Insights / Digital Asset Strategy

RWA Lending: The Road to $10 Billion

DeFi markets have proved strong pmf with crypto native assets - but what about RWAs?

By Silvio Busonero ·

RWA Lending: The Road to $10 Billion

DeFi markets have proved strong pmf with crypto native assets - but what about RWAs?

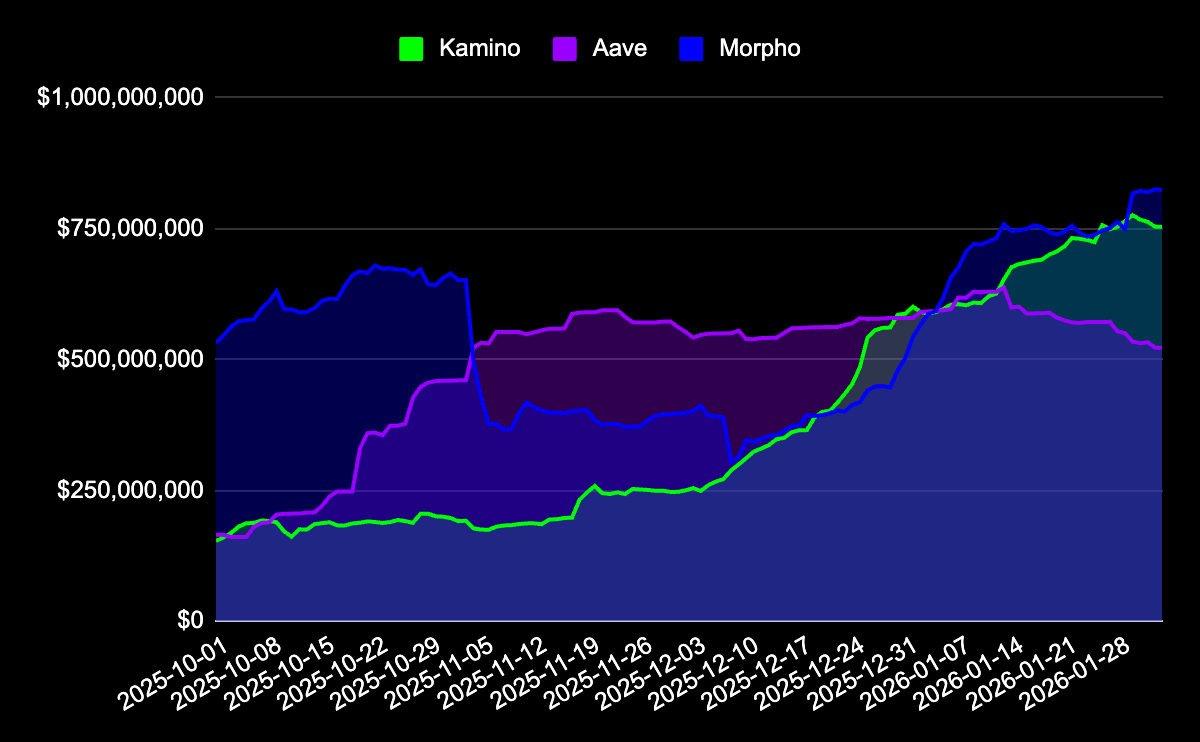

While the market crashed, RWA in lending continued the upward trend, getting to currently about 1.6b$ TVL (roughly 3% of total lending size).

Morpho and Kamino are head to head in the race:

That said, the RWA % in lending is still minimal, and its relative growth is also due to price crashing.

For onchain borrowers, using stocks / bonds and fixed yield as collateral may sound trivial but the reality of traditional finance tells another story:

- Bank A cannot verify stocks help in bank B

- If credit is available at bank B, it often goes into the brokerage account, so it’s very hard to pull out liquidity from it

During the last weeks, I’ve talked with various protocols and institutions. The goal of this article is to outline the barriers that need to be solved for this market's growth.

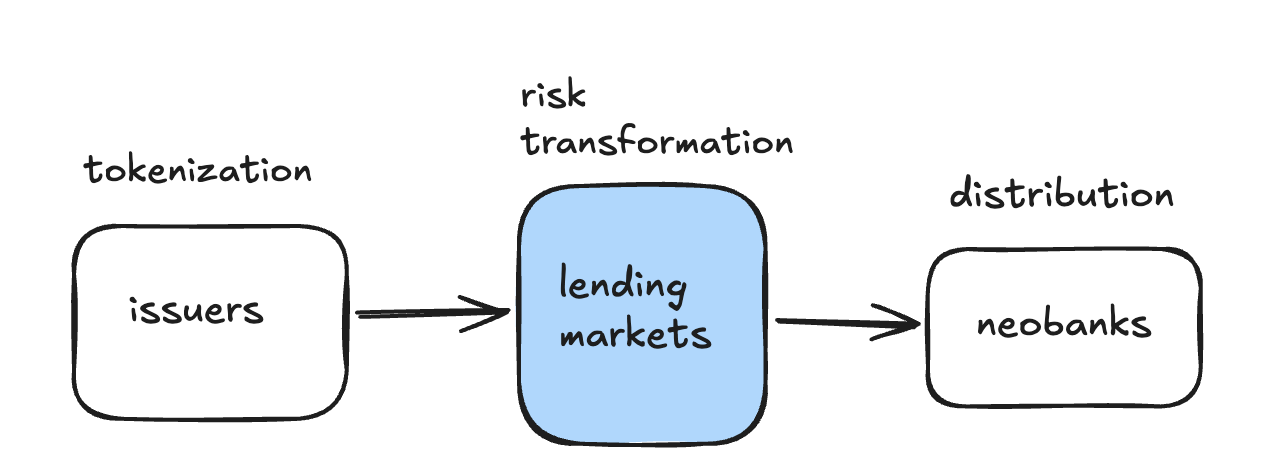

The barriers to make RWA productive

Liquidity

Crypto-native assets trade 24/7 with deep secondary markets. Most real-world assets do not. This creates a structural liquidity mismatch:

- Liquidations require either strong secondary markets or rapid redemption mechanisms

- Secondary liquidity is costly and typically subsidized by issuers.

- Risk providers often treat liquidity as the primary requirement for listing new RWA.

Examples in the market include:- BlackRock’s BUIDL liquidity on Uniswap. An automatic system helps users find the best price from a group of approved trading partners (including Flowdesk, Tokka Labs, and Wintermute). This is a way to do secondary permissioned liquidity in size.

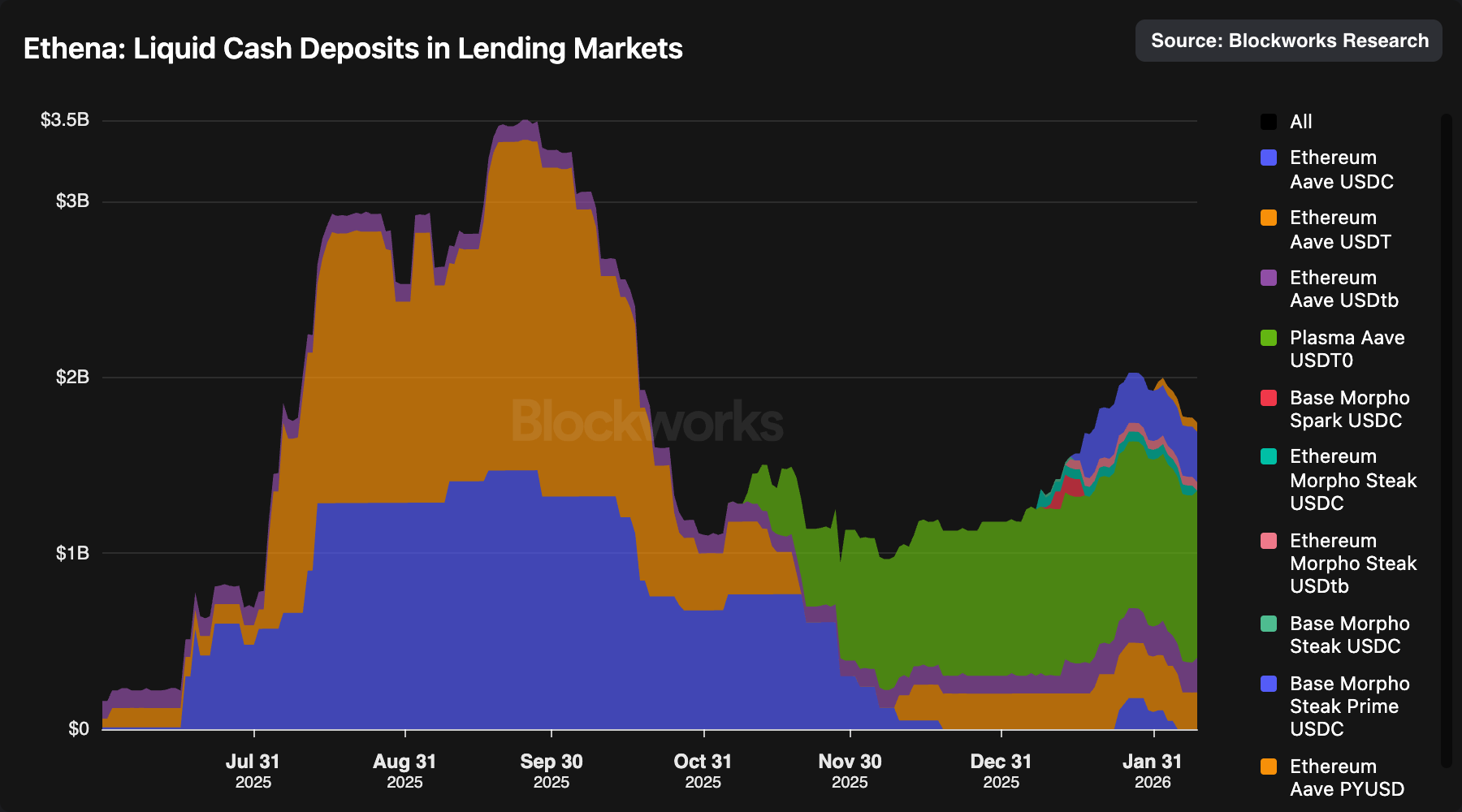

- Liquid stablecoin reserve backstops (e.g., Ethena, Maple) capable of absorbing redemptions in size:

- Transparent redemption mechanisms with real-time reserve verification (tools like Accountable)

- High efficiency in the dex side helps as well: Fluid for instance is capturing the majority of volumes for syrupUSDC and USDT, thanks to its superior liquidity efficiency

- At the protocol layer, innovation can also help with new market designs that better match collateral liquidity profiles to borrowing demand. Avon on megaEth is working on this.

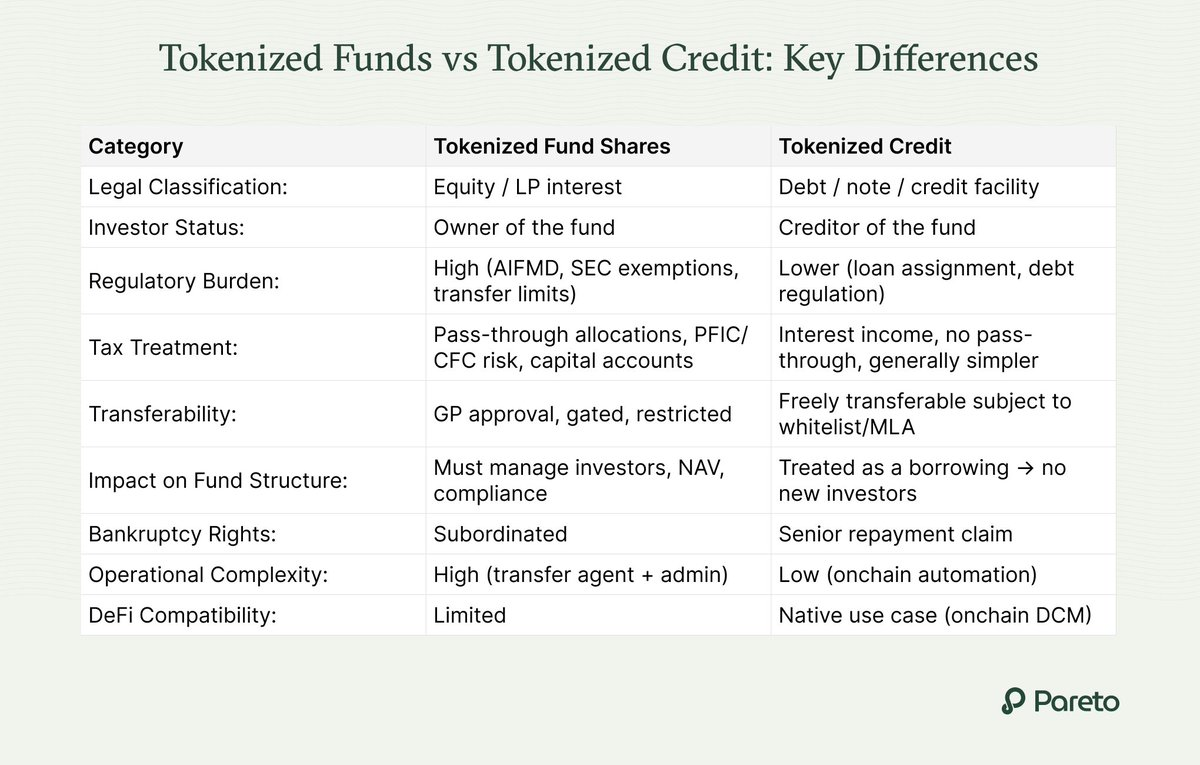

Common legal wrapper

There are several legal and onchain wrappers for tokenized assets. One notable example is Pareto, that is standardizing credit as is generally simpler to operationalize as it's structured as borrowing (a debt instrument) rather than ownership.

This avoids complex fund investor/limited partner onboarding, allows for simpler position transfers via loan assignment, and fits more naturally into DeFi for automated interest accrual and covenant monitoring.

Compliance

Compliance is not a one-size-fits-all solution; requirements differ significantly across geographies and asset classes. Players like Keyring offer zero-knowledge (zk) compliance solutions that can be adapted to various use cases, enhancing privacy and flexibility.

The other problem is integrating these solutions in protocols:

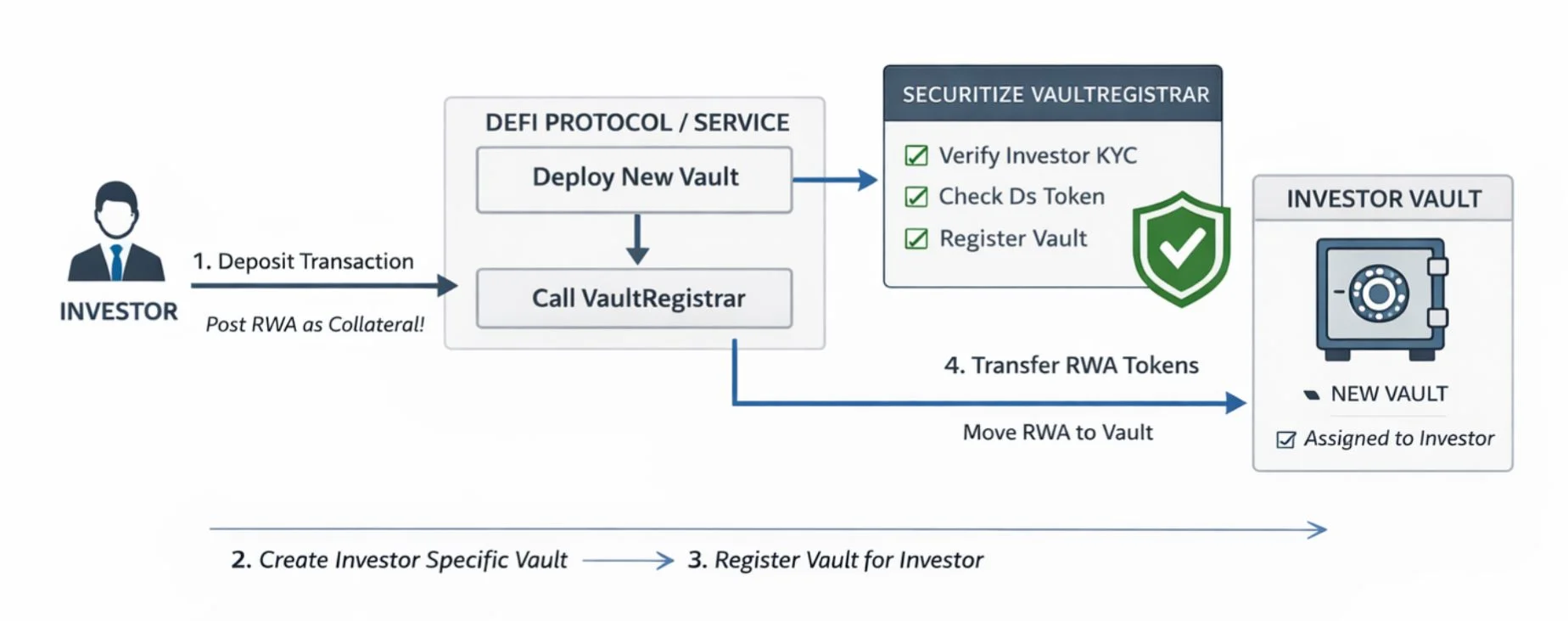

Securitize is working on the vault registrar, that is user specific vaults to avoid handling the compliance at a protocol level. Ideally different vaults can have varying level of verification and do not disclose sensitive information, while preserving the travel rule.

- The other solution is using transaction level gating with onchain requirements using tools as Predicate (Predicate.io)

Organic Distribution

Issuance and listing in market is not enough. Borrower demand is largely a function of speculation.

Neobanks are emerging as the ultimate distribution channel for RWAs.

There are 100s of stablecoins neobanks who need to differentiate and offer competitive services to users. There is obviously pmf for payment, financial services are next. Players like Etherfi and Avici are best positioned to offer new products that benefit from lending markets.

RWA lending’s long-term growth depends not only on infrastructure but on reaching users where they already manage capital.

This is a must have: utilization is currently driven by incentives and basis trade, with some rwa experience little borrowing activity (notably stocks).

Lending is decoupling from crypto

RWA lending is small but growing fast, and plenty of institutions are looking to enter the market.

The path is building resilient liquidity, standardizing the legal wrappers for asset tokenization, implementing adaptable compliance at the transaction level, and securing organic distribution through platforms like neobanks.

Just as we have witnessed stablecoins and prediction markets find their definitive product-market fit, the lending protocols that successfully bridge the divide between onchain efficiency and traditional finance's requirements are poised to be the next major growth sector in DeFi.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network