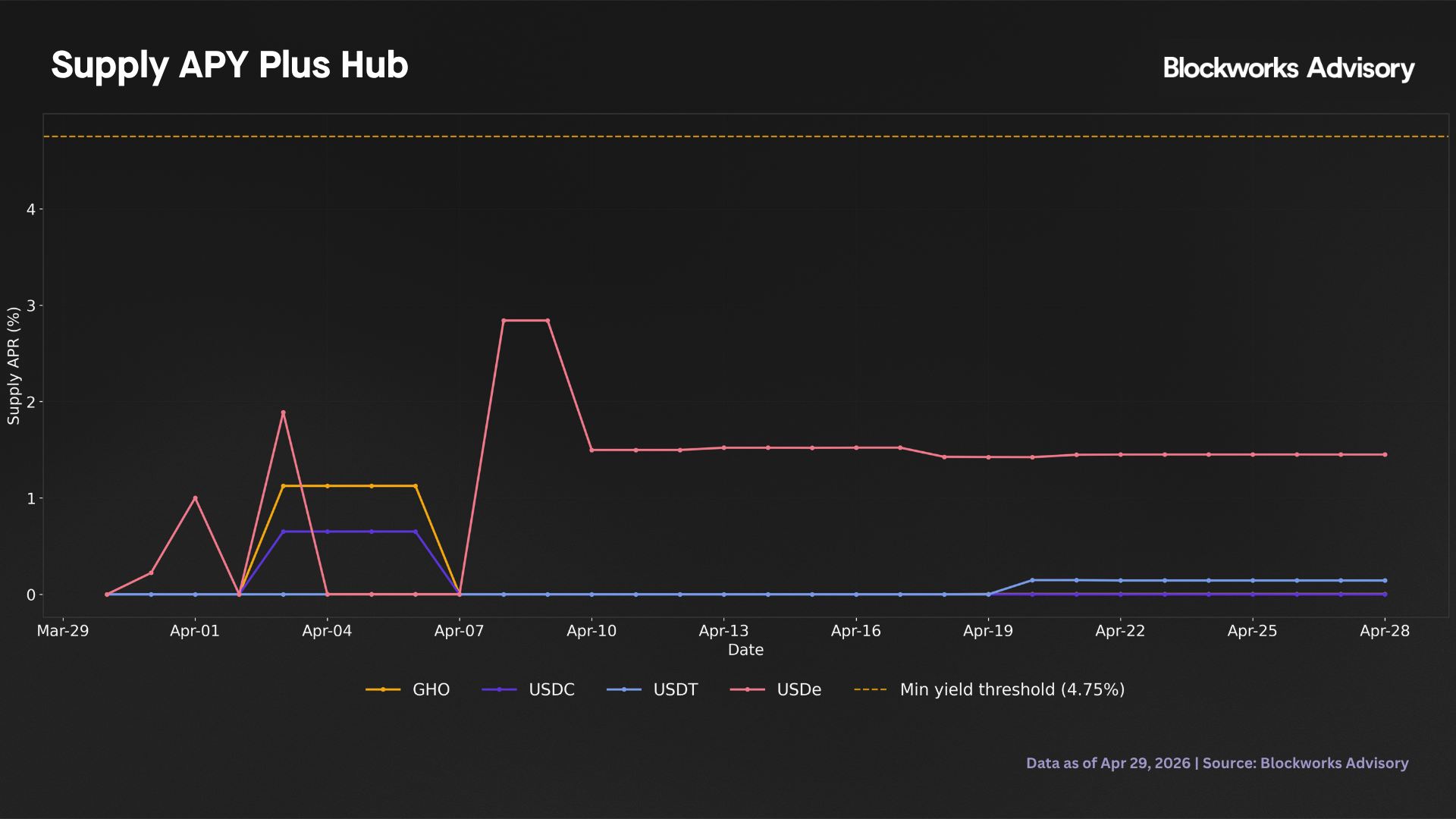

IR curve projection and minimum yield threshold

With the minimum allocation yield threshold being 4.75% (based on previous analysis) and at V4 a current utilization of 37.8%, the model projects 0.93%, showing a gap of 382 bps. The model break-even utilization is 85.5%.

The V4 native calibration is more restrictive. Observed data shows supply APRs running 96 bps to 118 bps below model projections at equivalent utilization: Core Hub USDC observed 1.45% at 60.9% utilization versus model 2.41% (-96 bps), Core Hub USDT observed 1.79% at 67.6% versus model 2.97% (-118 bps), and Plus Hub USDe observed 1.45% at 62.2% versus model 2.52% (-106 bps). Applying this offset, the effective break-even rises to approximately 88% for Plus Hub USDC/USDT (LF=15%), approximately 90% for Core Hub USDC and USDT (LF=10%, -96 bps to -118 bps gap applied), and above 90% for Plus Hub USDe (LF=25%). Model projections are upper bounds in all cases.

Observed per Spoke yields

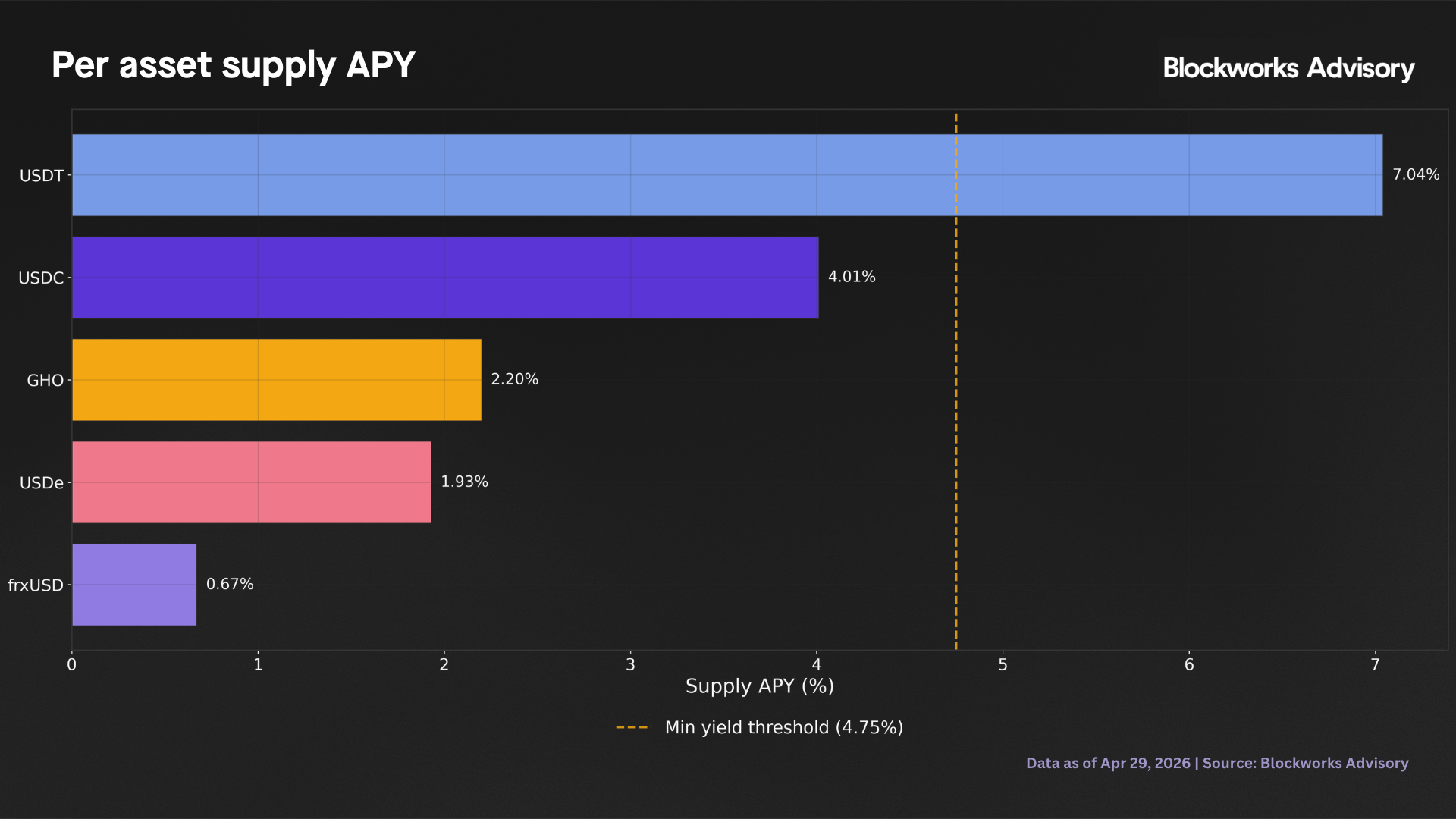

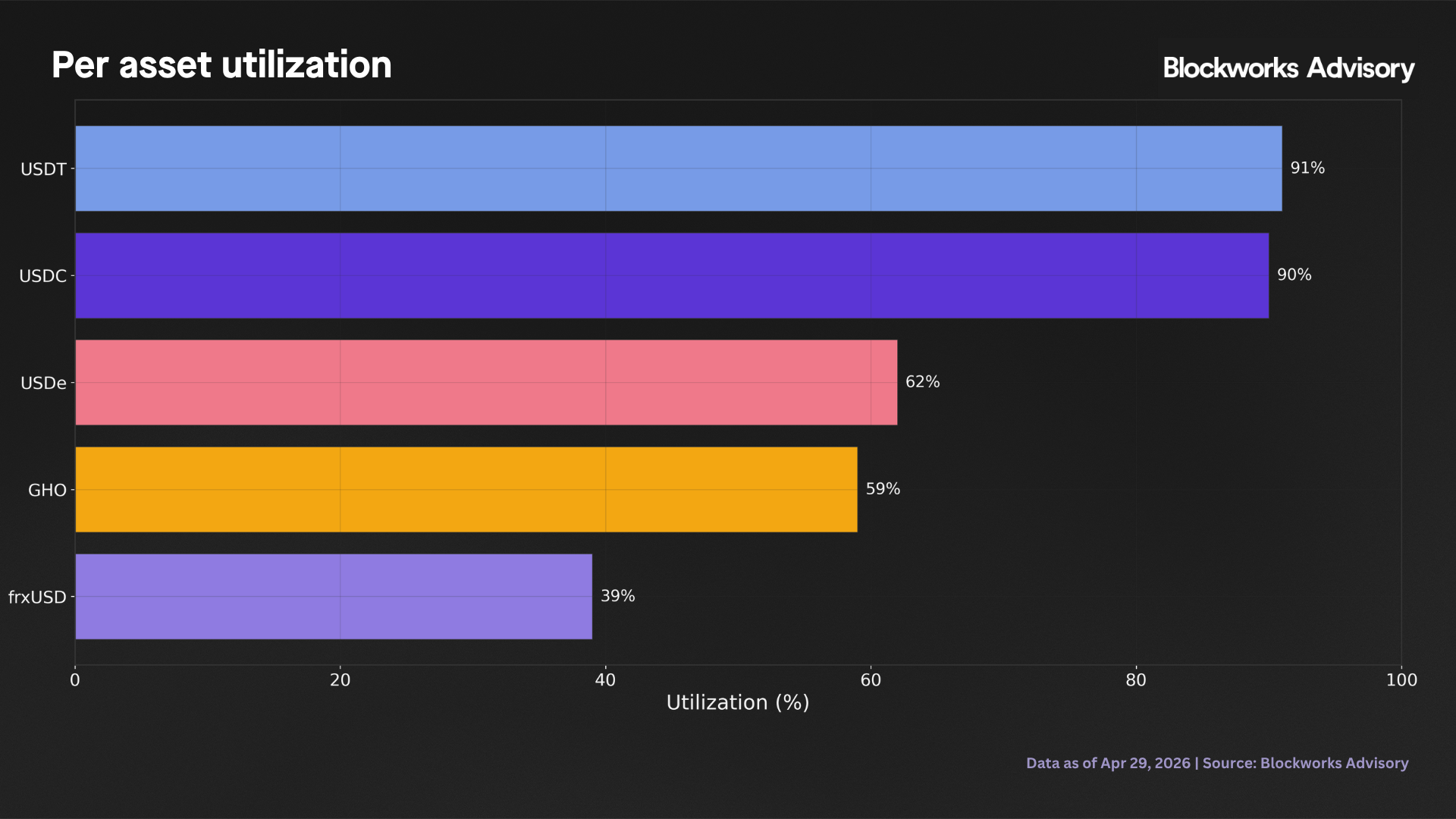

One of five Ethena Spoke stablecoins clears the 4.75% threshold on a net liquidityFee basis. USDC fails by 113 bps despite running at 90% utilization. The divergence between USDC and USDT at nearly identical utilization confirms the Risk Premium system is assigning different CR scores per Reserve. The deposit-weighted average supply APY is 3.81% gross and 3.43% net of liquidityFee at 74.9% weighted utilization. Assets failing the threshold require active entry timing where passive deployment is not justified under current conditions.

| Asset | Utilization | Borrow APY | Supply APY | LF | APY net LF | vs 4.75% |

|---|---|---|---|---|---|---|

| USDT | 91% | 7.76% | 7.04% | 10% | 6.36% | +161 bps |

| USDC | 90% | 4.47% | 4.01% | 10% | 3.62% | −113 bps |

| USDe | 62% | 3.11% | 1.93% | 25% | 1.45% | −330 bps |

| GHO | 59% | 3.72% | 2.20% | 10% | 1.98% | −277 bps |

| frxUSD | 39% | 1.72% | 0.67% | 20% | 0.54% | −421 bps |

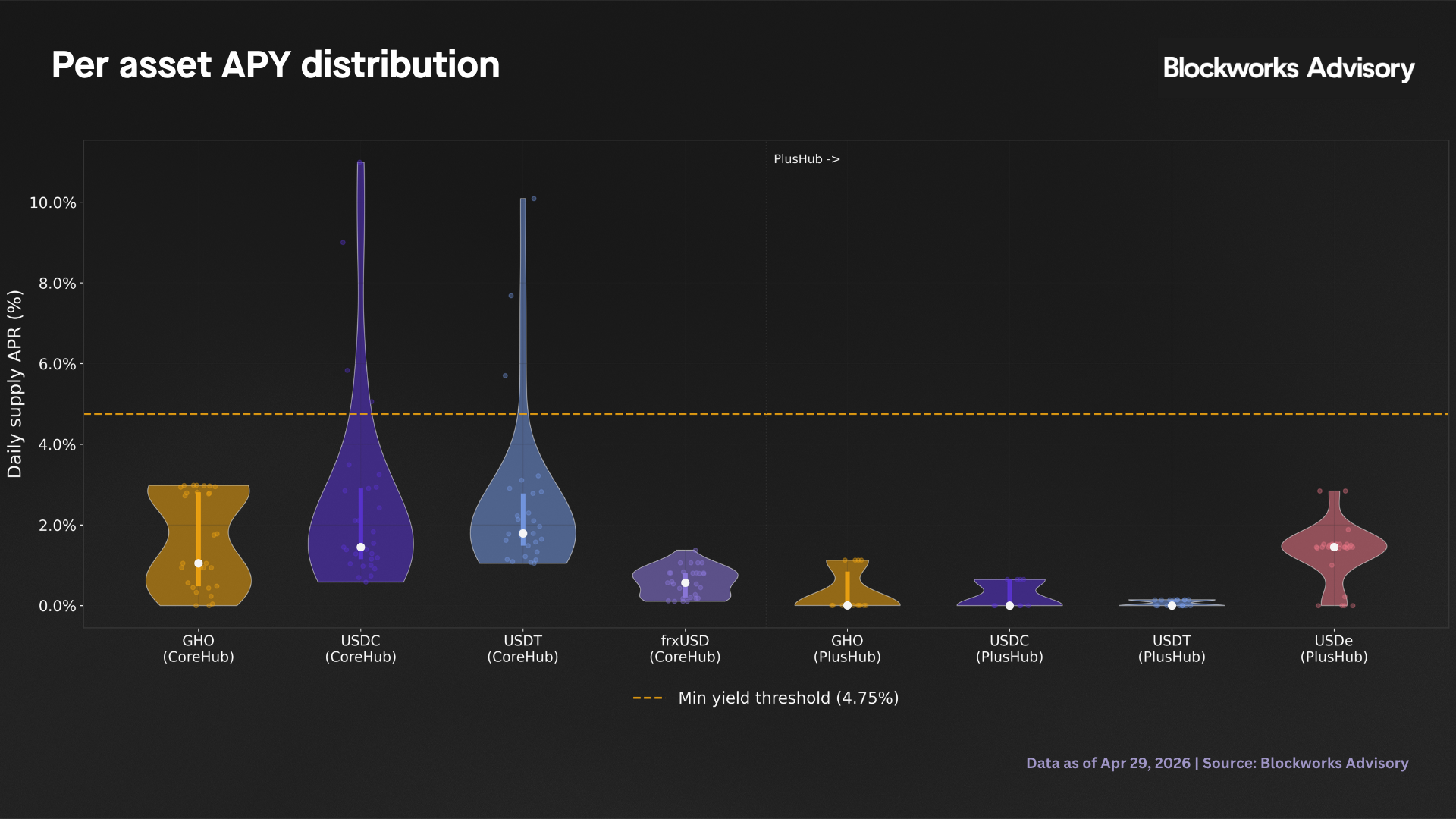

Supply APY distribution

No asset in the Core Hub or Plus Hub consistently sits above the 4.75% threshold at its distribution center. Only USDT reaches the threshold at the upper end of their IQR. The distribution confirms that benchmark clearing yields are accessible only when utilization is simultaneously near peak and sustained, which is a regime requiring active entry timing.

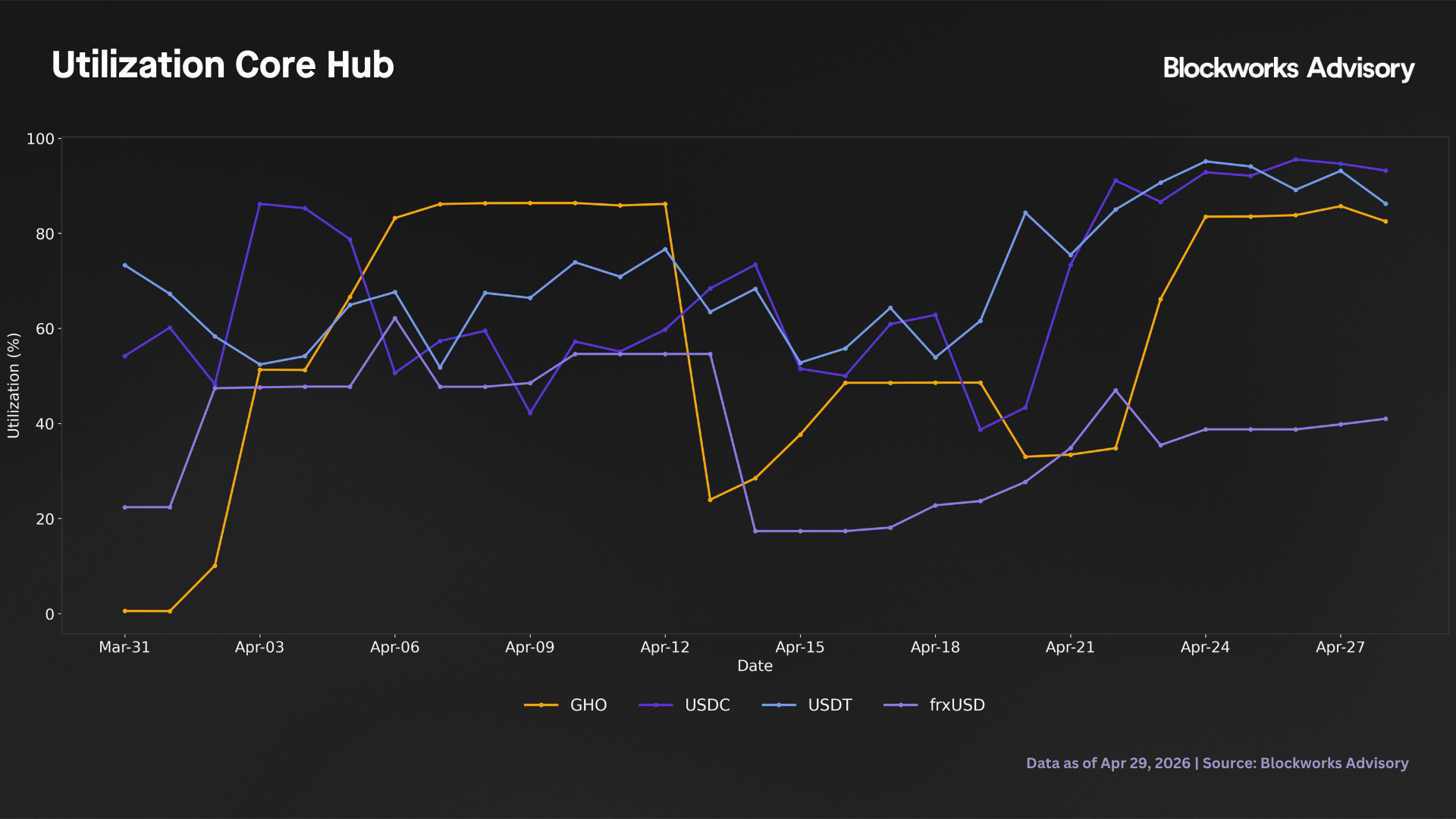

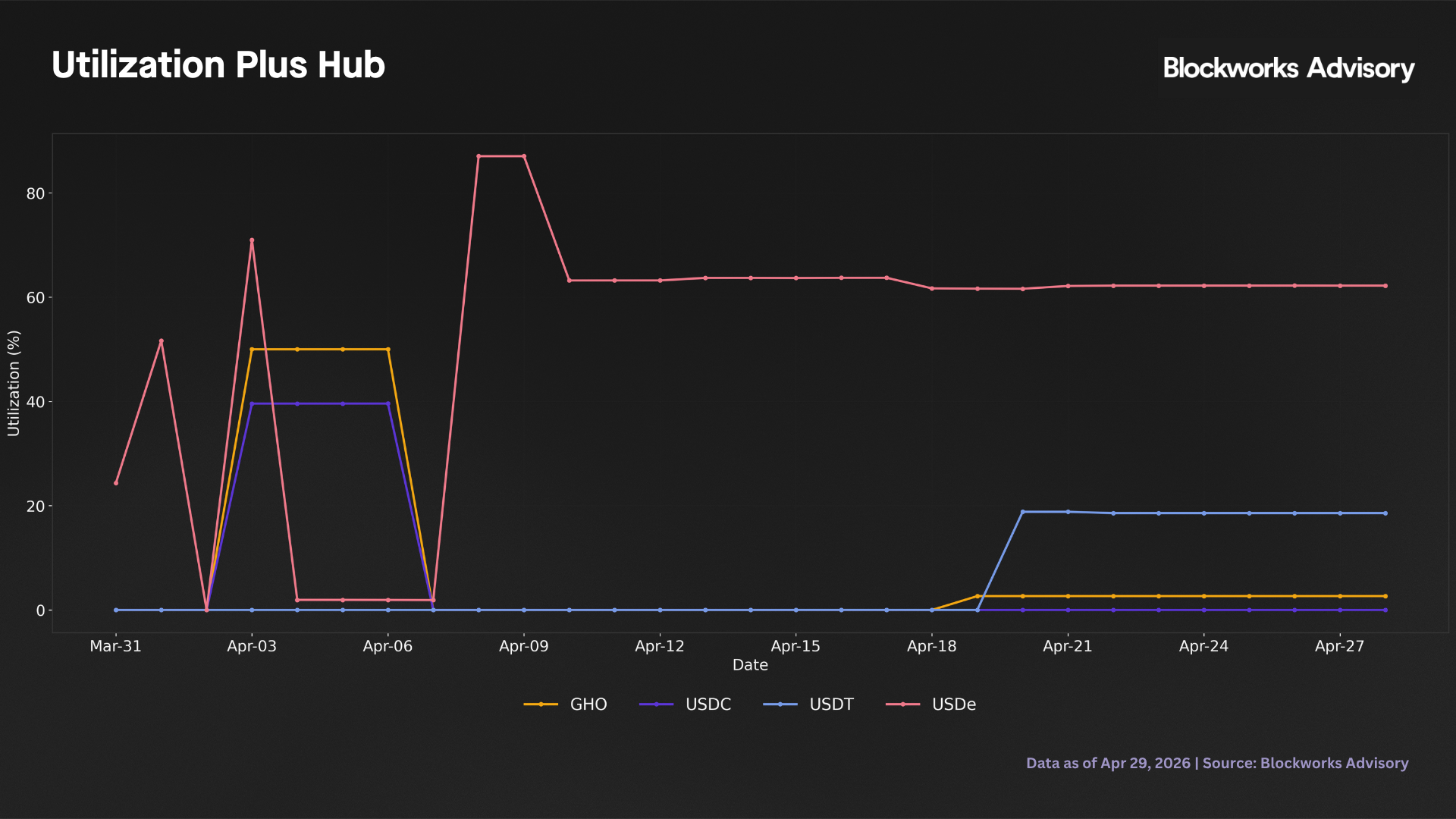

Daily Hub level history

| Hub | Asset | TVL wtd avg util | TVL wtd avg supply APR | liquidityFee | Latest supplied | Latest borrowed |

|---|---|---|---|---|---|---|

| Core Hub | USDC | 67.6% | 2.78% | 10% | $2.48M | $2.31M |

| Core Hub | USDT | 73.1% | 2.73% | 10% | $1.24M | $1.07M |

| Core Hub | frxUSD | 34.1% | 0.47% | 20% | $1.41M | $0.58M |

| Core Hub | GHO | 57.1% | 1.52% | 10% | $0.57M | $0.47M |

| Plus Hub | USDC | 5.5% | 0.09% | 15% | $0.05M | $0.00M |

| Plus Hub | USDT | 5.8% | 0.05% | 15% | $0.05M | $0.01M |

| Plus Hub | USDe | 63.7% | 1.55% | 25% | $0.01M | $0.01M |

| Plus Hub | GHO | 8.7% | 0.17% | 10% | $0.05M | $0.00M |

TVL weighted averages over the 30-day window. liquidityFee observed from onchain data. The flat 10% proxy used in the model understates fees for Plus Hub USDC/USDT (15%) and USDe (25%).

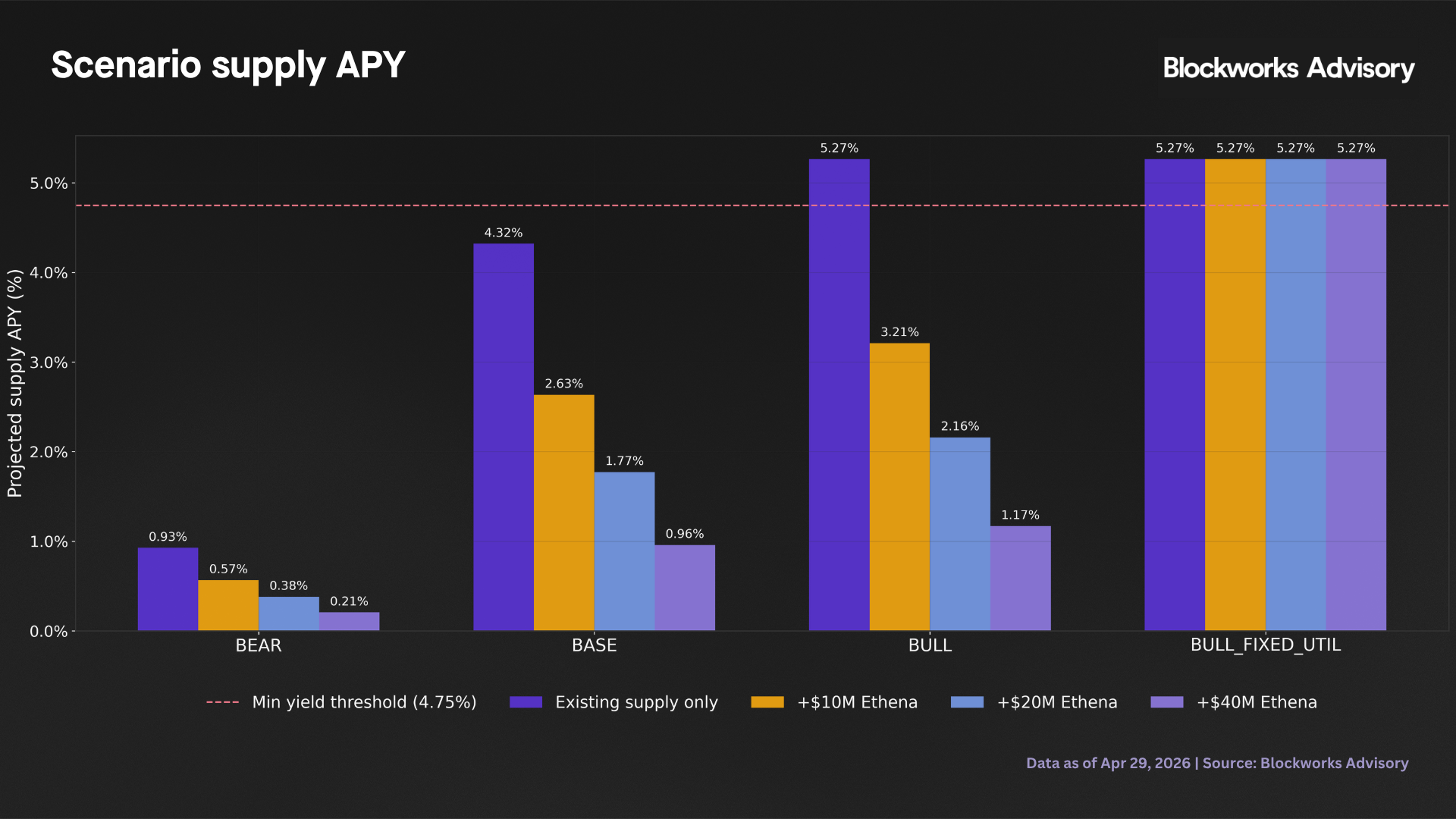

Supply APY scenarios

Projected supply APY by scenario (bear/base/bull) and Ethena supply addition. Bear holds borrow constant, base scales to historical average, and bull scales to 90%, bull_fixed_util holds utilization at 90%.

| Scenario | Borrow assumption | Ethena supply added | Projected util | Projected APY | Clears 4.75%? |

|---|---|---|---|---|---|

| Bear | Held at $13.5M | $0 | 37.8% | 0.93% | No (−382 bps) |

| Bear | Held at $13.5M | +$40M | 17.8% | 0.21% | No (−454 bps) |

| Base | Scaled to 81.5% util | $0 | 81.5% | 4.32% | No (−43 bps) |

| Base | Scaled to 81.5% util | +$10M | 63.7% | 2.63% | No (−212 bps) |

| Bull | Scaled to 90% util | $0 | 90% | 5.26% | Yes (+51 bps) |

| Bull | Scaled to 90% util | +$10M | 70.3% | 3.21% | No (−154 bps) |

| Bull (fixed 90%) | 90% util.; borrow scales with supply | +$40M | 90% | 5.26% | Yes (+51 bps) |

Model projections using V3 proxy parameters with upper bounds on actual V4 yields. V4 calibrated break-even is approximately 88-90% for Plus Hub assets.

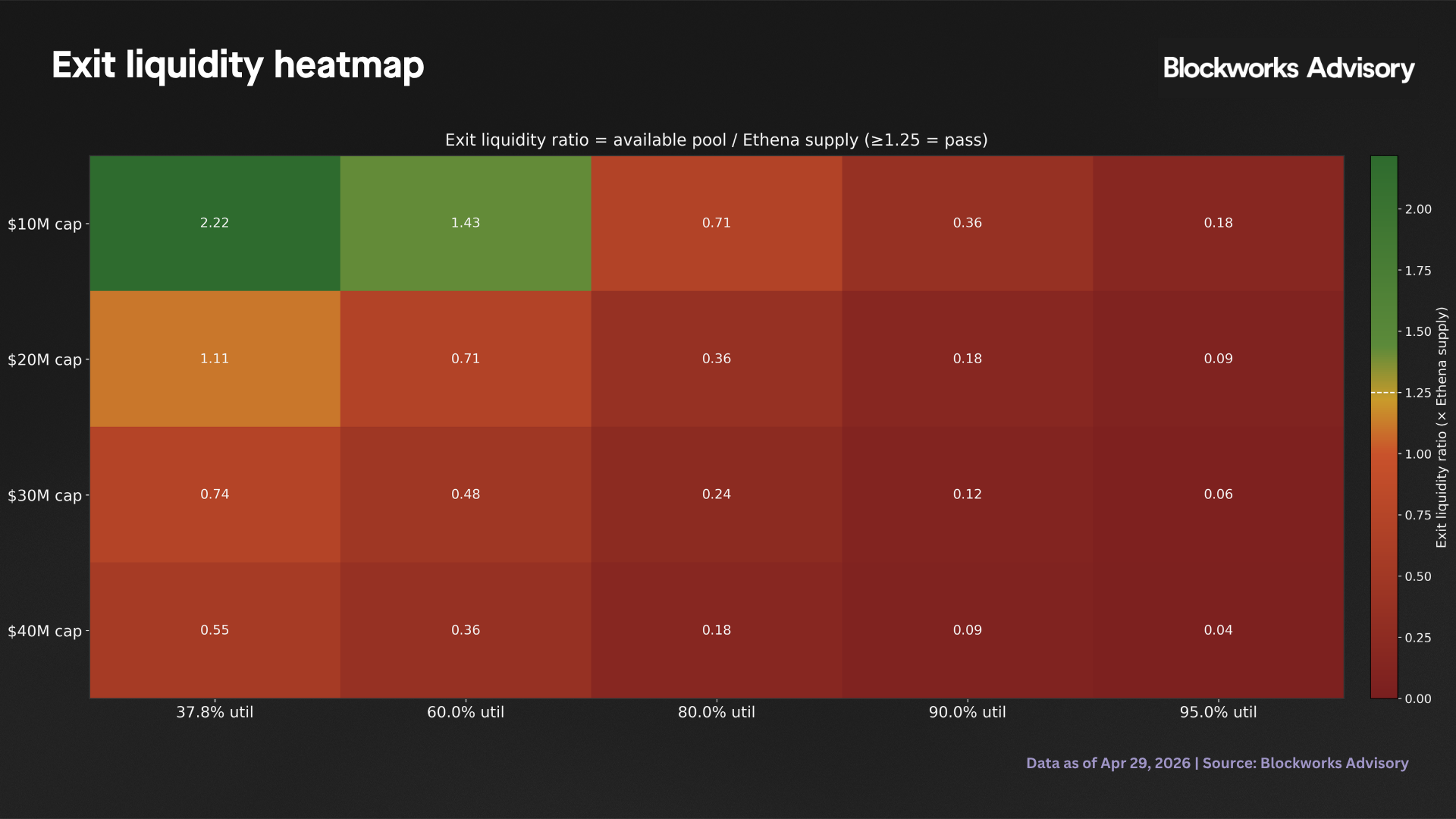

Exit liquidity and redemption risk

Exit liquidity for Ethena in the Ecosystem Spoke has three layers:

- pool-level availability;

- the Plus Hub draw cap; and

- the Core Hub credit line cap (for coreUSDC, corefrxUSD, coreUSDT).

The Correlated Spoke has only pool-level availability and the Plus Hub draw cap. Under stress, all three layers tend to bind simultaneously. The Core Hub credit line is a normal conditions bootstrapping mechanism and does not function as a stress safety valve.

The wrong way risk is structural, where a USDC or USDT depeg event simultaneously increases Ethena redemption pressure and reduces Core Hub credit line availability. frxUSD routes exclusively via the Core Hub credit line, making a frxUSD stress and a Core Hub liquidity contraction correlated.

| Ethena supply cap | Protocol utilization | Available pool liquidity | Exit ratio | ≥ 1.25× |

|---|---|---|---|---|

| $10M | 37.8% (current) | $22.2M | 2.22× | Yes |

| $10M | 60% | $14.3M | 1.43× | Yes |

| $10M | 80% | $7.1M | 0.71× | No |

| $10M | 95% | $1.8M | 0.18× | No |

| $20M | 37.8% (current) | $22.2M | 1.11× | No |

| $40M | 37.8% (current) | $22.2M | 0.55× | No |

Exit liquidity scenarios at the current pool size ($35.6M). Binding exit liquidity cap: at 95% stressed util. = $35.6M × 0.05 / 1.25 = $1.43M and at 90% util. = $35.6M × 0.10 / 1.25 = $2.85M.

At the current pool size, the 1.25× threshold holds only for caps up to approximately $17.7M at current utilization. The $20M initial policy cap exceeds this threshold and passes only once the pool TVL reaches approximately $40M at current utilization (37.8%). Active management is required throughout the bootstrapping phase; deployment must remain within C2 regardless of the policy cap level

Looping risk

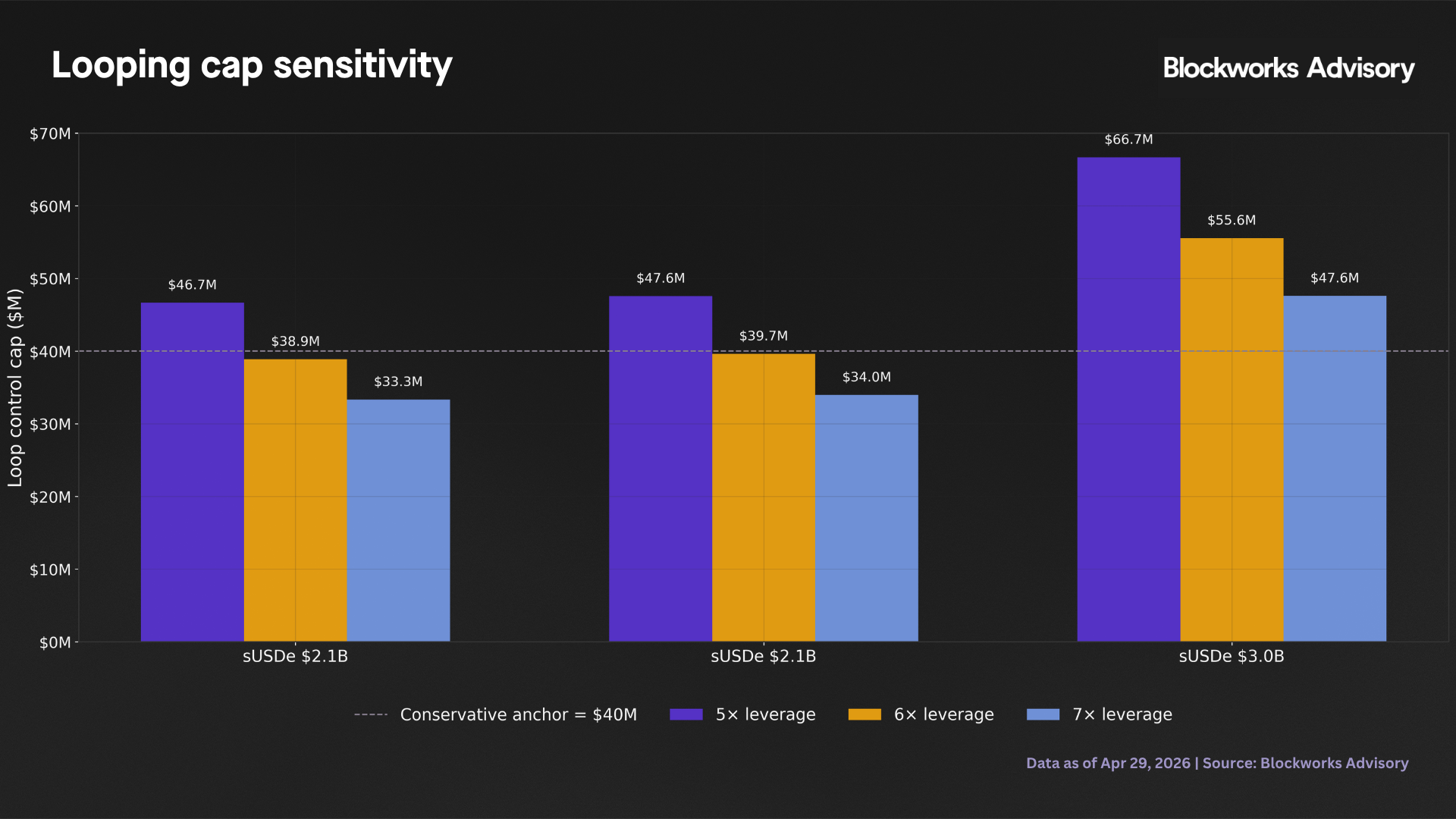

Ethena Ecosystem Spoke

The Ecosystem Spoke is designed for sUSDe collateralized borrowing of Ethena ecosystem stablecoins. The loop chain is to deposit sUSDe as collateral, borrow stable, sell into USDe, restake as sUSDe, and repeat. The borrower population approaches 100% of the Ethena ecosystem by Spoke design. The loop formula max_supply = (10%/90%) × sUSDe_supply / max_leverage is the primary policy cap for the Ecosystem Spoke allocation. The looping formula output of $39.8M at $2.15B sUSDe and 6x leverage represents the analytical steady state ceiling. The initial policy cap is set at $20M, below the formula ceiling, pending further analysis as pool depth and utilization history develop.

Loop control cap and Ethena 50% ownership floor by sUSDe supply scenario and leverage assumption.

| sUSDe supply | Max leverage | Loop control cap | Ethena 50% floor | Conservative cap |

|---|---|---|---|---|

| $2.15B (working assumption) | 5× | $47.8M | $23.9M | $40M |

| $2.15B | 6× | $39.8M | $19.9M | $39.8M (anchor $40M) |

| $2.15B | 7× | $34.1M | $17.1M | $34.1M |

| $3.0B (proxy) | 6× | $55.6M | $27.8M | $40M (draw cap binding) |

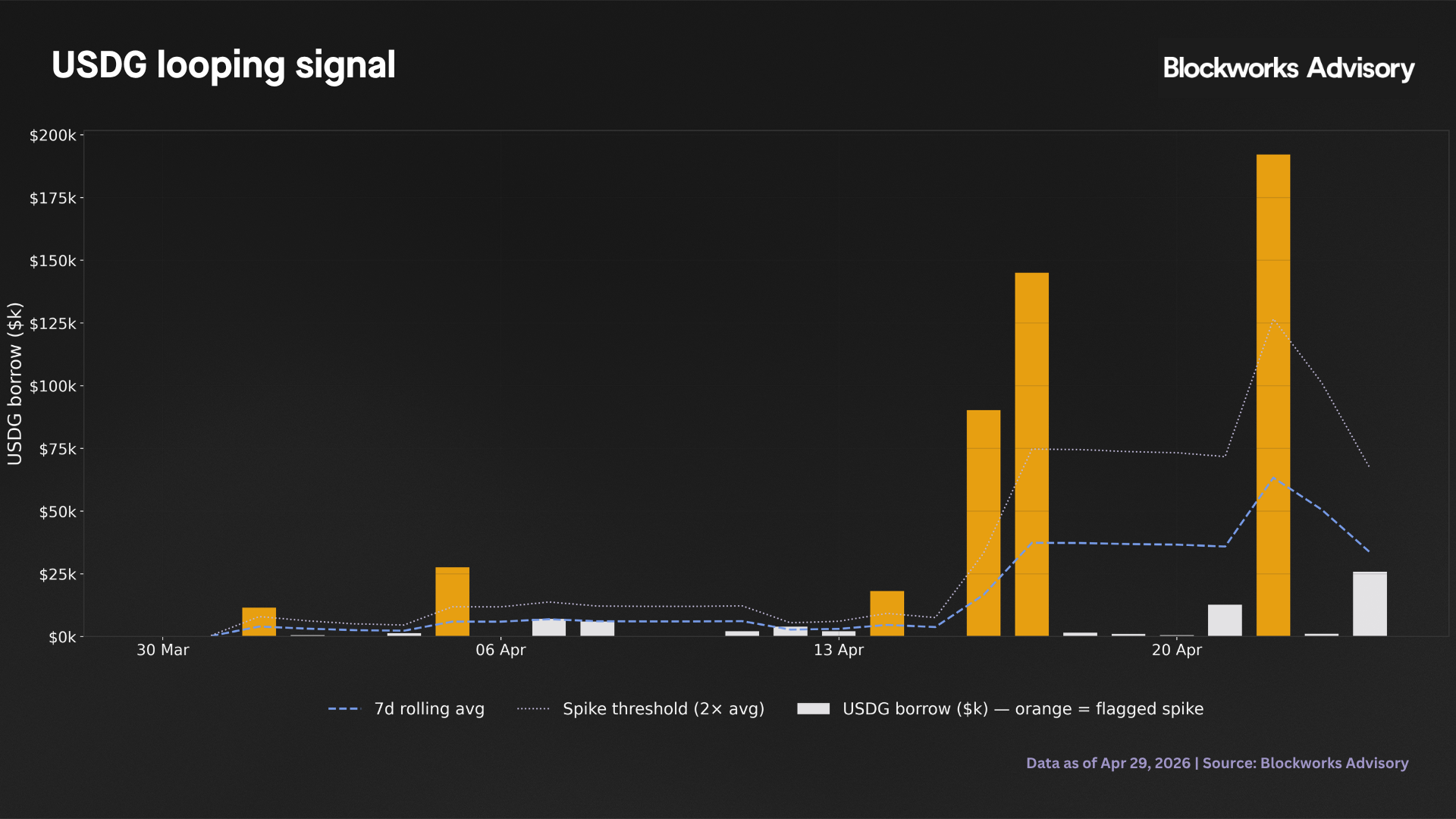

USDG looping signal

USDG borrow demand exhibits six spike days when daily borrows exceeded twice the rolling seven-day average. Spike day average transaction size of $40.0k versus normal day average of $1.5k (27× concentration differential) is consistent with early looping tests. Cumulative USDG borrow across the window is $550.5k, operationally immaterial at the current scale. The pattern is flagged as a behavioral leading indicator for how loop dynamics could develop as TVL grows.

Ethena Correlated Spoke

The Correlated Spoke can borrow only USDe. The loop is to deposit sUSDe, borrow USDe, restake as sUSDe, and repeat. This circuit does not involve external stablecoins, eliminating cross-stablecoin wrong-way risk. However, the feedback is entirely Ethena native, where sUSDe yield compression and loop unwind are both Ethena internal events. Where USDe is used as collateral, a second loop path exists, which is deposit USDe, borrow USDe, redeposit, repeat, without requiring a staking step. The sUSDe restake path carries additional friction via a cooldown queue unless executed via the secondary market at the prevailing basis. USDe was borrowed on only seven of 26 days (maximum single-day draw $15.2k), confirming minimal activity at genesis. The initial cap of $10-15M reflects the contained but reflexive nature of the loop. PT token maturity on May 7, 2026, may affect Correlated Spoke activity.

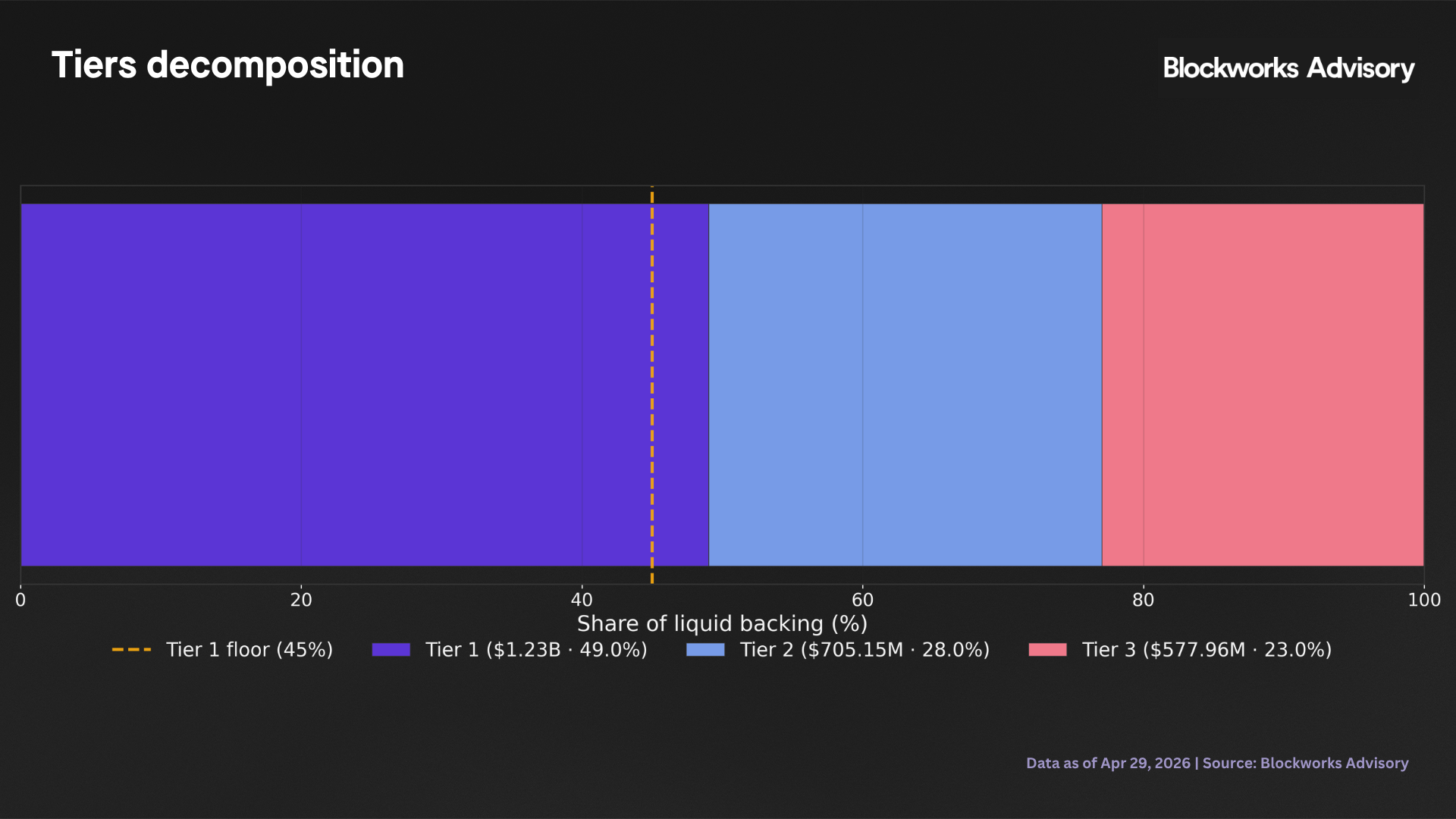

Cooldown framework integration

The cooldown framework decomposes USDe backing into three tiers:

- Tier 1 — one-day cash;

- Tier 2 — two-day yield-bearing and withdrawable lending; and

- Tier 3 — five-day rest of loans.

Policy requires Tier 1 ≥ 45% of total liquid backing. Allocating Ethena stables to Aave V4 lending reroutes liquidity from Tier 1 into Tier 3, consuming Tier 1 headroom. The maximum Aave allocation is therefore also bounded by Tier 1 headroom above the 45% floor.

Tier 1/2/3 composition as a share of liquid backing, as of April 29, 2026. Dashed line: 45% Tier 1 floor.

| Metric | Value |

|---|---|

| USDe supply | $3.80B |

| Tier 1 | $1.30B (49.8%) |

| Tier 2 | $688.9M (26.3%) |

| Tier 3 | $623.8M (23.8%) |

| Total liquid backing (T1+T2+T3) | $2.62B |

| Tier 1 floor (45% × liquid backing) | $1.18B |

| Tier 1 headroom | $126.8M |

| Max Aave alloc T1 funded (conservative) | $126.8M |

| Max Aave alloc. 50/50 T1+T2 blend | $253.5M |

The Tier 1 floor cap is a hard policy boundary. At the current headroom of $126.8M, the floor is not the binding constraint since the exit liquidity cap ($1.43M at 95% stress) binds earlier. However, Tier 1 headroom is dynamic, where growing sUSDe supply and increased Tier 3 loan activity can compress headroom, at which point the floor becomes the operative ceiling.

Binding allocation cap framework

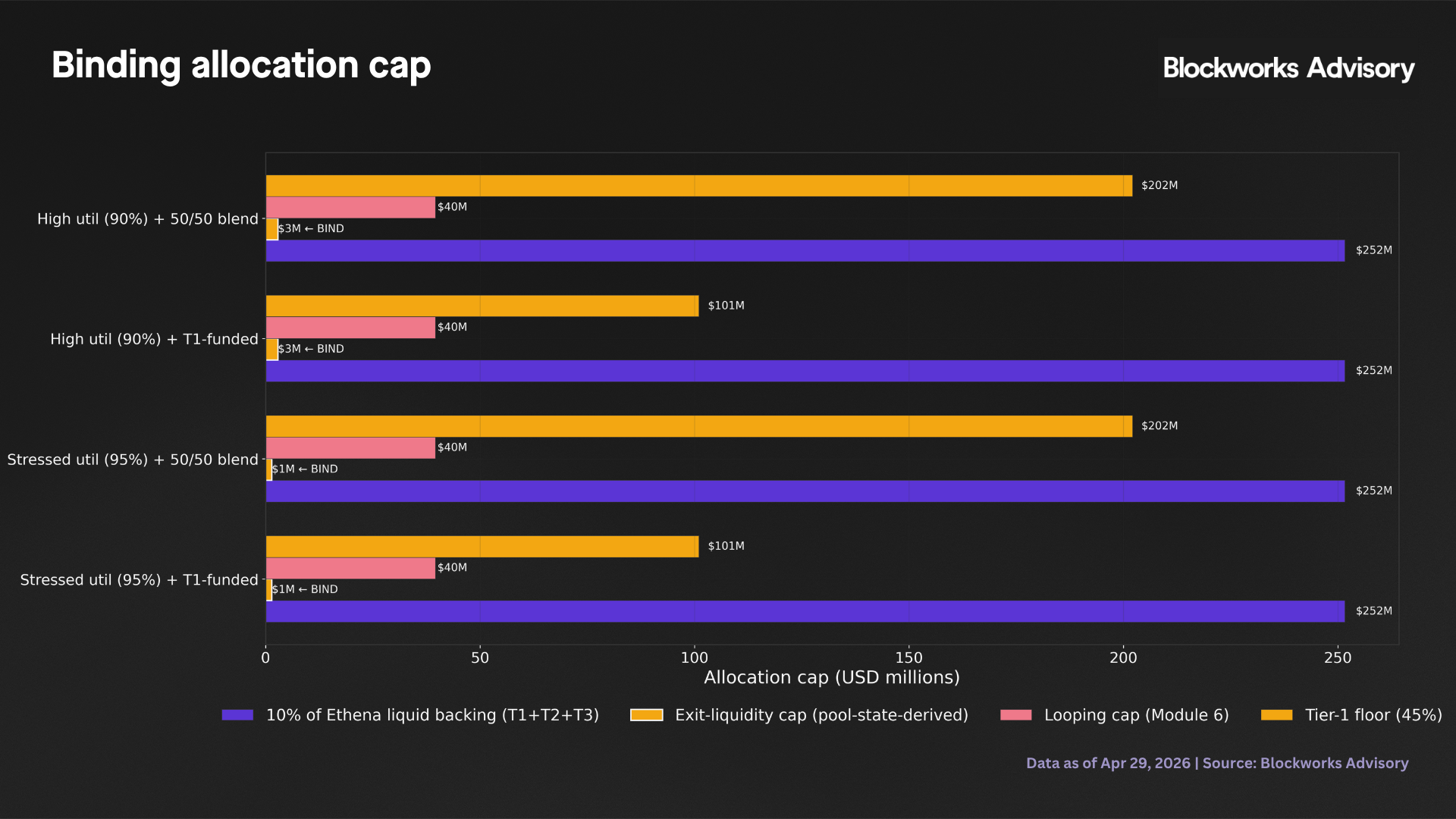

The looping formula (C3) defines the policy cap for the Ecosystem Spoke with $39.8M at $2.15B sUSDe supply and 6x leverage. Three additional independent constraints bound the allocation, with C1 representing 10% of liquid backing ($261.7M), C2 representing the exit liquidity cap (available pool liquidity at stressed utilization / 1.25), and C4 representing the Tier 1 floor cap ($126.8M). At the current liquidity pool scale of $35.6M, C2 is the operative daily constraint. C3 becomes the binding policy constraint when Plus Hub pool TVL exceeds approximately $498M at 90% utilization.

All four cap values by scenario with binding constraint highlighted. The exit liquidity cap is the binding constraint in all current scenarios.

| Scenario | C1 (10% backing) | C2 (exit liquidity) | C3 (loop) | C4 (T1 floor) | Binding | Max alloc |

|---|---|---|---|---|---|---|

| Stressed (95%), T1 funded | $261.7M | $1.43M | $39.8M | $126.8M | C2 | $1.43M |

| Stressed (95%), 50/50 | $261.7M | $1.43M | $39.8M | $253.5M | C2 | $1.43M |

| High (90%), T1 funded | $261.7M | $2.85M | $39.8M | $126.8M | C2 | $2.85M |

| High (90%), 50/50 | $261.7M | $2.85M | $39.8M | $253.5M | C2 | $2.85M |

| Steady state (90%), TVL > $498M | $261.7M+ | $20M+ | $20M | $126.8M | C3 | $20M |

C2 = $35.6M × (1 − util) / 1.25. C3 uses $2.15B sUSDe supply at 6× leverage. C1 and C4 are non-binding at the current TVL. The policy allocation target is C3=$39.8M; the current accessible maximum is C2.

The initial policy cap is $20M for the Ecosystem Spoke; further analysis will inform scaling towards the looping formula ceiling of $29.8M as pool depth and utilization history develop. Day one sizing should remain within the exit liquidity constraint (C2) where $20M exceeds the 1.25x exit threshold at the current pool size of $35.6M and becomes accessible once the pool TVL reaches approximately $40M at current utilization or $250M at 90% utilization, at which point C3 becomes the operative constraint.

Risk considerations

Exit liquidity concentration. The benchmark clearing utilization regime (≥88-90% for Plus Hub assets) coincides with stressed exit liquidity. At 90% utilization and any Ethena supply cap above $2.85M, the 1.25× exit threshold fails. The inverse relationship between yield and exit liquidity is structural and requires active position management.

Core Hub credit line wrong-way risk. A USDC or USDT depeg event simultaneously increases USDe redemption pressure and reduces Core Hub credit line availability. A comparable dynamic exists in the V3 shared liquidity pool, where stablecoin stress similarly compresses exit liquidity for all borrowers concurrently. V4 credit line (governance capped) bounds Ethena's worst-case exposure more tightly than V3 pool exposure, but it introduces a separate risk. The cap itself can be reduced by governance during stress, which is absent in V3 continuous utilization-driven mode. The dynamic indicates that loopers unwinding leveraged sUSDe positions must repay borrowed USDC or USDT before withdrawing collateral and that repayment returns liquidity to the Core Hub reserve. It depends on loopers repaying promptly, and it does not address withdrawal demand from non Ethena Core Hub depositors drawing on the same reserve. Frax’s frxUSD is additionally exposed since it routes exclusively via the Core Hub credit line, making a frxUSD stress and a Core Hub liquidity contraction structurally correlated.

riskPremiumThreshold governance risk. If Aave governance reduces the riskPremiumThreshold on Plus Hub below the current effective premium ratio of active sUSDe borrowers, new borrows and liquidations are blocked until the ratio falls below the threshold. A misconfiguration during a period of sUSDe yield stress blocks the liquidation mechanism that would otherwise cap losses on undercollateralized positions. Bad debt risk against Ethena-supplied capital is conditional as it materializes only if collateral values continue to deteriorate while the misconfiguration remains active. A misconfiguration identified and corrected quickly, or one occurring while collateral prices are stable, would not by itself generate bad debt.

Dead share yield lock during bootstrapping. Aave V4 seeds a small fixed quantity of virtual dead shares at each Reserve genesis to prevent first depositor share price manipulation. These dead shares accrue yield like any other share, but that yield is permanently unclaimable and acts as a fixed-size absolute deduction from the yield pool. Because the dead share notional is fixed in absolute terms, the locked fraction of yield is largest when Reserve TVL is small and decreases as TVL increases. At current Reserve TVL levels across Ethena Spokes, this effect is most pronounced and further understates model-derived supply APY estimates beyond the 96-118 bps calibration gap already confirmed from observed data. This effect is expected to become immaterial as Reserve TVL scales.

Preliminary allocation framework

| Parameter | Recommendation | Rationale |

|---|---|---|

| Total Aave V4 ceiling | ≤10% of liquid backing ($261.7M) | Protocol-level concentration limit; unchanged from prior analysis |

| Plus Hub draw cap | Confirm from Aave governance before deployment, supersedes all internal calculations | New hard external ceiling in V4; no internal calculation can substitute |

| Core Hub credit line caps | Track coreUSDC, corefrxUSD, coreUSDT caps separately from Plus Hub draw cap | Total Ecosystem Spoke depth = Plus Hub supply + Core credit; both layers monitored |

| Ecosystem Spoke policy cap | $20M initial cap; $39.8M (looping formula ceiling at $2.15B sUSDe, 6×); actual binding = min(looping formula, draw cap, credit line cap) | Initial cap set below formula ceiling; scale up subject to further analysis as pool depth and utilization history develop. Draw cap and credit line caps are external ceilings that may bind below $20M |

| Correlated Spoke initial cap | $10-15M; USDe only; sized independently | Reflexively Ethena native loop; absent empirical track record; separate monitoring |

| Ethena ownership | ≥50% of Ecosystem Spoke supply | Near 100% Ethena borrower population; predominant ownership is the control mechanism |

| Minimum yield threshold | 4.75%; use per Reserve liquidityFee in APY calculation | Carries forward from prior analysis; liquidityFee required in V4 APY computation |

| Exit liquidity trigger | 1.25× at Reserve level; monitor pool availability, Plus Hub draw cap, and Core credit line cap | Three-layer exit structure; all three bind simultaneously under stress |

| Management posture | Active from day one; enter only when supply APY > 4.75% and exit liquidity ≥ 1.25× | Protocol-wide utilization 37.8% at launch; passive supply does not clear threshold |

Conclusion

Aave V4 introduces three structural changes that require standalone analysis.

- The per-Spoke draw cap as a new external ceiling.

- The Core Hub credit line whose governance set cap bounds exposure more tightly than V3 shared pool, introduces a discrete cap reduction scenario which partly offset by repayment-driven liquidity recovery during loop unwind.

- The Correlated Spoke’s reflexively Ethena native USDe loop.

Three independent audits found no critical or high-severity issues, and all medium-severity findings were resolved before mainnet launch. The analytical framework, including a looping formula as the primary policy cap, a 10% ceiling, a 1.25× exit trigger, and a 25 bps minimum yield premium, carries forward intact.

At protocol-wide utilization of 37.8%, a passive supply APY of 0.93% is 382 bps below the 4.75% threshold. V4 native observed yields run 96-118 bps below model projections at equivalent utilization, raising the effective break-even to approximately 88% for Plus Hub USDC/USDT, approximately 90% for Core Hub USDC/USDT, and above 90% for Plus Hub USDe. At the current pool scale ($35.6M), the exit liquidity cap is the binding constraint at $1.43M under 95% stressed utilization. Active management from day one is the required posture: enter positions only when supply APY exceeds the threshold and exit liquidity exceeds 1.25×.

The recommended initial policy cap is $20M for the Ecosystem Spoke. The looping formula at $2.15B sUSDe supply and 6x leverage gives a steady-state analytical ceiling of $39.8M, and the $20M initial cap is set below this pending further analysis as pool depth and utilization history develop. The Correlated Spoke is sized independently at $10-15M. Both are steady-state targets.

Scaling is recommended as Plus Hub TVL and borrow depth develop, with rebalancing triggered when utilization approaches 90% or the exit liquidity ratio falls below 1.25×.

The recommendation changes when three conditions are simultaneously met:

- Plus Hub TVL grows to the point where the exit liquidity cap at high utilization exceeds the $20M initial cap (approximately $250M pool TVL at 90% utilization), at which point scaling toward the looping formula ceiling of $39.8M can be assessed;

- per-Spoke IR curve parameters are disclosed and confirm yields at or above the threshold at realizable utilization; and

Plus Hub draw cap accommodates at least $20M in the Ecosystem Spoke.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network