Insights / Digital Asset Strategy

The quest for the next leverage flywheel

DeFi lending revenues depend on leverage looping: around 40% of current borrow demand is driven by staked ETH looping. The market is hungry for new leverage use cases, as the yield on the most popular looping strategy compresses.

By Silvio Busonero ·

The quest for the next leverage flywheel

DeFi lending revenues depend on leverage looping: around 40% of current borrow demand is driven by staked ETH looping. The market is hungry for new leverage use cases, as the yield on the most popular looping strategy compresses.

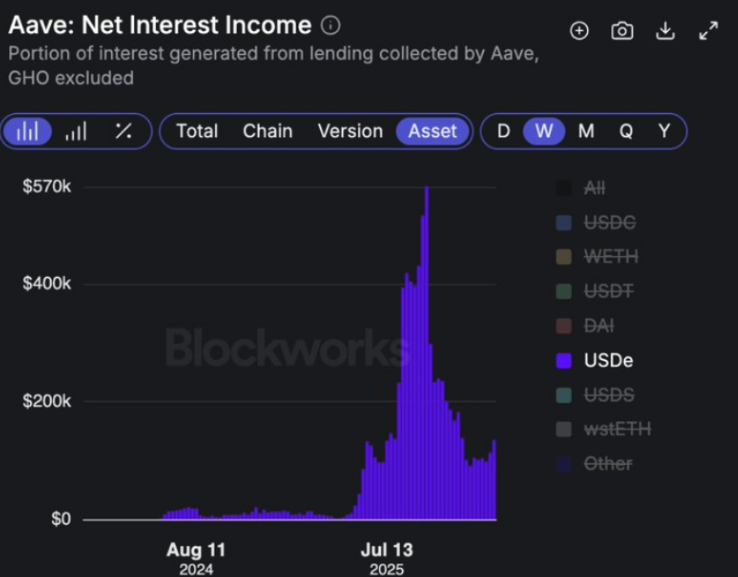

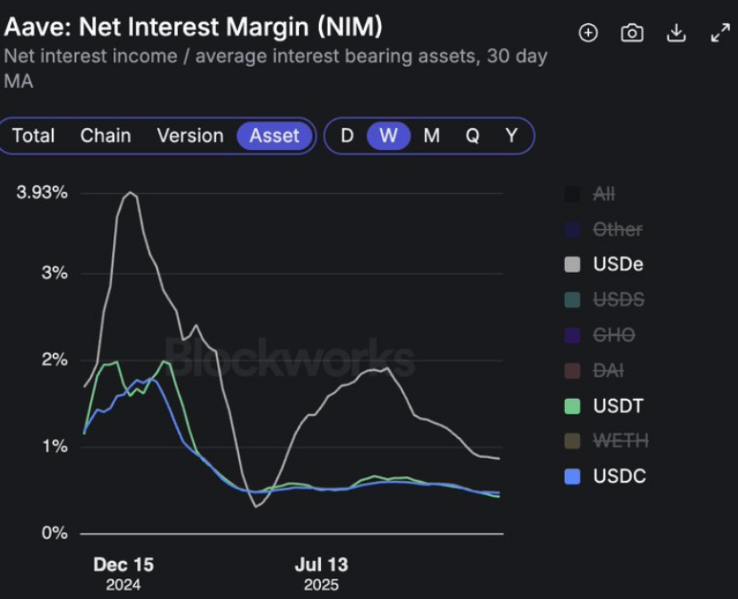

The success story for 2025 has been Ethena USDe, which, thanks to the Pendle integration, developed a massive demand for stablecoins on Aave.

I estimate that the integration resulted in 12-15m$ of net interest income for Aave (10-15% of total revenues), mostly in the form of USDe interest rates.

The leverage flywheel works thanks to:

- High redemption capacity and secondary liquidity.

- No duration risks for liquidations.

- High funding rates during part of the year making the trade profitable.

Putting all together, USDe produced massive surge of demand for Aave stablecoins (and for other lending protocols to a lesser extent).

USDe is very profitable for Aave.

The next question is: which assets can produce the same effect?

RWAs are the best candidate

RWAs could be a perfect candidate to expand lending markets revenues in size and diversity. There are over 22b$ of RWAs onchain, and about 1.5b$ are in deposited lending markets today across EVM and Solana.

RWA lending is showing sign of PMF with isolated markets, that can better adapt to idiosyncratic asset risks:

- Isolated markets have a big advantage in listing quickly and setting risk parameters for specific RWA needs.

- Moreover, increased demand for one asset does not increase the borrowing costs for everyone.

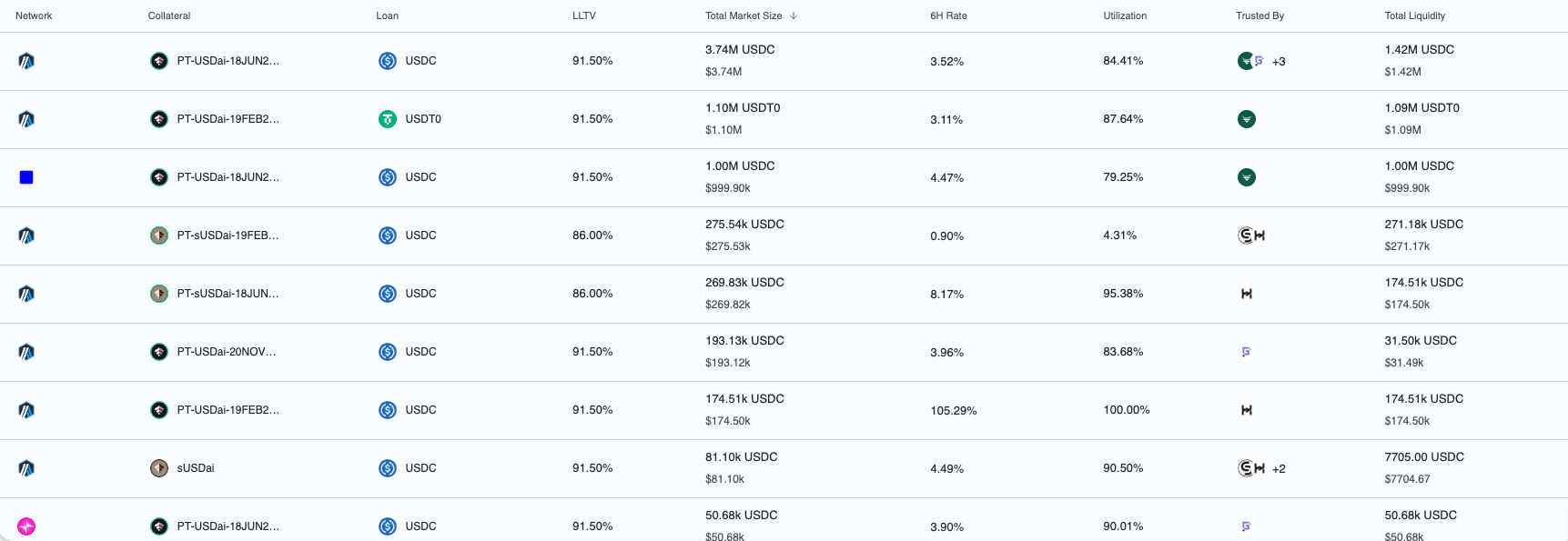

Morpho is leading with 750m$ deposits and 300m$ borrows.

The flipside is that isolated markets cannot recreate the same leverage flywheel as monolithic models due to fragmented liquidity.

Euler has shown how a multi asset market can actually improve the fragmentation / isolation tradeoff. A possible design would be to put in a connect all markets with collateral related to similar trades (e.g. aggregating all markets in the picture above).

To see the challenges with RWAs in lending, I’d look at a huge success story in the market today - Maple syrupUSDT, backed by a fixed rate lending book and a liquid stablecoin reserve.

SyrupUSDT shares similarities with USDe: above market yield, high capacity, presence of pendle yield tokens. However, Aave governance has decided to set more conservatively risk parameters and not list it as collateral due to a worse liquidity profile (particularly secondary liquidity, currently 20mln$ on dexes).

Maple liquidity cadence is different from Ethena, that does not add duration risk:

- Small variations in duration risk break the leverage flywheel adoption, as liquidators job becomes harder and less predictable.

- DeFi lenders, on their part - are more “money market” lenders than “credit market” lenders and current protocols are optimized for instant liquidity withdrawals.

RWA lending is also growing on Solana, where Kamino markets are also showing traction with Prime (Figure's tokenized HELOCs) with an isolated design:

We need to make more assets leverage friendly

While the success of Ethena USDe has demonstrated the immense revenue potential of onboarding new, high-demand assets, RWAs present unique challenges, primarily around duration transformation and non-atomic settlement.

In practice: can you liquidate it, how fast can you redeem it, and does the oracle reflect its true value.

Some approaches to mitigate the problem:

- Tranching to transfer duration risk to higher seniority: does not solve liquidation issues, but improves liquidity.

- Setting up isolated markets with specific parameters to transform money markets in credit markets.

- Oracles that take redemption values into account.

Unlocking leverage on new assets classes is will create the next growth leg for onchain lending markets.

Back to Insights

Newsletter

The Breakdown

Decoding crypto and the markets. Daily, with Byron Gilliam.

Blockworks Research

Unlock crypto's most powerful research platform.

Our research packs a punch and gives you actionable takeaways for each topic.

Blockworks Inc.

133 W 19th St., New York, NY 10011

Blockworks Network