Insights / Protocol strategy

Why the defi lending moat is bigger than you think

The mindshare of vaults and curators is rising, and lending protocol thin margins are under attack. But lending has a large moat in the credit value chain. Let’s quantify it.

By Silvio Busonero ·

Why the defi lending moat is bigger than you think

The mindshare of vaults and curators is rising, and lending protocol thin margins are under attack. But lending has a large moat in the credit value chain. Let’s quantify it.

Across Aave and SparkLend, interest fees paid by vaults to lending protocols exceed the revenues vaults generate themselves, directly contradicting the narrative that distribution is king.

So Aave makes more money than the vaults built on top of it, but also and more than the issuers (like Lido and Etherfi) of assets employed in lending protocols. To see why, we break down the DeFi lending value chain and follow fees across pooled-liquidity protocols.

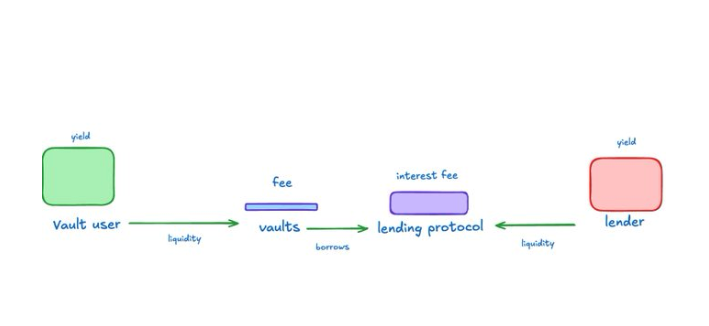

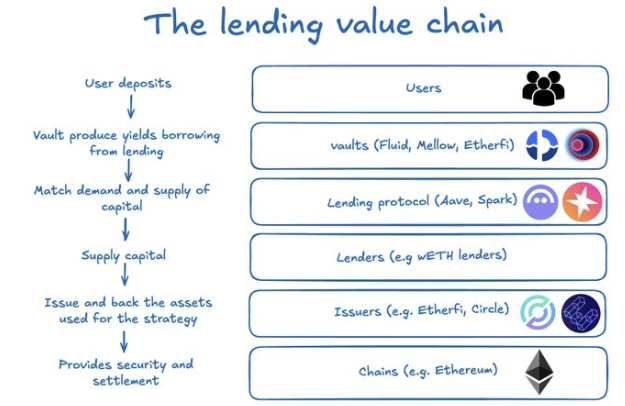

The lending value chain

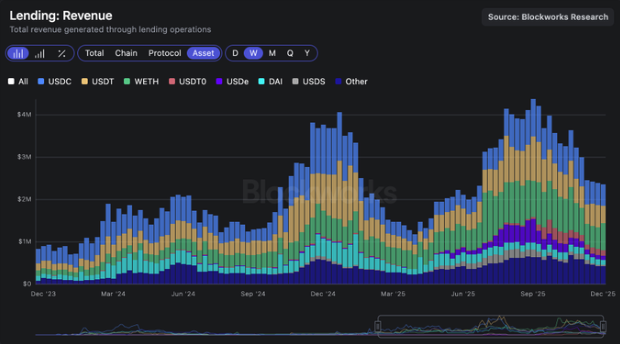

The lending category makes more than 100$m on aggregate. That value is generated across a complex stack: the settlement blockchain, asset issuers, lenders, the protocol and the distribution vaults are all involved in the demand and supply for these markets.

In the previous article we saw a lot most of the usage is due to basis trades and farming opportunities, and broke down the main strategies.

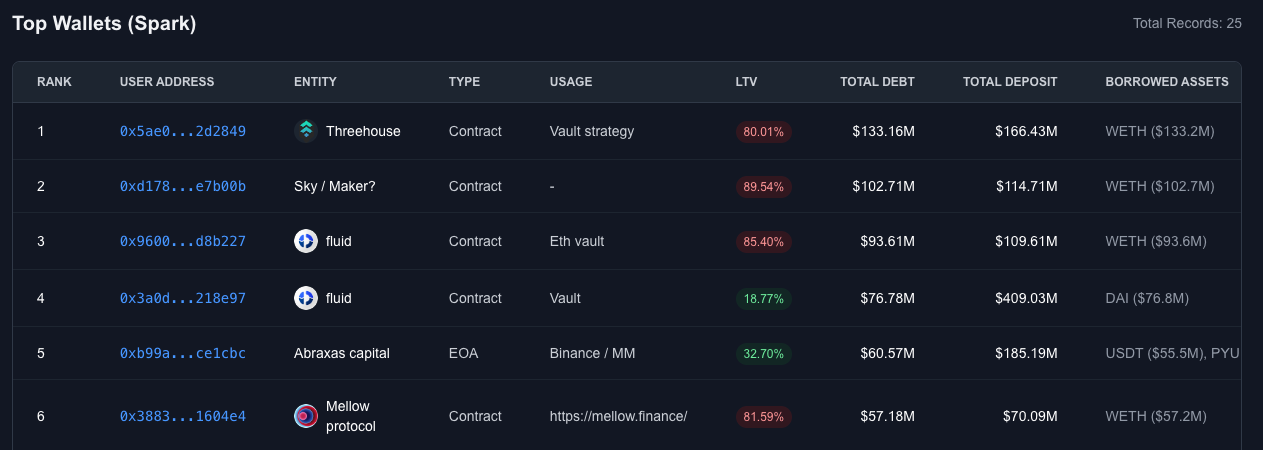

But who are the entities demanding capital from lending markets? I analyzed the top 50 wallets of Aave and SparkLend (you can see them here: https://lending-crm.vercel.app/).

- The largest counterparties are vaults like Fluid, Treehouse, Mellow, Etherfi and Lido (also issuers). They own distribution for users who want to get extra yield without managing the loops, the risks etc.

- Other large counterparties include institutional funds such as Abraxas Capital, which deploy external capital into similar strategies and therefore exhibit economics broadly comparable to vaults.

Vaults are only a part of it however:

- Users: deposits and look for vault / strategist to earn extra income on crypto asset.

- Lending protocol: They provide infra and liquidity to match supply and demand. They make money with a % fees on borrow apy.

- Lenders: can be passive users or other vaults, are the supply side of capital in the lending markets

- Issuers: most onchain assets used in lending markets are backed by something. The asset issuance business is a core part of the value chain. The backing assets generate yields, part of which is captured by issuers.

- Chain: the rails where everything happens.

Lending protocols are making more than downstream vaults

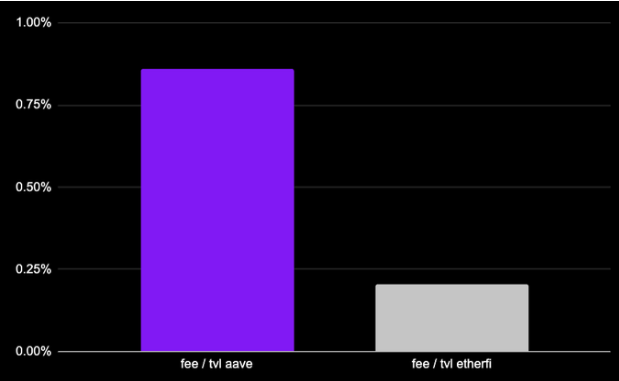

Consider the Ether.fi liquid ETH vault, the second-largest borrower on Aave, with roughly $1.5 billion in outstanding loans. The strategy is straightforward: supply weETH (≈ +2.9%) and borrow wETH (≈ –2%). The vault charges a 0.5% platform fee on TVL.

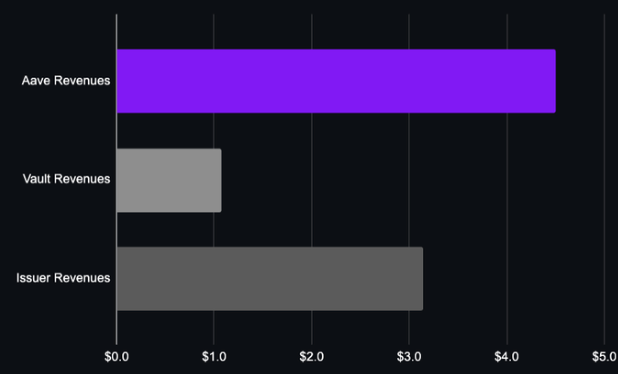

Of Ether.fi’s total TVL, approximately $215 million represents net liquidity deployed on Aave. This generates about $1.07 million per year in platform fees for the vault. The strategy pays roughly $4.5 million in interest fees to Aave, (calculated as $1.5B in borrowings × 2% borrow APY × 15% reserve factor).

Even in one of the largest and most successful looping strategies in DeFi, the lending protocol earns several times more than the vault operating on top of it:

However, Etherfi is also an issuer and this vault is directly generating demand for weETH:

- The lending value add (Aave revenues) is greater than vault strategy value and issuer value add.

- The lending layer adds more economic value than any other part of the stack.

We can replicate the analysis on other popular vaults:

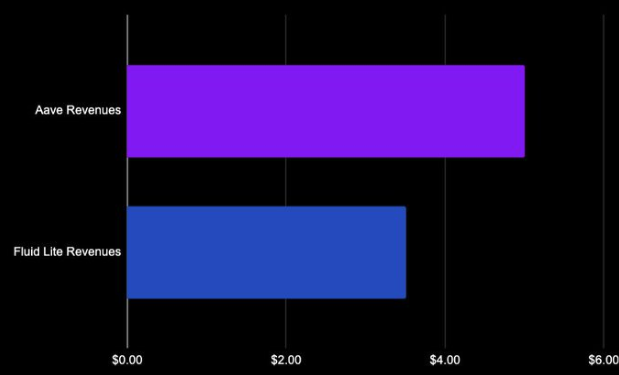

- Fluid lite Eth: performance fee of 20% and exit fee of 0.05%. No platform fees. Borrows 1.7B$ in weth from aave and pays 33mln$ in interest, of which around 5mln$ go to aave. Makes almost 4mln$ in revenues.

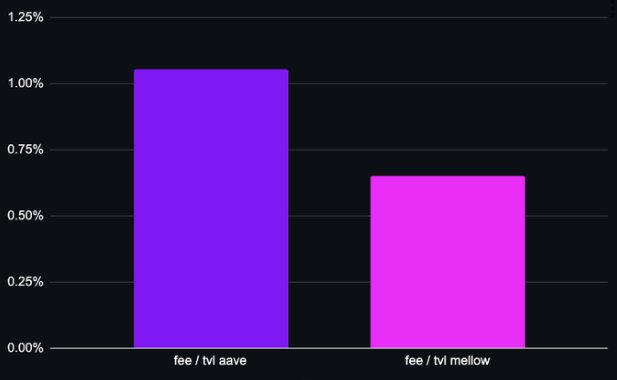

Mellow protocol strETH has a 10% performance fee, and is borrowing 165mln$ with a tvl of around 37mln$: again we see that Aave is making more money per unit of tvl than Mellow.

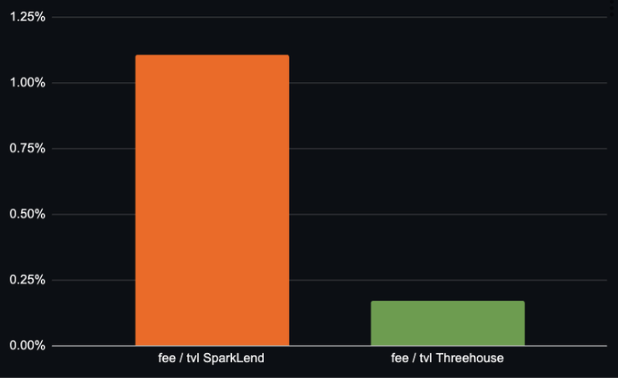

Let's consider one last example on SparkLend, the second lending protocol on Ethereum by total assets. Threehouse is among the top lenders and is running a looping Eth strategy.

Threehouse charges a performance fee on marginal performance on top of staked Eth (so on any return above 2.6%). Its vault is borrowing 133mln$ from SparkLend on 34$ of TVL.

Vault pricing has a huge impact on value capture, while the borrowing costs for these strategies are stable (since they depend on notional borrowed).

Things may change if we consider USD based strategies. However, lower leverage is compensated by higher interest rates (so protocol take rates). I don't expect results to drastically change.

In isolated markets expect more value to flow toward curators. The Stakehouse prime vault is an example: 26% performance fee while Morpho is running incentives. That said, this is not the end game of Morpho pricing, and curators have distribution deals with other platforms.

Lending versus issuers

Is it better to be Lido or Aave? This is harder to compute than vaults - as staked asset can be used to produce indirect revenues for lending protocol in the form of stablecoin interest fees. We need to approximate.

Lido is making around 11mln on the 4.42$b deposited on Ethereum core markets on performance fees. These positions back loans in eth and stablecoins in roughly the same proportion, so we can use the current Net Interest Margin to get yield from deposits.

With the current NIM at around 0.4%, we get 17mln$, more than 30% Lido (notice this is historically a low net interest rate margin)

The lending protocols have a moat

Measured against traditional finance, DeFi lending protocols appear low-margin when evaluated on deposit profitability alone. But this comparison misses where the moat actually lies.

Within the onchain credit stack, lending protocols capture more value than the downstream distribution layer and, in aggregate, more than upstream asset issuers.

Lending looks low-margin in isolation, but it is the highest value-capturing layer relative to every other participant in the onchain credit stack: vaults, issuers, and distribution included.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network