Insights / Protocol strategy

There is a third way in defi lending

The October 10th liquidation event triggered a debate in DeFi lending: are monolithic liquidity models more robust than isolated markets, or do they simply concentrate risk in different ways? Much of the discussion has focused on these two extremes. But there is a third lending architecture that has received far less attention.

By Silvio Busonero ·

There is a third way in defi lending

The October 10th liquidation event triggered a debate in DeFi lending: are monolithic liquidity models more robust than isolated markets, or do they simply concentrate risk in different ways? Much of the discussion has focused on these two extremes. But there is a third lending architecture that has received far less attention, despite being among the best performers over the past year.

This article examines that third model: the SubDAO-based lending architecture pioneered by Sky:

At a high level, lending protocols balance three core components: infrastructure, risk management, and governance. Different architectures align these components in different ways, leading to very different risk and return profiles.

Monolithic lending models concentrate these functions within a single protocol. A central entity sets risk parameters, manages markets, and optimizes for liquidity efficiency. Aave v3 is the canonical example, and remains the leading model by most revenue and usage metrics.

At a high level, lending protocols balance three core components: infrastructure, risk management, and governance. Different architectures align these components in different ways, leading to very different risk and return profiles.

Monolithic lending models concentrate these functions within a single protocol. A central entity sets risk parameters, manages markets, and optimizes for liquidity efficiency. Aave v3 is the canonical example, and remains the leading model by most revenue and usage metrics.

Vault or curator models externalize risk management to independent curators, while maintaining shared infrastructure. This design saw explosive growth in 2025, but also proved fragile during the October 10th event. While markets are technically isolated, lender concentration creates hidden dependencies, amplifying liquidity risk during stress.

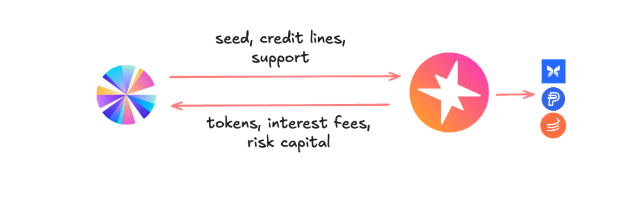

The SubDAO model takes a different approach. A large, unified liquidity pool is allocated to specialized entities—SubDAOs—that operate under a shared governance framework. These allocators can access undercollateralized credit at governance-defined rates, and earn returns by deploying capital more efficiently than the base protocol.

Sky and its largest SubDAO, Spark, provide the clearest real-world example of how this model functions in practice.

Sky economics

MakerDAO’s DAI was initially minted using the Collateralized Debt Position (CDP) model, where users locked ETH to mint DAI at a set rate. Its success coincided with the early adoption of DeFi, while competitors like USDT and USDC focused on a CEX first strategy, allowing them to grow massively.

After the endgame and rebrand, Sky introduced a new protocol design:

- The new stablecoin, USDS, earns a governance set rate (if staked) and is deployed in DeFi and RWAs. No need to borrow, Sky allocations is delegated to subDAOs.

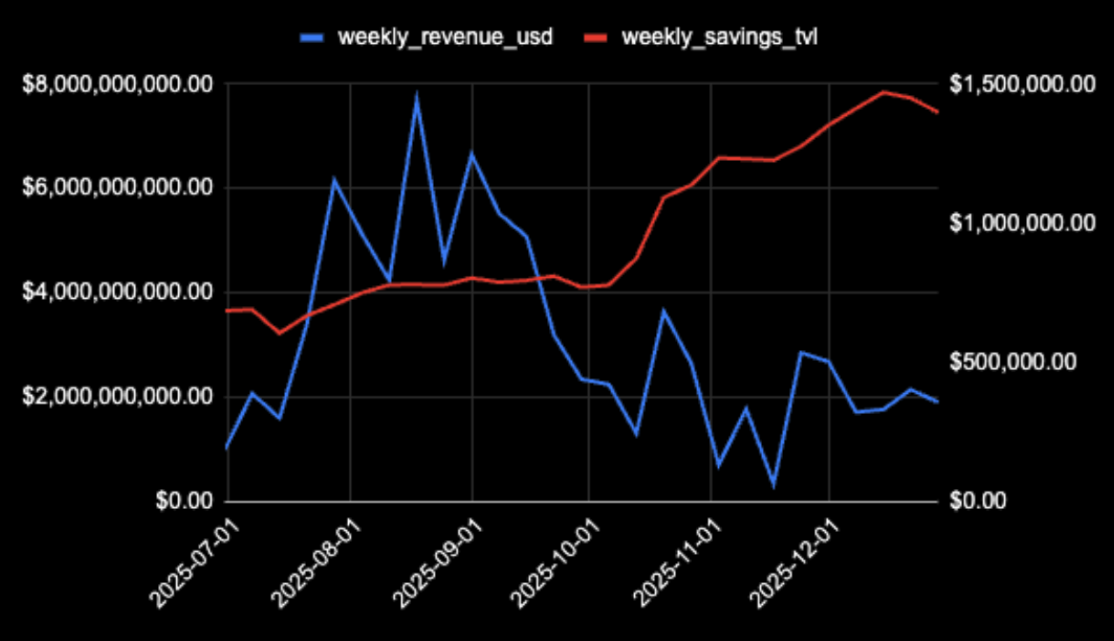

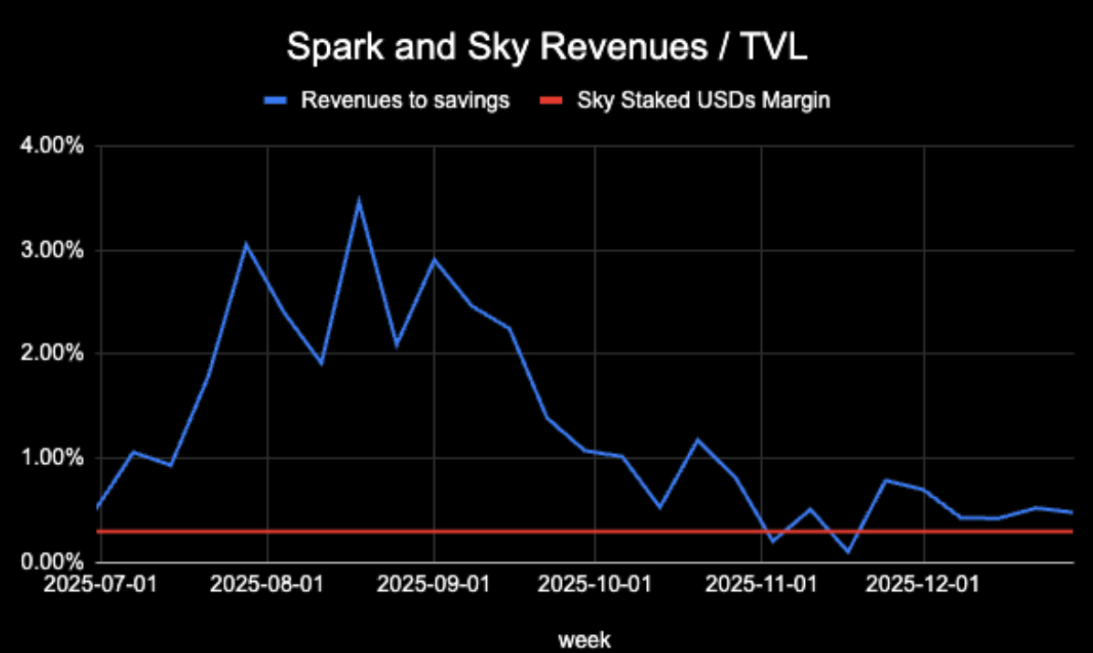

- USDS is meaningfully more capital efficient than DAI. As a result, Sky remains one of the highest-revenue protocols in crypto, generating approximately $168m in annualized earnings.

This corresponds to an average margin of roughly 1.8% on TVL, exceptionally high by DeFi standards, and significantly above Aave’s margins for comparison.

- USDS: Sky earns 30 basis points (bps) on staked USDS, which receive the Sky Saving Rate (currently 4.30%). Most USDS is staked, and the overall holder base remains relatively small (under 10,000). Sky earns the full Sky Saving Rate on the unstaked USDS.

- The largest holders of staked USDS are Spark (around 42%), Sky treasury, some DeFi contracts and other treasuries (like ENS).

- DAI: Sky earns a spread (between 5-8%) on unstaked DAI, which constitutes 90% of the unstaked amount.

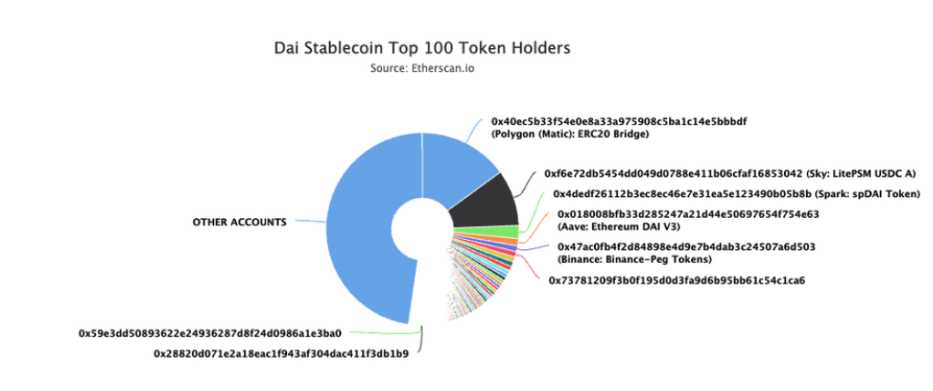

- Despite the current USDS focus, DAI still has a large holder base (580,000) and is heavily used by other DeFi protocols.

In summary, Sky’s revenue fundamentals are solid, although high margins still depends on unstaked DAI, so expect them to trend down with the growth of USDS.

Looking at holders and usage, USDS is currently more an investment product than a decentralized currency.

Spark and the subDAO model

Spark has been the first subDAO, or “prime agent” in Sky jargon.

Sky has incubated (or branched out) Spark, and these are the main points of their ecosystem accord:

- Sky has seeded Spark initial operational expenses.

- Spark has access to an uncollateralized credit line at the Sky Base rate, providing sufficient risk capital and stabilizing capital.

- In exchange, 65% Spark token is owned by Sky and used for liquidity mining programs for USDS, indirectly benefiting Sky token.

- Spark activity needs to adhere to Sky Atlas, a sort of regulation that sets risk parameters and governance for the subDAOs. Sky retains some governance rights in case of emergency. The risk management is partially controlled by Sky.

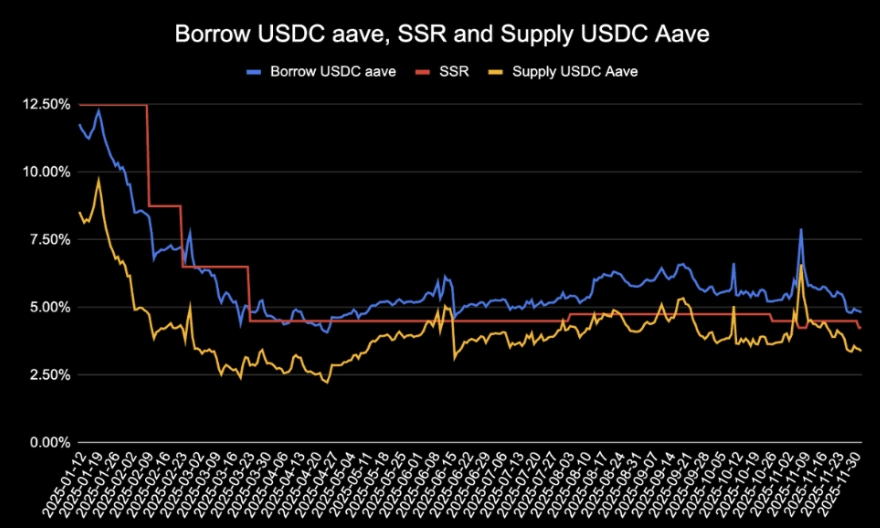

Spark’s business model is straightforward: deploy capital at returns that exceed its borrowing cost from Sky. Borrowing costs have been roughly between Aave USDC supply and borrow rate (but remember, loans to Spark are undercollateralized). Moreover, Spark earns an extra 0.50% as a referral rewards from Sky.

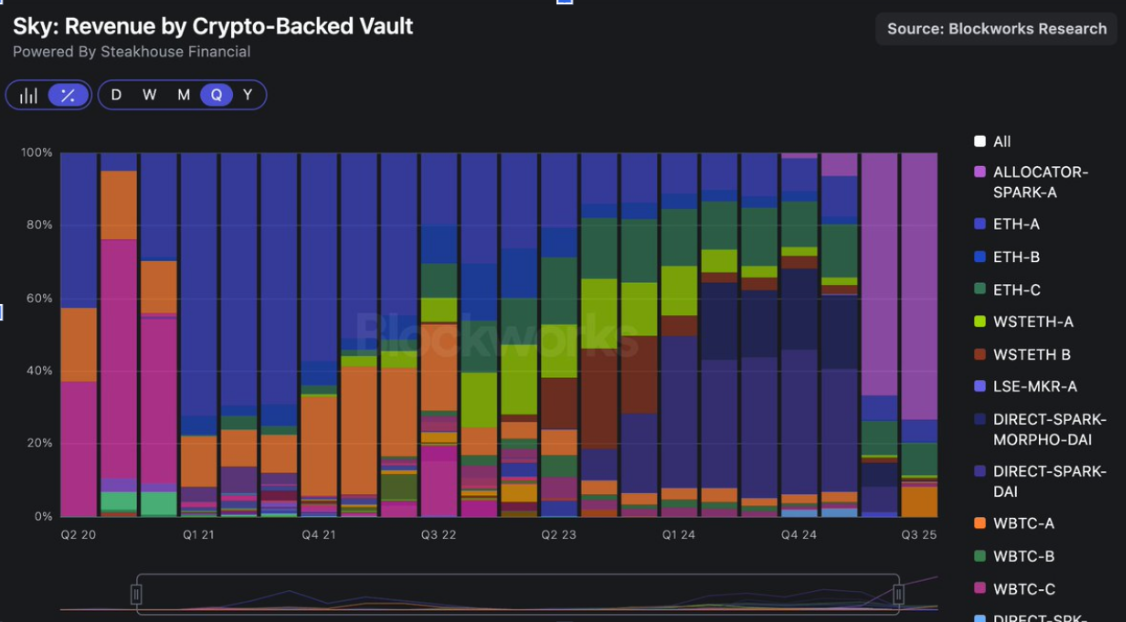

Over time, Spark has evolved from a single allocator into a “super-curator,” aggregating multiple yield-generating strategies under one operational umbrella:

- Offchain Yield: Integrating off-chain yield sources like the Anchorage lending facility and Arkis margin lending.

- Vault Management: Managing vaults on Morpho.

- Bluechip Market: Curating Sparklend, the blue-chip lending market on Sky.

- Direct Liquidity: Deploying a series of vaults called Spark Savings, which allow users to provide liquidity directly to Spark instead of going through Sky. SubDAOs do not have any lock in to borrow from Sky only.

Spark is currently making around 21m$ in net interest margins, paying around 171m$ in interest to Sky. The other revenue stream from USDS distribution is 17m$.

Spark makes more on the staked USDs than Sky. Notice that Sky 0.30% is fixed, and does not increase as yield increases, allowing Spark to pocket a large risk premium:

Spark is building a lending protocol, leveraging Sky liquidity to specialize in different lending verticals (including origination, margin trading, and Sparklend, an Aave v3 fork). Spark long term value will be in merging curation, liquidity and yield optimization infrastructure.

There are also other SubDAOs (like Grove, focused on RWA, and Keel, focused on Solana ecosystem) - and more will be launched to cover the different investment verticals.

SubDAOs are working

Sky and its SubDAOs illustrate a different path for protocol scaling: one that prioritizes specialization and execution speed without fragmenting liquidity.

Instead of forcing a single DAO to manage every market and risk surface, the SubDAO model allows independent teams to move quickly, specialize by asset class, and retain direct economic upside, while remaining anchored to a shared liquidity and governance framework.

Beside the healthy margins, there are some other reasons for Sky and Spark to have outperformed the sector:

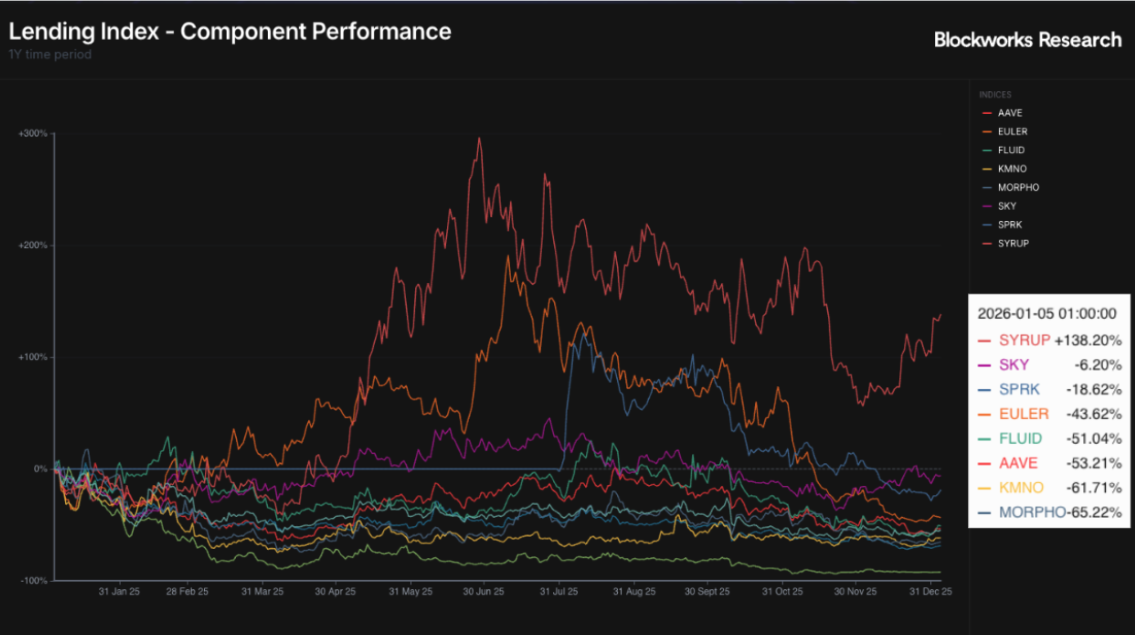

- They did not incur price and TVL setbacks as severe as Morpho and Euler after October 10.

- Little exposure to Ethena (that suffered the most from the immediate risk off environment), helped in retaining TVL.

- Stable governance and no DAO drama, which penalized Aave token toward the end of the year.

I see these challenges for Sky:

- Organically attracting depositor demand and growing the demand side of sUSDS (fintech partnerships, retail apps). While the strategy has focused on the allocation, the demand side has been largely inherited from DAI (that has still more holders and activity than USDs). Growing the demand side of USDs is key for the ecosystem,

- Managing subDAOs and related governance. The disadvantage of this model is potential governance overhead, and misaligned incentives. There is a delicate equilibrium between the ecosystem actors.

The SubDAO model balances decentralized control with execution delegated to specialized, fast-moving teams, while leveraging the liquidity moat as a huge competitive advantage compared to the standard lender - borrower approach in crypto vault managers.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network