Insights / Protocol strategy

Should Aave compete with revolut?

The "Aave will win" proposal brings more alignment between labs and tokenholders and a $50m bet to expand in fintech. Is this the right direction or a step too far?

By Silvio Busonero ·

The "Aave will win" proposal brings more alignment between labs and tokenholders and a $50m bet to expand in fintech.

Is this the right direction or a step too far?

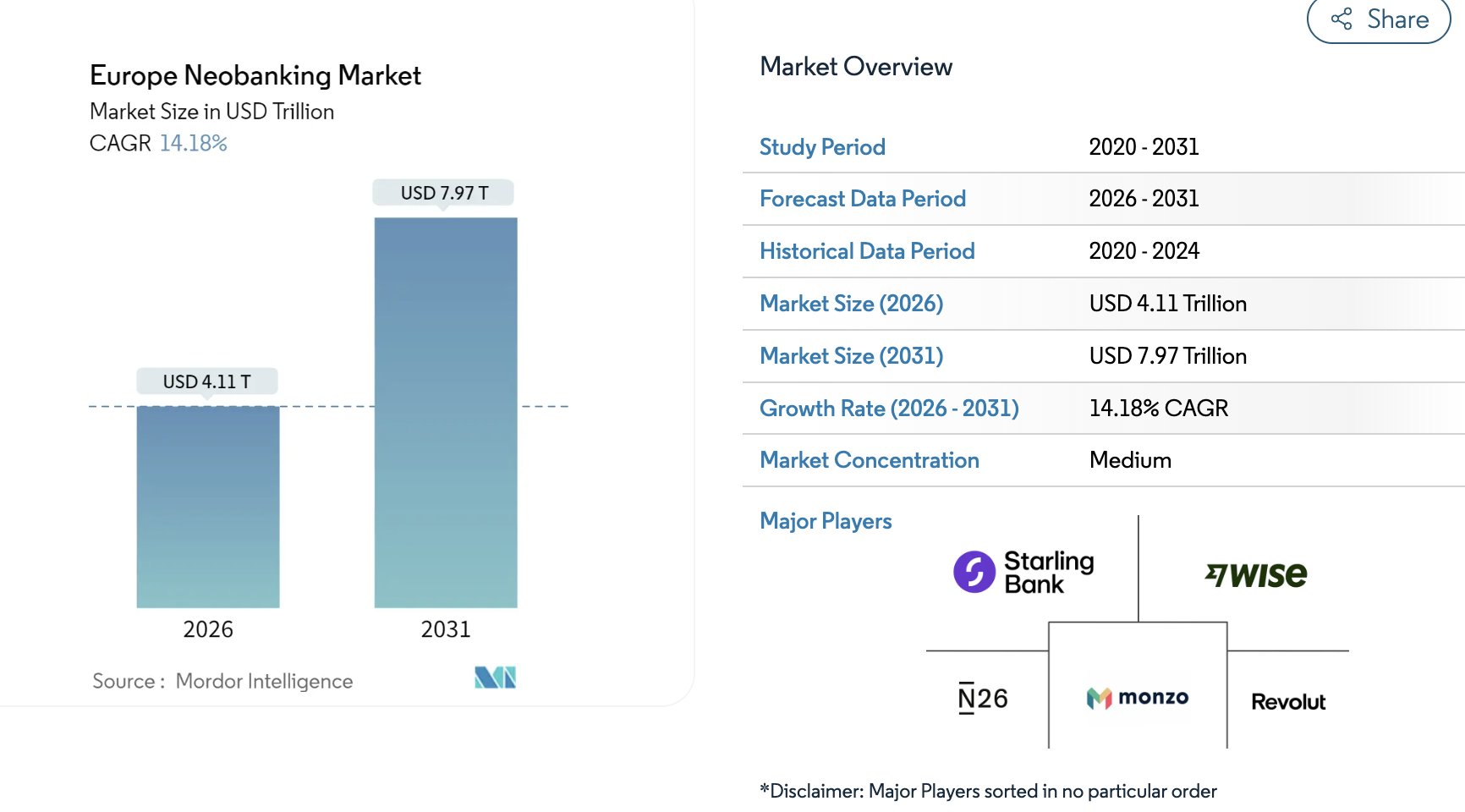

A 4 trillion opportunity

Aave new product lines expands into traditional banking services for retail and institutions.

The total customer funds held in fintech apps in Europe only is 4 trillions (40x current defi tvl), expected to grow to almost 8T$ in 2030.

Loans are registering the fastest ascent in the sector, at a forecast 44.95% CAGR.

In traditional fintech, customer acquisition costs are very high - between 80$-130$ for retail and thousands for institutions. The investment requested by Labs is in line with these benchmarks and may even be on the low end.

There may be other ways to deploy $50M, but growing fintech applications powered by the protocol is certainly one of the most compelling.

Composability can beat fintech

A more interesting question is: what can Aave do better than fintechs?

It's hard to win on the "supply and earn" feature. Instead, crypto apps must drive adoption by integrating unique experiences enabled by DeFi.

One example borrowing against stocks, something that is nearly impossible for retail investors, and even high-net-worth individuals, in traditional finance. Bank A cannot verify holdings in bank B, and loans are usually confined to the brokerage account.

Composability can be the true edge and many new use cases will emerge in the next few years. Being closer to the end users of money can help crypto develop these innovations faster than if it remains purely in the backend.

Is this even sustainable?

The Labs funding request is $50M per year, subject to a governance vote annually.

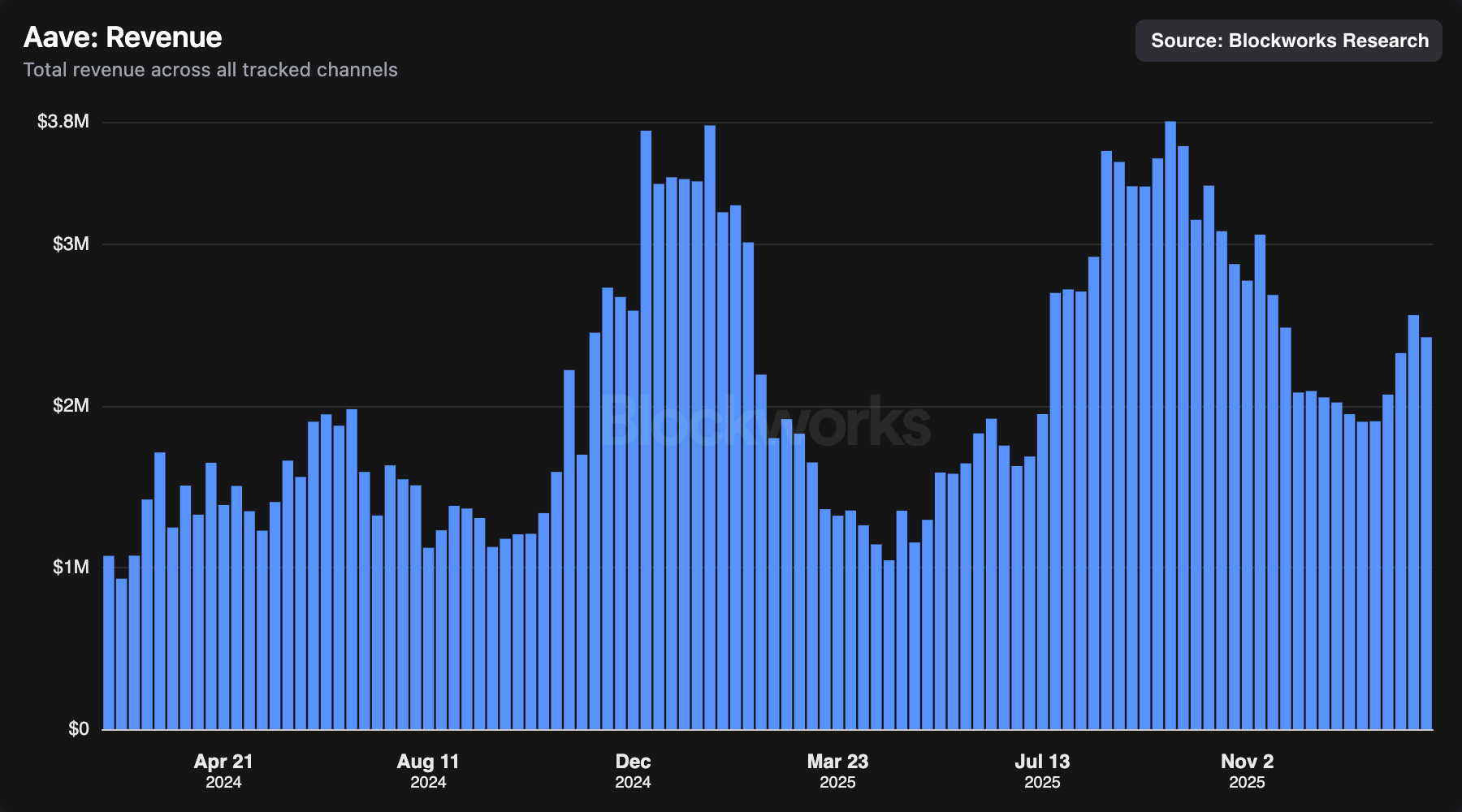

Aave closed 2025 with $100M in revenue and is on track for $120M. I think it is very likely that this number increases to $150M with the launch of v4 and the introduction of new monetization streams.

According to TokenLogic, the current projected costs for 2026 are $140M; these would rise to $190M after the proposal. The annual burn would be between $40–60M.

With a treasury of $170M, the runway would still be more than three years.

A larger issue, though, is concentrating too much liquidity into Aave token, since the proposal requests 50% of the treasury’s stablecoins.

hot take: let’s stop the buybacks ($35M in 2025). Capital is better allocated toward growth, especially given the increased alignment with $AAVE. Suspending buybacks provides an additional margin of safety and reduces treasury concentrations.

No other fintech in growth mode is doing buybacks (which also concentrate the treasury)

We need more long term planning

The opportunity is large and the funding is reasonable and sustainable. There have been also some valid concerns aspects about transparency and accountability. I think these are important, but are secondary to the strategic direction.

I like this proposal a lot. But I also would like to see a clearer multi-year strategic plan that aligns capital allocation, revenue targets, and measurable milestones.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network