Insights / Protocol strategy

Why banks are 10x more profitable than lending protocols

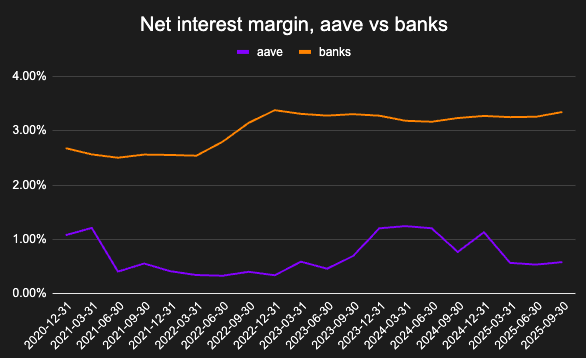

One USD in a bank deposit makes 10x money for the bank than the same USDC on Aave. This seems bearish for DeFi lending. In reality, it says far more about current crypto market structure than about the long-term potential of onchain credit.

By Silvio Busonero ·

Why banks are 10x more profitable than lending protocols

One USD in a bank deposit makes 10x money for the bank than the same USDC on Aave. This seems bearish for DeFi lending. In reality, it says far more about current crypto market structure than about the long-term potential of onchain credit.

This article explores how lending protocols are used today, why their margins look structurally lower than banks’, and how that could change as lending starts to decouple from crypto-native leverage cycles.

The role of credit onchain

My first job involved analyzing banks books and assessing borrowers health.

Banks transmit credit to real businesses and their margins are directly related to the economy. In the same way, analyzing borrowers of DeFi protocols can help understand the role of credit in the onchain economy.

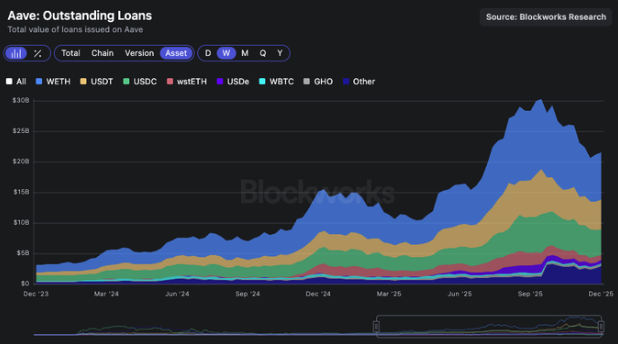

Aave has surpassed an impressive 20b$ of outstanding loans - but why are people borrowing onchain?

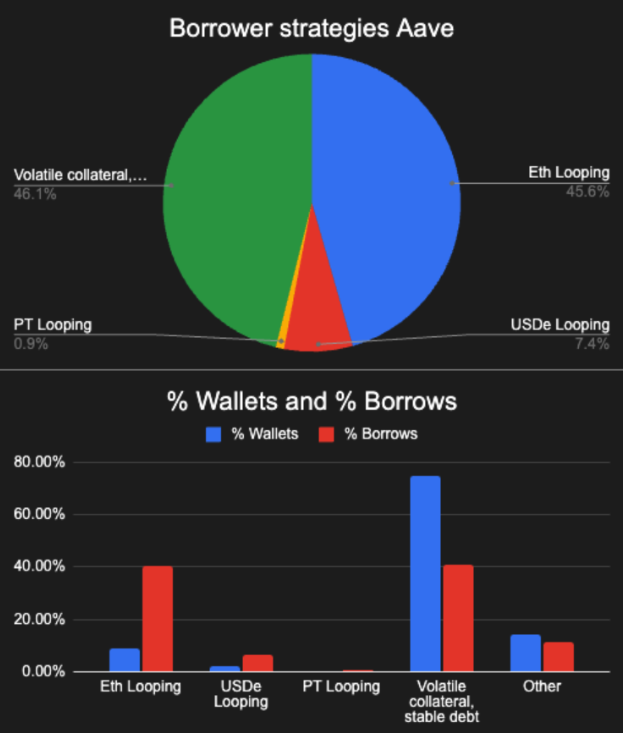

Aave borrowers: what they actually do

Borrowers strategies can be classified in four buckets:

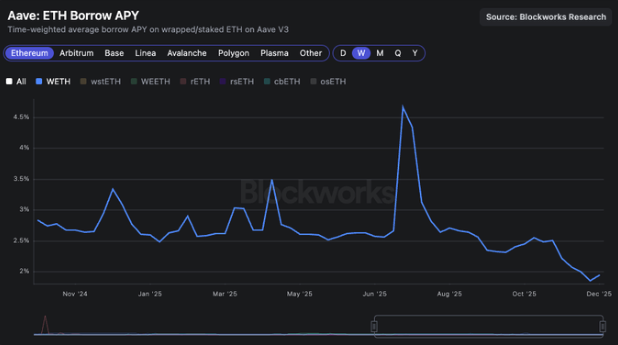

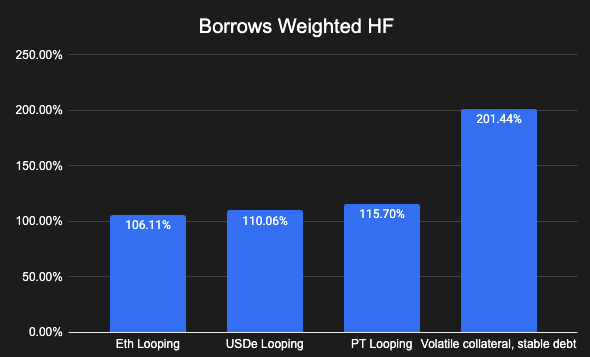

- yield bearing ETH as collateral, WETH debt: yield on staked ETH is usually higher than WETH, creating a structural basis trade (basically, being paid to borrow WETH). Currently contributes to 45% of outstanding borrowing amount, with only a few whales contributing to most of it. These wallets are related to issuers of staked ETH (like EtherFi) and other loopers. The risk of this strategy is spikes in the costs of WETH, which can quickly drive health factors below liquidation.

- Stablecoins and PT loopers: a similar basis trade is generated by yield bearing (like USDe), which can be higher than the cost of borrowing USDC. These positions used to be very popular before October 11. While structurally attractive, these strategies are highly sensitive to changes in funding rates and protocol incentives, which explains their rapid contraction when conditions shift.

- Volatile collateral, stable debt. This is the most popular strategy of users that want to get extra leverage on coins, or reinvest stables in highest yield farms to get a basis trade. This is directly related to farming opportunities and is the main source of demand for borrowing stablecoins.

- Others are residual. Stable collateral, volatile debt to short assets and volatile collateral, volatile debt to express pair trades.

For each of this strategies, there is a value chain of protocols that use aave to package them and distribute yields to retail users - these integrations are the real moat of a lending market in crypto today.

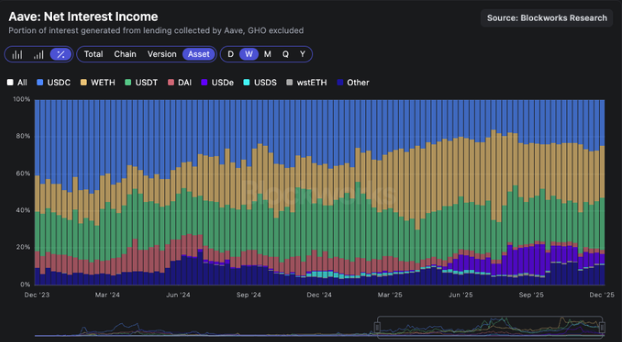

The "volatile collateral - stable debt" has the largest marginal contribution to the interest income (USDC and USDT borrowing yields make for more than 50% of revenues.

While there may be some businesses or individual that finance operations or real life expenses with crypto loans, this is very limited compared to use case related to leverage / exploit yield differences onchain.

These are three main factors that contribute to lending protocol growth:

- Onchain yield opportunities, like new launches and farming (e.g. Plasma)

- Presence of structural basis trade with deep liquidity (eth / wstETH and stablecoins)

- Partnerships with large issuers that can boostrap new markets (like pyUSD and RWA)

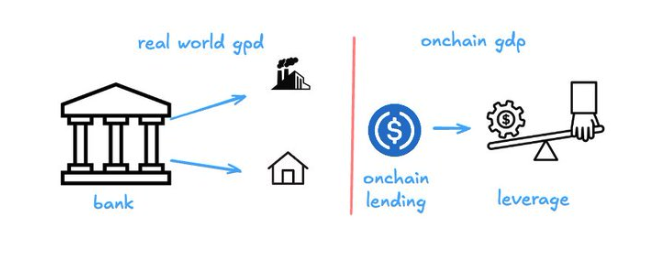

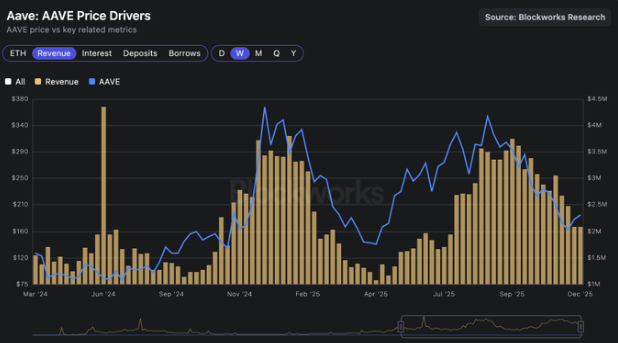

Lending markets are mechanically a direct beta of the crypto GDP, like banks are essentially a proxy for real world GPD. When crypto prices go up, yields opportunities increase, yield bearing stablecoins expand and issuers move more aggressively - increasing revenues, buybacks and ultimately the price of Aave.

Banks versus onchain lending markets

As we saw, one USD in a bank makes 10x money for the bank than the same USDC in Aave. Some people have called out this as bearish - but I'd say it's really part of the market strucure:

- Higher cost of funding in crypto. Banks borrow at FED rates (below the treasuries), Aave USDC deposits are usually slightly above treasuries.

- Risk transformation activity of general commercial banks is more complex and deserves a larger premium: large lenders manage billions of unsecured positions to corporates (for instance, to build data centers). This deserves a better premium that managing collateral values for looping ETH.

- Regulation and market power. Banking is an oligopolistic business with high switching costs and barriers to entry.

Detaching lending from crypto

Crypto categories that succedd are decoupling from crypto trends. Prediction markets open interest has been growing consistently despite ups and down in prices. Same goes for stablecoin supply - much less volatile than the rest of the market.

To behave more like broad credit markets, lending protocols are listing new types of risk and new types of collateral, such as:

- Tokenized real-world assets (RWAs) and stocks

- On-chain credit from off-chain originators

- Stocks or RWAs as collateral

- Structured underwriting via crypto-native credit scores

Tokenization makes lending one of crypto’s most natural endpoints. When credit decouples from price cycles, margins and valuations will decouple with it. I expect this to start happening in 2026.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network